WDAF

Asia Defense Fund

Published November 11, 2025

Global Head of Research

Macro Strategist, Model Portfolios

For most of the postwar era, global defense was a story anchored in Washington. The story was simple—American aircraft carriers patrol the seas, U.S. bases ring the globe and NATO1 allies benefit from the security umbrella. In that era, investors could get their defense exposure from a handful of primes—Lockheed, Raytheon, Northrop, Boeing and General Dynamics, to name a few2—assuming the rest of the world would continue outsourcing their defense sovereignty to the U.S.

That no longer holds.

The U.S. possesses unmatched military power, but its willingness to deploy that power abroad is not without limitations. Taiwan and Ukraine are not "on their own," but they cannot depend on overwhelming U.S. firepower as a backstop. Even NATO allies cannot be fully confident the U.S. will commit blood and treasure in the event of a skirmish in the Baltics. This is not about Trump or Biden, Democrats or Republicans—it is structural. America is strategically retrenching toward domestic priorities, and the rest of the world is being told to be able and willing to defend itself.

For Asia, the implications are potentially existential. Unlike the U.S., which is buffered by oceans, Asian powers are next to one another, often with clashing ideologies and contested borders. India and China are "emerging competitors" with different goals and worldviews. Japan and South Korea remain within missile range of North Korea. Taiwan lives under constant pressure from across the Strait.3 Australia must grapple with a militarized Indo-Pacific. In this geography, suspicion is natural. When the U.S. retreats from being the global police, neighbors put up more fences, install more cameras and buy more weapons.

This is why the Asia Defense theme is not about one flashpoint. It is not waiting for a Taiwan crisis. It is already happening, because the structural forces—geography, China's ambitions and U.S. retrenchment—make it inevitable.

This logically leads to a singular conclusion—countries will have to procure more weapons in the next 20 years than they did in the previous 20.4 That is not cyclical; it is secular.

The driver is not a political decision in Washington. China's rapid naval buildout, its space ambitions and its posture in the South China Sea leave its neighbors little choice. India, Japan, South Korea and Australia are rearming because of proximity. They share borders or waters with powers whose ambitions are global. And they cannot assume the U.S. will always be there.

That means Asian nations are not content to be customers. They are deliberately cultivating domestic champions—companies that can provide defense sovereignty without depending on external suppliers. This is why India insists on "Atmanirbhar Bharat" (self-reliance).5 Why Japan is rewriting its postwar constitution.6 Why South Korea is turning itself into a defense exporter. Why Australia has committed to AUKUS7 naval expansion.

Investors often look for catalysts. The more important framing here is inevitability. Whether or not Taiwan is ever attacked, the rearmament is underway.

Domestic Rearmament and Sovereignty8

Defense sovereignty begins with the ability to build one's own defense. India is perhaps the clearest example. Mazagon Dock Shipbuilders is turning out submarines and destroyers, giving the Indian Navy capabilities it cannot outsource. Hindustan Aeronautics (HAL) builds fighter jets, helicopters and drones—platforms India once bought abroad. Bharat Electronics fills in the nervous system of the military, supplying radars, communications and electronic warfare gear. India is shifting to being a producer, not a consumer.

Japan is at a different stage, but the direction is the same. Mitsubishi Heavy Industries (MHI) has become indispensable to Tokyo's defense push, from missile defense to submarines to next-generation fighters. Constitutional barriers that once prevented exports are being dismantled, and MHI is at the center of the change.

The logic is straightforward: when neighbors are uncertain and alliances are conditional, domestic champions are the only guarantee of sovereignty.

Missile Defense and Advanced Systems

The past few years have underscored that drones, missiles and hypersonics are not abstract threats. From Russian drone incursions in Eastern Europe to North Korean launches over Japan, the reality is clear: defense begins at interception and ends at impact.

South Korea has built formidable capabilities in this domain. Hanwha Systems and LIG Nex1 specialize in missile guidance, radars and integrated air defense. These firms not only serve Seoul but also win export contracts in Europe, where trust in U.S. timelines is fading. Korea Aerospace Industries (KAI) is pushing forward with the KF-21 fighter jet and a range of trainer aircraft, integrating missile systems and positioning South Korea as a credible supplier to Southeast Asia.

