The Case for Local Currency and Active Management in a Softening Dollar Environment

Published March 3, 2026

Global Head of Research

Director of Market Strategy

Key Takeaways

- With the U.S. dollar weakening in 2025 and early 2026, local currency emerging market debt has surged toward 20% returns, outpacing hard currency peers closer to 15%, making active local exposure through the WisdomTree Emerging Markets Local Debt Fund (ELD) increasingly compelling in a shifting macro regime.

- After more than a decade in which dollar-denominated EM debt delivered roughly 60% cumulative returns versus less than 20% for local currency strategies amid a 40% rise in the dollar, the pivot toward Fed easing and softer FX trends is now flipping leadership back to local markets.

- In this new environment, active country allocation has mattered, as ELD has outperformed its largest passive local currency peer across YTD, 1-year, 5-year and 10-year periods by overweighting higher-carry Latin America and avoiding structural laggards such as China, underscoring why ETF selection is as critical as the asset class itself.

If we look at the biggest ETFs in the Morningstar Emerging Markets Bond category, measured by assets under management (AUM), we see two giants exemplifying this:

- iShares J.P. Morgan USD Emerging Markets Bond ETF (EMB), $15.9 billion.

- Vanguard Emerging Markets Government Bond Index Fund (VWOB), $5.9 billion.

Conversely, if we look for the biggest ETF by AUM that generates exposure to local currency emerging markets bonds, we find:

- VanEck J.P. Morgan EM Local Currency Bond ETF (EMLC), $5.2 billion.

Two Potential Surprises for Investors

A granular analysis of the performance data from both a recent period, 2025 and early 2026, as well as a longer period back to 2013, reveals a distinct bifurcation on two distinct levels we will explore in this piece:

- Local currency debt, recently, has rather dramatically outperformed hard currency debt.

- Within the local space, active management, exemplified by the WisdomTree Emerging Markets Local Debt Fund (ELD), has been able to generate consistent outperformance relative to EMLC.

We can use the WisdomTree Bloomberg U.S. Dollar Bullish Fund (USDU) as a way to bring context to these questions, marrying analysis of the emerging markets bond asset class with a view on performance of the U.S. dollar.

Point 1: Surprise—Local Currency Emerging Market Debt has been Outperforming

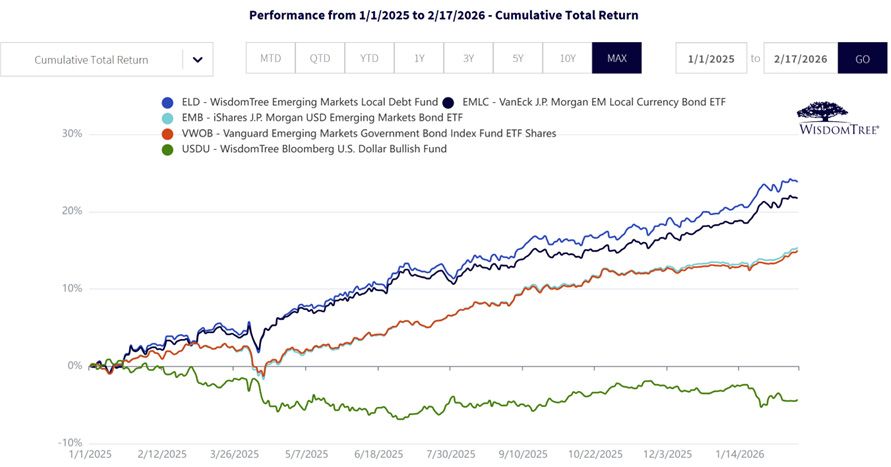

For many U.S.-based investors, emerging markets bonds can feel like a black box. Returns are shaped not only by credit risk and interest rates, but also by currency movements that don’t always show up clearly in traditional performance snapshots. Distinguishing between hard currency and local currency debt adds another layer of complexity. Yet beneath that complexity, leadership has emerged, as local currency bonds have been doing much of the heavy lifting performance-wise, at least since early 2025.

