WDAF

Asia Defense Fund

Published September 12, 2025

Global Head of Research

Macro Strategist, Model Portfolios

The "peace dividend1" is over. What has emerged in its place is the "production dividend," a global rebuilding of arsenals, industrial bases and the software-defined systems that now shape modern deterrence. Wars consume faster than peacetime models predicted. Democracies are rearming, stockpiles are being rebuilt and factories are scaling under government-backed contracts.

This cycle is not a one-off event. It is a multiyear industrial program spanning continents, creating durable runways for defense companies and investable opportunities for long-term portfolios.

As of today, WisdomTree has two additional strategies designed to provide targeted exposure to this trend:

Together with the WisdomTree Europe Defense Fund (WDEF), they provide both regional and broad access to the businesses building the arsenals of the 21st century.

Global defense is being reshaped by three forces:

1. Consumption shocks: Ukraine fired more artillery in two days than the U.S. once produced in a month, exposing critical planning gaps.

2. Allied rearmament: Europe has broken fiscal taboos, Japan is remilitarizing, Australia is embedding supply chains and India is accelerating domestic champions.

3. Technology turnover: Cheap drones, advanced sensors and software-driven warfare are displacing legacy procurement models.

This wave is years in the making. Rheinmetall has expanded ammo capacity tenfold. RTX anchors air defense. L3Harris secured the bottleneck of solid rocket motors. Even "dull" parts of the supply chain like fuses, propellants and warheads now determine who can deliver.

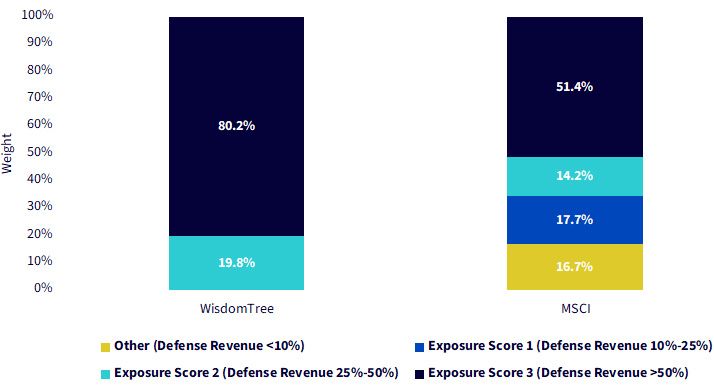

The WisdomTree Global Defense Fund (WDGF), which is designed to track the WisdomTree Global Defense Index, captures this secular growth by focusing on companies with at least 50% of revenues from defense activities, with far higher exposure than traditional benchmarks. It is a strategy aligned with deterrence as a service: missiles that hit, sensors that see, software that decides and satellites that connect.

Source: WisdomTree, FactSet. Holdings as of 3/31/25. WisdomTree refers to WisdomTree Global Defense Index. MSCI refers to the MSCI ACWI Aerospace & Defense Index. Defense revenue exposure is sourced from multiple in-house and external sources. Data is as of the most recent rebalancing screen. Exposure Score 1 = Companies with defense revenue between 10%–25%. Exposure Score 2 = Companies with defense revenue between 25%–50%. Exposure Score 3 = Companies with defense revenue greater than 50%. You cannot invest directly in an index.

If Europe's wake-up call came first, Asia's response is now accelerating. South Korea, India and Japan sit at the heart of the region's transformation.

These programs are not temporary. Backlogs stretch years, exports diversify revenue streams and governments co-fund capacity expansions, turning cyclical manufacturing into something closer to utility-like cash flows.

The WisdomTree Asia Defense Fund (WDAF) is designed to track the WisdomTree Asia Defense Index, a strategy built to capture this regional surge. While global benchmarks underrepresent Asia's defense revenues, this Fund helps ensure investors gain direct access to Asia's defense industrial buildout.

