A Market You Probably Have Not Been Watching

Published March 4, 2026

Christopher Gannatti, CFA

Global Head of Research

Key Takeaways

- South Korea has quietly emerged as one of the top-performing emerging markets over the past year—despite limited investor attention—highlighting how leadership rotations beyond the U.S. can materially reshape returns in 2026.

- While China, India, Taiwan, South Korea and Brazil dominate the MSCI Emerging Markets Index by weight, dispersion across smaller markets underscores that benchmark exposure often masks where the most intense gains are occurring, making strategy selection as important as the macro call.

- With the WisdomTree Asia Defense Fund (WDAF) leading early-2026 performance and offering differentiated exposure to South Korea, investors have a broader toolkit to actively position for shifting country leadership rather than passively accept benchmark concentration.

Every so often, a simple question reveals how narrow our field of vision can become.

Ask a group of U.S.-based investors to name one of the top-performing country equity markets over the past year. Most people know the U.S. was not the standout. They might point to Japan. Maybe a rebound story in Europe.

Very few would think to say South Korea.

And yet, South Korea has been among the strongest performers.1

That pause is instructive. Sitting inside one of the deepest and most liquid capital markets ever created, it’s natural for our U.S. attention spans to cluster around U.S. benchmarks. Even when we acknowledge that leadership has shifted abroad, our mental map of global performance is often incomplete.

Intensity May Not Be Influence

If a major economy can lead global returns without immediately registering in conversation, it’s worth asking: where else might opportunity be compounding, just outside our habitual line of sight?

If the opening question challenges perception, this figure sharpens the point—and adds necessary nuance.

Looking at Figure 1, South Korea leads over the past year. Peru, Colombia, and Egypt have posted eye-catching gains. Greece and Hungary show powerful multi-year recoveries. The dispersion is real, and it’s dramatic.

But the narrative isn’t just about returns. It’s also about scale.

In the MSCI Emerging Markets Index, the largest weights are China, India, Taiwan, South Korea and Brazil.2 These markets drive the benchmark’s structural exposure. When they move, they matter. By contrast, Peru, Hungary or Egypt can produce triple-digit returns and still barely register at the index level. They are smaller, often more concentrated, and sometimes more cyclical, features that can amplify both upside and downside.

That’s the tension embedded in the chart. Leadership rotates broadly across countries, but benchmark impact is uneven. Some rallies reshape portfolios. Others remain powerful but localized.

Understanding global equity performance requires tracking both dimensions simultaneously: return dispersion and market footprint. Without that context, we risk mistaking intensity for influence.

I placed the 5 largest market exposures, along with the broad benchmark, in bold text to set them apart in the table.

Figure 1: The Geography of Emerging Markets Equity Performance

Source: MSCI, with performance data for respective MSCI Emerging Markets Indices as of February 12, 2026. Past performance is not indicative of future results.

Emerging Markets Is Not a Monolith

Performance invites explanation. In South Korea’s case, it’s hard to ignore the role of artificial intelligence, semiconductor leadership and its position inside the global technology supply chain. In other markets, the drivers may be commodities, currency stabilization, reform momentum or simple valuation resets. The point is that ‘emerging markets’ is not a single story—it is a collection of very different macro regimes, sector exposures and policy paths.

That reality has direct implications for portfolio construction. The range of emerging markets strategies—broad beta, regional tilts, sector overlays, state-owned screens and factor approaches—means implementation decisions can matter as much as the macro thesis itself.

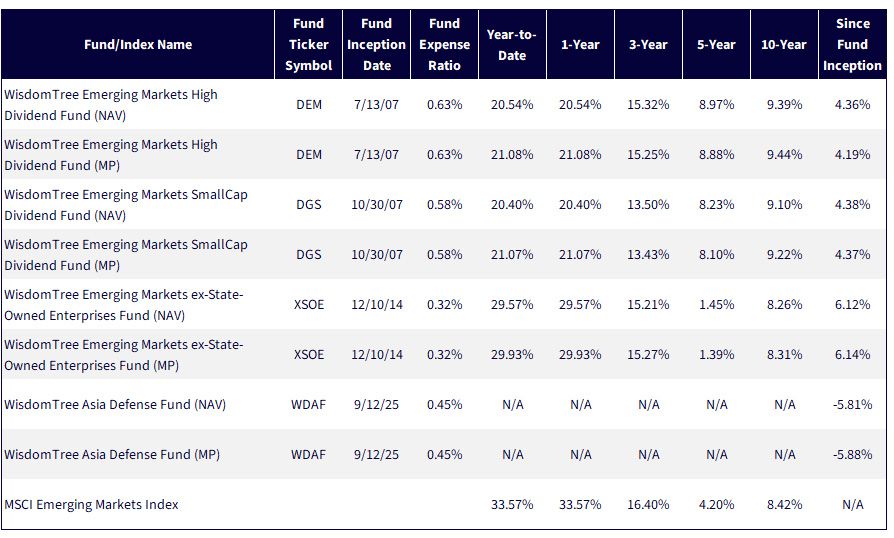

If we look at some of the WisdomTree strategies with significant emerging markets equity exposure, we find:

- The WisdomTree Emerging Markets ex-State-Owned Enterprises Fund (XSOE), which is designed to provide differentiated exposure that avoids companies with large government ownership stakes. In emerging markets, particularly in some countries rather than others, this can be a rather important consideration.