In Figure 1a, we see this as both ELD and EMLC (local currency strategies) have opened up a performance advantage against EMB and VWOB (hard currency strategies). It’s important to note that, over this period, the return of USDU was negative, telling us that the overall environment was that of a ‘weak U.S. dollar.’

Figure 1a: Recent Outperformance of Emerging Markets Local Currency Debt

Figure 1b: Standardized Performance

Sources: WisdomTree, FactSet, Morningstar specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed February 19, 2026 with returns as of February 17, 2026 for Figure 1a and as of December 31, 2025 for Figure 1b. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: ELD, USDU, EMLC, EMB, VWOB.

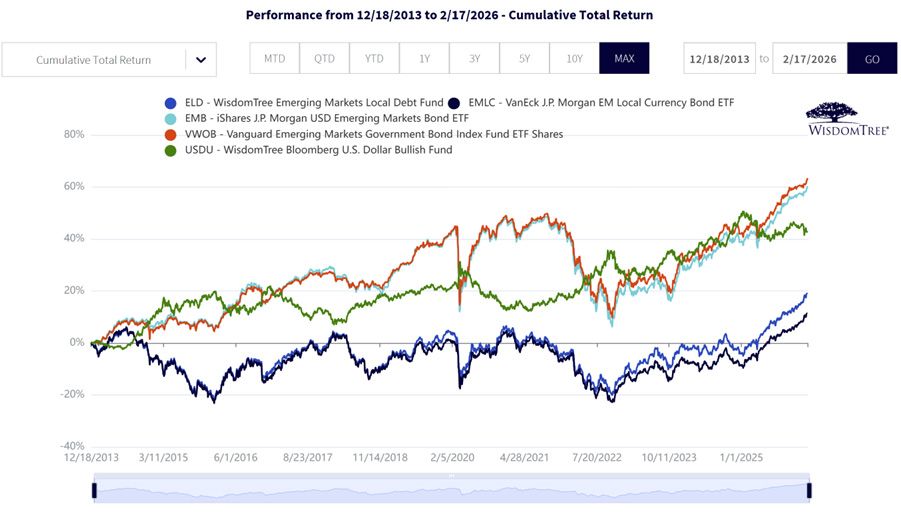

The Hard Currency Trap and the Macro Pivot

To understand the current opportunity, one must first understand the inertia of the past. Looking back over a common period dating back to 20131, EMB and VWOB, the U.S. dollar denominated exposures, delivered much stronger performance than their local currency peers, EMLC and ELD. As we see in Figure 2:

- The cumulative returns of EMB and VWOB were in the neighborhood of 60% over this period.

- By comparison, the cumulative returns of ELD and EMLC were below 20%.

- Remembering that we have to maintain cognizance of the performance of the U.S. dollar, we see that USDU's return over this same period was in the neighborhood of 40%.

In our view, this disparity solidified the dominance of USD-based funds in investor portfolios. When the dollar is strong, the currencies of emerging markets depreciate, eroding the returns of local-currency bonds when converted back to dollars. For years, avoiding currency risk was the winning trade.

Figure 2: A Period where Hard Currency Exposures Outperformed

Sources: WisdomTree, FactSet, Morningstar specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed February 19, 2026 with returns as of February 17, 2026. NAV denotes total return performance at net asset value. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: ELD, USDU, EMB, VWOB.