India complements this with Bharat Dynamics, which manufactures missiles across the spectrum—short-range tactical, air-to-air and strategic. Feeding into these programs, Data Patterns supplies avionics and subsystems critical for guidance and reliability.

Missile defense is not a hedge—it is the baseline insurance policy for any nation that shares a border with China or lives under North Korean threats. And Asian firms are increasingly the underwriters.

Naval Power and Indo-Pacific Maritime Security

Geography makes the sea the frontline. The Indian Ocean, the Taiwan Strait and the South China Sea are not distant theaters—they are vital arteries. Control of maritime lanes will determine the balance of power.

This is why naval contractors are at the heart of Asia's defense investment case. In India, Mazagon Dock and Cochin Shipyard are scaling capacity for submarines, destroyers and aircraft carriers. In South Korea, Hyundai Heavy Industries and Daewoo Shipbuilding are producing warships and submarines that serve both domestic fleets and export customers.

Australia's Austal has carved out a niche in high-speed patrol vessels and littoral combat ships, directly tied to AUKUS priorities. And in Japan, Kawasaki Heavy Industries supplies maritime patrol aircraft and submarines, now with greater export potential as restrictions ease.

Naval power is the steel backbone of Asia's deterrence strategy, and these shipyards are where that backbone is forged.

One of the more surprising dynamics is how quickly Asian defense firms are becoming exporters. European nations once reluctant to buy outside NATO now sign contracts with South Korean artillery makers. Southeast Asian navies are sourcing Indian patrol boats. Japan is preparing to enter the export market in earnest.

Hanwha exemplifies this shift, selling artillery and missile defense systems to customers far beyond South Korea's borders. India's HAL and Bharat Electronics are scaling exports into Southeast Asia, leveraging both cost advantages and political goodwill. Singapore Technologies Engineering maintains a global reputation in defense electronics and munitions.

Export momentum turns these firms from national champions into global suppliers, giving investors a growth vector that is not tied to a single country's budget.

Next-Gen and Emerging Defense Tech

Modern defense is not only about ships and missiles. Drones, satellites and space capabilities are shaping the future battlefield. Asia has no shortage of innovators.

Australia's Droneshield is producing counter-drone systems, a necessity as low-cost UAV swarms change the tactical environment. India's Paras Defence & Space Technologies works on optics and space components, while ideaForge supplies tactical drones already in use by Indian armed forces. South Korea's SATREC Initiative develops small satellites for surveillance, and Japan's Astroscale pioneers orbital debris removal—dual-use technology for space security.

These firms may look small compared to the shipyards and missile houses, but they represent the leading edge of Asia's defense buildout. They are the disruptors, offering investors exposure to capabilities U.S. primes do not fully capture.

Regional Alliances and Integration

Defense in Asia is not pursued in isolation. Alliances such as the Quad, AUKUS and bilateral defense pacts demand interoperability. That creates an advantage for firms that can deliver systems designed for multi-partner integration.

Singapore Technologies Engineering is a prime example, operating across domains and producing systems built for alliance environments. Hyundai Rotem manufactures tanks and armored vehicles that integrate with allied forces. Electro Optic Systems in Australia develops directed-energy weapons and space surveillance tools, tailored for joint operations. Even smaller firms like Poongsan and Woori Technology gain relevance by aligning to alliance standards.

In a multipolar Indo-Pacific, interoperability is not optional—it is a moat. Companies that deliver it will secure long-duration pipelines.

Skeptics point out that defense is nothing new. European defense equities have surged in price, and U.S. primes trade at premiums. But what looks expensive may in fact be cheap relative to the scale of the rearmament cycle.

Asia Defense is still in its early innings. The WisdomTree Asia Defense Fund (WDAF) only launched in September 2025. Meanwhile, India, Japan and Australia are at the front end of structural budget expansions.