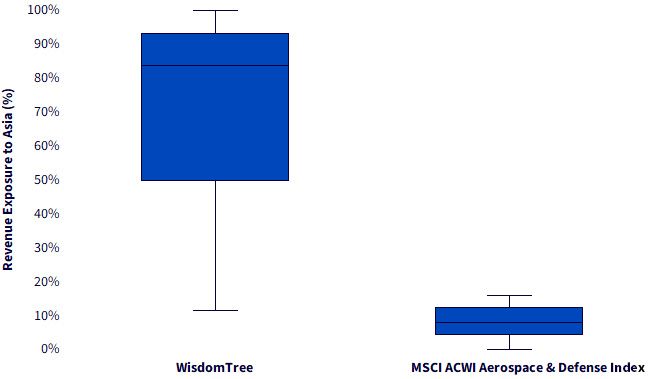

Figure 2: Asia's Defense Surge: Exposure That Leaves the Global Benchmark Behind

Sources: WisdomTree, FactSet. Data is as of 7/31/25. WisdomTree refers to the WisdomTree Asia Defense Index. The blue boxes reference the middle 50% of the index exposure, whereas the lower whisker shows the range of the lowest 25% and the higher whisker shows the range of the highest 25%. The dark line in the blue represents the weighted average. The chart plots revenues from defense activities in Asia. Subject to change. You cannot invest directly in an index.

What Makes the WisdomTree Defense Suite Compelling?

The investable buildout is happening inside the U.S. alliance system and its closest partners. And all three strategies are about more than headlines. They are about owning bottleneck capacity, recurring electronics/software refresh and long-term backlog visibility. In short: owning the arsenal, not the headline.

The WisdomTree defense strategies are built on principles of clarity and precision:

These Funds are designed for investors seeking a rare combination: secular growth, government-backed end customers, global diversification and technology curves still bending upward.

The rebuilding of arsenals is not an abstract forecast. It is happening now—measured in contracts signed, plants expanded and backlogs stretching for years. With the addition of the WisdomTree Global Defense Fund and the WisdomTree Asia Defense Fund to our defense suite, investors can gain targeted, disciplined exposure to the companies at the heart of this historic industrial shift.

Deterrence is becoming a service. These Funds are designed to help investors own the providers of that service from Washington to Warsaw, from Busan to Bengaluru.

1 "Peace dividend," Fortune, 1968. This is often cited as the first use of this term.

For current holdings, please click the respective ticker: WDGF, WDAF. Holdings are subject to risk and change.

WDGF: There are risks associated with investing, including the potential loss of principal. Foreign investing involves specific risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. To the extent the Fund invests a significant portion of its assets in securities of companies of a single country or region, it is more likely to be impacted by events or conditions affecting that country or region. Investments in non-U.S. securities involve political, regulatory and economic risks that may not be present in investments in U.S. securities. Investments in non-U.S. securities may be subject to risk of loss due to foreign currency fluctuations, political or economic instability, or geographic events that adversely impact issuers of foreign securities. Investments in non-U.S. securities also may be subject to withholding or other taxes and may be subject to additional trading, settlement, custodial and operational risks. These and other factors can make investments in the Fund more volatile and potentially less liquid than other types of investments. These risks may be heightened to the extent the Fund invests in companies domiciled in or otherwise tied to developing or emerging market countries. The Fund invests in the securities included in, or representative of, its Index. The Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

WDAF: There are risks associated with investing, including the potential loss of principal. Foreign investing involves specific risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Because the Fund invests primarily in the securities of companies in Asia, the Fund’s performance is expected to be closely tied to social, political and economic conditions within Asia and to be more volatile than the performance of more geographically diversified funds. Many countries in the region have historically faced political uncertainty, corruption, military intervention and social unrest. To the extent that such events continue in the future, they can be expected to have an unpredictable effect on economic and securities market conditions in the region and may impact the ability of the Fund to buy, sell or otherwise transfer securities and cause the Fund to decline in value. Investments in non-U.S. securities involve political, regulatory and economic risks that may not be present in investments in U.S. securities. The Fund invests in the securities included in, or representative of, its Index. The Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.