Currency Return Behavior Can Fluctuate

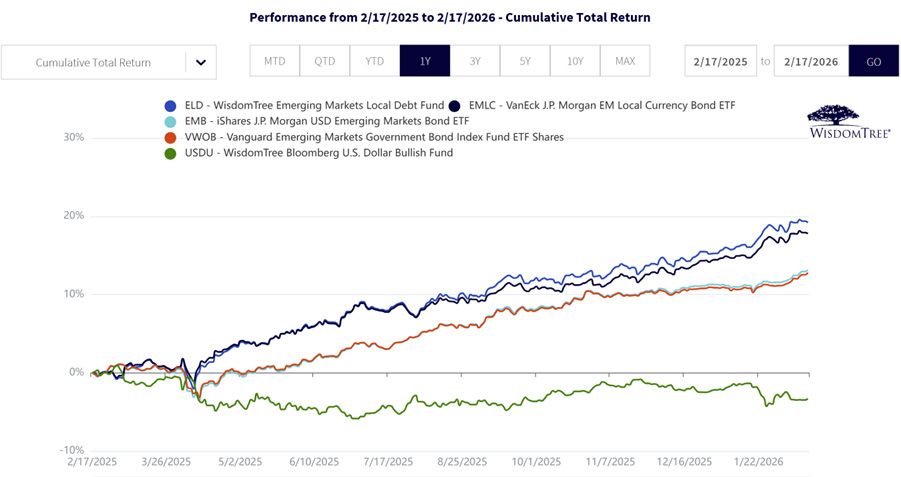

In Figure 3, we look instead at the latest 1-Year period ended February 17, 2026. The reason we do this is that we are focusing on a period where the performance of the U.S. dollar shifted from that of strength to that of weakness—seen in the Figure as a negative cumulative return for USDU. The results of this shift are stark:

- ELD and EMLC became the performance leaders, with cumulative returns pushing towards, but not quite reaching 20%.

- EMB and VWOB became the performance laggards, with cumulative returns pushing towards, but not quite reaching 15%.

The message from the market is clear: the ‘more obvious’ exposure of the last decade has become the underperforming exposure of the current recovery. We use ‘more obvious’ to reflect investors’ tendency to extrapolate performance trends indefinitely, frequently forgetting that ‘past performance is not indicative of future results.’

It is also worth noting that if the local currency ETFs mentioned here are pushing towards 20% for this period and the hard currency ETFs mentioned here are pushing towards 15%, it’s telling us that the overall asset class, Emerging Markets Bonds, is showing some real strength.

Figure 3: When Local Currency Strategies Started Outperforming

Sources: WisdomTree, FactSet, Morningstar specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed February 19, 2026 with returns as of February 17, 2026. NAV denotes total return performance at net asset value. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance and to download the respective Fund prospectuses, click the relevant ticker: ELD, USDU, EMB, VWOB.

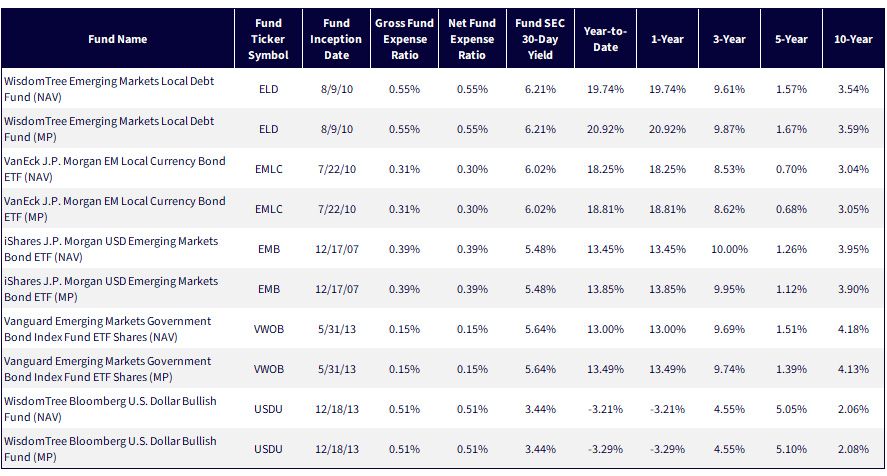

Point 2: Active vs. Passive, Why ELD is Beating EMLC

Once an investor accepts the premise that local currency debt may be a compelling place to be, the next decision is the vehicle. The largest product in the Morningstar Emerging Markets Bond category that provides exposure in local currency is the VanEck J.P. Morgan EM Local Currency Bond ETF (EMLC), a passive fund tracking an index. However, in the complex world of emerging markets, passive indexing often exposes investors to troubled economies simply because those countries issue a lot of debt.

That point bears repeating, but phrased as a question: Does it make sense to put the most weight within a fixed income strategy into the entity issuing the most debt?