- The WisdomTree Emerging Markets High Dividend Fund (DEM), which has been running for nearly 19 years, with live calculation beginning in July 2007.

- The WisdomTree Emerging Markets SmallCap Dividend Fund (DGS), which also has been running for nearly 19 years, with live calculation beginning in July 2007.

- In September 2025, WisdomTree launched the WisdomTree Asia Defense Fund (WDAF), recognizing that similar forces that made the European defense segment attractive might also play out in Asia, a region also fraught with its own set of tensions.

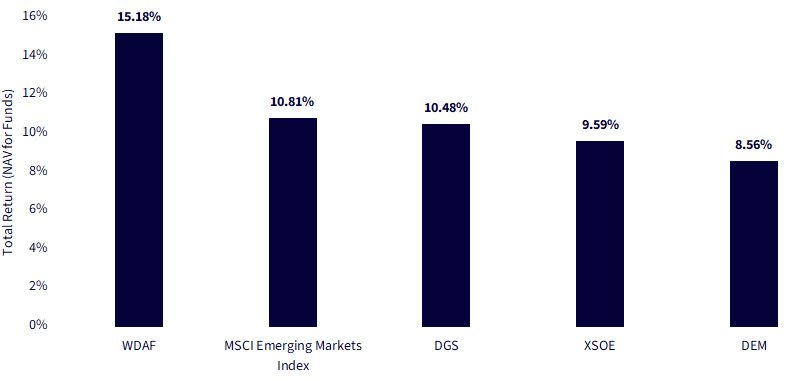

In Figure 2a, we see how these distinct strategies have started the year, measured against the returns of the MSCI Emerging Markets Index benchmark. WDAF has been the standout so far and also has the largest overall exposure to South Korea’s equity market.

Figure 2a: Gauging Performance to Start 2026

Figure 2b: Standardized Returns

Sources: WisdomTree, FactSet, Morningstar specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed February 14, 2026 with returns as of February 13, 2026 for Figure 2a and as of December 31, 2025 for Figure 2b. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: DEM, DGS, XSOE, WDAF.

Conclusion: The Toolkit Is Broader Than the Benchmark

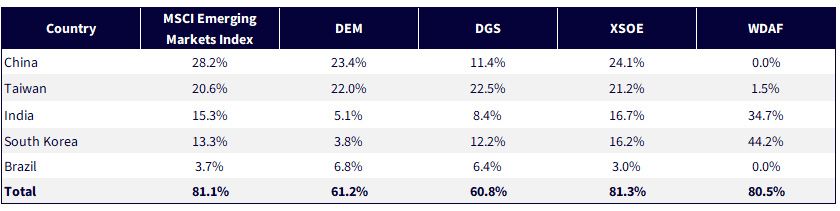

The MSCI Emerging Markets Index is structurally anchored by five primary economic exposures: China, Taiwan, India, South Korea and Brazil. Together, they dominate benchmark exposure and shape the narrative most investors internalize. But this figure shows that exposure is not static—it is a choice.

Different strategies redistribute that weight in meaningful ways. As we see in Figure 3, some dial down China. Some lean further into Taiwan. And some, like WDAF, meaningfully increase exposure to South Korea, while targeting a differentiated set of companies beyond the well-known memory chip manufacturers that typically define the country in global portfolios.

That matters. Because when leadership rotates, as it has, how you access a market can be just as important as whether you access it at all.

For U.S.-based investors accustomed to thinking in broad index terms, it’s worth recognizing that the emerging markets toolkit is far more nuanced than the headline benchmark suggests.

Figure 3: The Five Largest Economic Exposures within the MSCI Emerging Markets Index

Sources: WisdomTree, FactSet, Morningstar, with data as of January 31, 2026. Subject to change.

1 Source: MSCI. South Korea is measured by the MSCI South Korea Index universe.

2 Source: MSCI Emerging Markets Index Factsheet, as of January 31, 2026.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Funds invest in the securities included in, or representative of, its Index regardless of their investment merit, and the Funds do not attempt to outperform its Index. Please read the Funds’ prospectus for specific details regarding the Funds’ risk profile.

DEM: Investments in emerging, offshore or frontier markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation, intervention and political developments. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs.

DGS: Funds focusing on a single sector and/or smaller companies generally experience greater price volatility. Investments in emerging, offshore or frontier markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation, intervention and political developments. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. The securities of small-capitalization companies generally trade in lower volumes and are subject to greater and more unpredictable price changes than larger capitalization stocks or the stock market as a whole. Small-capitalization companies may be particularly sensitive to adverse economic developments as well as changes in interest rates, government regulation, borrowing costs and earnings. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time.

XSOE: Investments in emerging or offshore markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. Funds focusing their investments on certain sectors and/or regions increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility.

WDAF: Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Because the Fund invests primarily in the securities of companies in Asia, the Fund’s performance is expected to be closely tied to social, political, and economic conditions within Asia and to be more volatile than the performance of more geographically diversified funds. Many countries in the region have historically faced political uncertainty, corruption, military intervention, and social unrest. To the extent that such events continue in the future, they can be expected to have an unpredictable effect on economic and securities market conditions in the region and may impact the ability of the Fund to buy, sell or otherwise transfer securities and cause the Fund to decline in value. Investments in non-U.S. securities involve political, regulatory, and economic risks that may not be present in investments in U.S. securities. The Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended.

Categories

About the contributor

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.