The multi-decade nature of the cycle means investors are not late—they are early.

For U.S. investors, Asia Defense as a strategy offers three distinct advantages:

This is not a theme tied to the outcome of U.S. elections. China is not modernizing because of Trump or Biden. India is not building ships because of Capitol Hill debates. South Korea is not exporting missiles because of Washington's mood. These nations are responding to their own geography, and that is what makes the theme durable.

Defense is always political in the West. In Asia, it is geographic. The U.S. has oceans for moats. Asia has contested borders, shared seas and a neighbor with global ambitions. That reality guarantees demand for submarines, missiles, drones, satellites and everything in between.

The companies inside WDAF—HAL, Mazagon Dock, Bharat Electronics, Hanwha, KAI, Austal, Astroscale—are the industrial response to that reality. They are not speculative plays. They are the builders of sovereignty in a region where sovereignty cannot be outsourced.

For investors who believe in themes that compound over decades, Asia Defense is not a trade. It is the frontier of defense investing for the next 20 years.

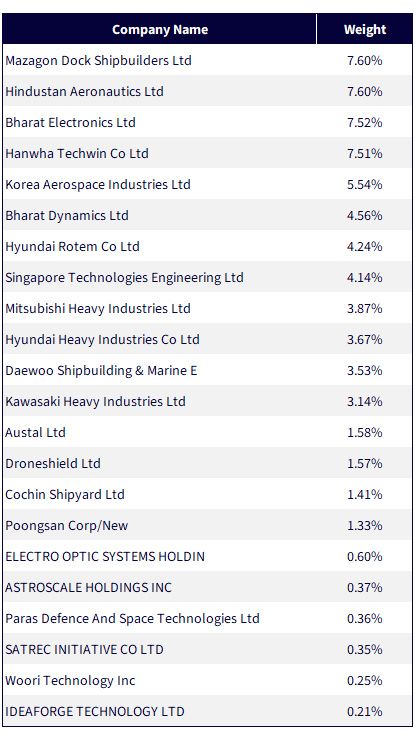

Figure 1: Exposure of Companies Mentioned in this Piece within WDAF

Source: WisdomTree Asia Defense Fund Holdings, as of 9/19/25. Holdings subject to change.

1 Refers to North Atlantic Treaty Organization.

2 Lockheed, Raytheon, Northrop, Boeing and General Dynamics had exposures of 5.34%, 5.14%, 5.10%, 4.81% and 5.17% within the WisdomTree Global Defense Fund, as of 9/19/25, but were not included in the WisdomTree Asia Defense Fund. Holdings subject to change.

3 Refers to the Taiwan Strait, where the mainland is China.

4 Source: C. Taylor, "The Cascade," pineconemacro.com, 9/5/25.

5 Source: Prime Minister's Office, "Atmanirbhar Bharat: The Foundation of a Strong and Developed India," pmindia.gov.in, 8/15/25.

6 Source: "Japan PM Calls for Speeding Up Debate on Revising Constitution," Kyodo News, 5/3/24.

7 Refers to Australia, U.K. and U.S.

8 Please look to figure 1 to see the exposure of these companies within the WisdomTree Asia Defense Fund as of 9/19/25. Holdings subject to change.

For current holdings of WDAF, please click here. Holdings are subject to risk and change.

There are risks associated with investing, including the potential loss of principal. Foreign investing involves specific risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Because the Fund invests primarily in the securities of companies in Asia, the Fund’s performance is expected to be closely tied to social, political and economic conditions within Asia and to be more volatile than the performance of more geographically diversified funds. Many countries in the region have historically faced political uncertainty, corruption, military intervention and social unrest. To the extent that such events continue in the future, they can be expected to have an unpredictable effect on economic and securities market conditions in the region and may impact the ability of the Fund to buy, sell or otherwise transfer securities and cause the Fund to decline in value. Investments in non-U.S. securities involve political, regulatory and economic risks that may not be present in investments in U.S. securities. The Fund invests in the securities included in, or representative of, its Index. The Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Asia Defense Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.