This is where the distinction between ELD and EMLC becomes critical. ELD utilizes an active approach that allows for strategic deviations from the standard indices. As of early 2026, ELD has maintained a strategic overweight in Latin American issuers, specifically Brazil, Colombia, and Peru, while underweighting Asia and EMEA relative to the index. This positioning has been prescient. Latin American issuers have offered higher yields with better fundamentals than their counterparts in other regions.

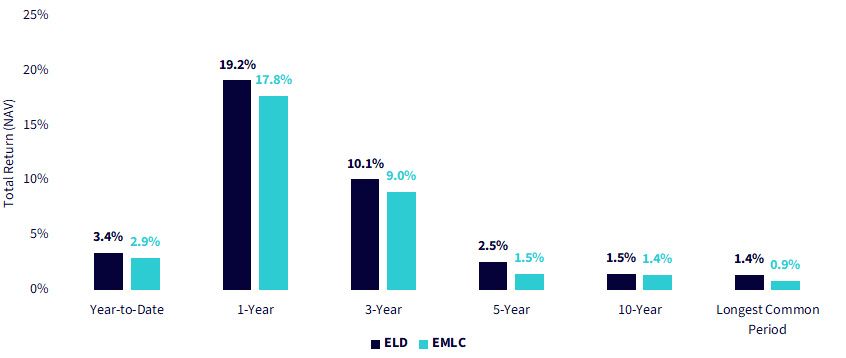

In Figure 4, we wanted to combine a look at recent periods, such as ‘year-to-date 2026’ and ‘1-year’ with looking at longer periods, such as 5 years and 10 years. We wanted to test the robustness of any performance differences between ELD and EMLC over numerous time horizons.

We see that, for the time periods shown, ELD outperformed EMLC in all of them. One should recognize that this can always change in the future, but one can also be impressed at this historical consistency.

Figure 4: ELD has Generated Consistent Outperformance over EMLC

Sources: WisdomTree, FactSet, Morningstar specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed February 19, 2026 with returns as of February 17, 2026. NAV denotes total return performance at net asset value. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance and to download the respective Fund prospectuses, click the relevant ticker: ELD, EMLC.

A look at country exposure further illustrates the difference. EMLC holds an 8.9% weighting in China, a market that has faced significant structural headwinds. ELD, by contrast, does not list China among its top exposures, instead allocating significant weight to high-carry2 nations like Indonesia (11.8%) and Brazil (8.2%). This ability to sidestep the drag of underperforming heavyweights in the index is a distinct advantage of the active methodology. While we could never say this will always be the case, it’s important to recognize differences in returns and underlying drivers of historical periods.

Fundamentals and Future Outlook

The case for ELD is not merely backward-looking; it is supported by improving fundamentals across the emerging market landscape. Inflation in most EM countries has trended lower, staying within stable ranges, which preserves the real value of the yields offered by local bonds. Additionally, external balances are well-contained, and growth has held up well.

The currency argument remains the linchpin. We have seen a "Liberation Day" from the pressures of the strong dollar. The recent strengthening of the Japanese yen against the dollar is another constructive signal for emerging markets, as a stronger yen historically weighs on the broad dollar index, easing financial conditions for EM economies.

Conclusion

The period of so-called ‘blind devotion’ to USD-denominated emerging market debt ETFs should be over. The macroeconomic environment that fueled the dominance of EMB and VWOB—specifically, a relentlessly strengthening U.S. dollar—has reversed. In this piece, we are challenging people to recognize this shift and not shelter their thinking in longer-run periods that might mute the impact of more recent trends. We believe we are now in a period characterized by Federal Reserve easing and improving EM fundamentals, a combination that historically ignites local currency debt returns.

Within this resurgent asset class, investors should be wary of treating all products as equivalent. The largest local currency ETF, EMLC, exposes investors to the rigidities of passive indexing, forcing them to own underperforming regions. In contrast, ELD offers a nimble, active approach that has proven its worth by capitalizing on the high-yield opportunities in Latin America while avoiding the pitfalls of Asia. With superior alpha generation, higher yield, and significantly stronger recent returns, ELD may represent a compelling option for investors seeking exposure to the shift in emerging markets.

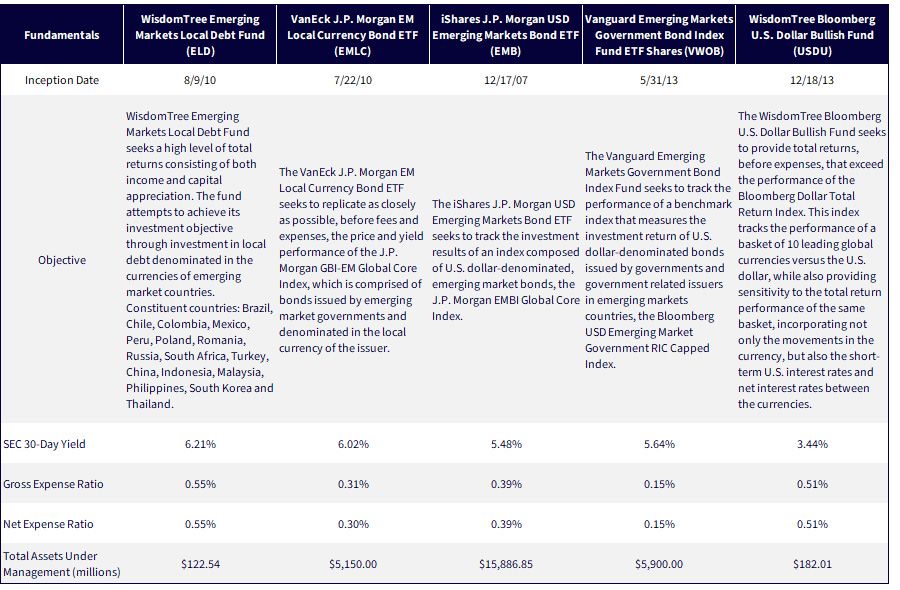

Figure 5: Additional Information

Sources: Respective fund company ETF pages on different websites, with assets under management current as of February 18, 2026. Subject to change.

1 The longest common period is defined by the inception date of USDU: 12/18/2013.

2 High carry refers to countries where the interest rate is high relative to the interest rate for the investor, in this case the U.S. If Indonesia is ‘high-carry’ that means that Indonesia’s interest rates are higher than those of the U.S.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Investments in emerging, offshore or frontier markets are generally less liquid and less efficient than developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effects of varied economic conditions. Please read the Funds’ prospectus for specific details regarding the Funds’ risk profile.

ELD: Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. In addition, when interest rates fall income may decline. Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner, or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs.

USDU: The Fund focuses its investments in specific regions or countries, thereby increasing the impact of events and developments associated with the region or country, which can adversely affect performance. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. While the Fund attempts to limit credit and counterparty exposure, the value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. The Fund’s investment in repurchase agreements may be subject to market and credit risk with respect to the collateral securing the repurchase agreements and may decline prior to the expiration of the repurchase agreement term. Issuer specific events, including changes in the actual or perceived financial conditions of an issuer, can have a negative impact on the value of the Fund. Due to the investment strategy of the Fund, it may make higher capital gain distributions than other ETFs. Although the Fund invests in very short-term, investment grade instruments, the Fund is not a "money market" Fund, and it is not the objective of the Fund to maintain a constant share price. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index.

For additional fund disclosures, please click the respective ticker: EMLC, EMB, VWOB.

About the contributors

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Director of Market Strategy

Jonathan Flynn serves as Director of Market Strategy at WisdomTree, helping bridge research, product strategy, distribution and investor engagement through data-driven market insights and thematic storytelling.

He brings more than 25 years of experience working with leading wealth management teams and advisors, with deep expertise in investor behavior, ETF trends, market flows and behavioral finance. Jonathan specializes in identifying emerging themes early, translating complex ideas into compelling investment narratives and helping investors better understand the intersection of sentiment, positioning and long-term opportunity.

His work is grounded in the belief that understanding investor behavior and crowd dynamics can help uncover tomorrow’s investment opportunities before they become consensus.