Closing the Curtain on Rate Cuts

Published July 8, 2026

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Key Takeaways

- Although the June’s jobs report revealed some moderation in new hiring, it reinforced the view that the labor market is still a positive contributor and closed the curtain on rate cuts

- With inflation still above target, the money and bond markets have clearly shifted monetary policy expectations for Fed rate hikes later this year.

- In this environment, a barbell strategy combining zero- or ultra-short-duration exposures with core bonds remains a disciplined approach to balancing income opportunities with interest rate risk.

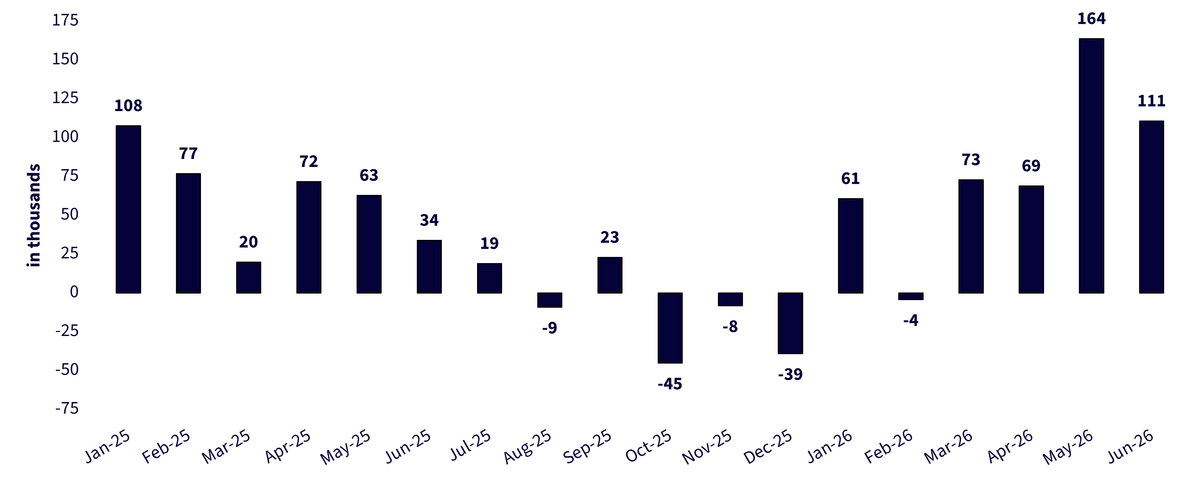

The June jobs report underscored our thesis that while the labor market remains in the 'economic plus column,' some of the prior months' increases in new hiring seemed a bit too high. Right on cue, the Bureau of Labor Statistics (BLS) reported that total nonfarm payrolls rose less than expected and that the prior two months’ gains were revised downward (see Figure 1). Moderate real gross domestic product growth, above Fed-target inflation and Warsh & Co. on hold are our primary themes for the second half of 2026 and this employment report plays right into those scenarios. Here are some key takeaways:

- Total nonfarm payrolls rose +57,000 or only about half of the consensus estimate while the prior two months’ gains were revised downward by -74,000. That places the ‘new’ 3-month moving average tally at +111,000, a bit more in line with what we expect going forward.

Figure 1: U.S. Total Nonfarm Payrolls – 3-Month Moving Average

Source: Bureau of Labor Statistics, as of July 2, 2026.

- The unemployment rate dropped -0.1 percentage point to 4.2% but this decrease contained a lot of noise—the civilian labor force, employment and unemployment readings all declined in a visible fashion

- This jobs report is not a gamechanger for Treasury yields and supports our Treasury 10-year yield call of maintaining a 4.00%–4.50% range, with the potential for occasional ‘overshoots’. The U.S. Treasury 2-year yield is still pricing in at least one rate hike

- The U.S. Treasury 2-year/10-year yield curve steepened by +10 basis points post-jobs

No Curtain Call for Warsh & Co.

- This jobs report should knock out all of the ‘Crazy Talk’ about a July rate hike. Fed funds futures still have December for the timing of the first rate hike, but October is also ‘in play’

- As mentioned above, we see the Fed on hold for the remainder of this year, the curtain has been closed for rate cuts

Bottom Line: The Barbell

With the curtain being closed for rate cuts (unless something dramatically unexpected were to occur), fixed income investors will be facing a money & bond market outlook that will more than likely continue to vacillate between the Fed being ‘on hold’ or potentially moving towards a rate hike as the second half of the year unfolds. We continue to advocate a fixed income strategy that does not ‘chase’ duration but rather utilizes the time-tested barbell approach. Our recommended barbell consists of a cornerstone allocation that emphasizes zero- or ultra-short-duration being paired with a weighting to a core bond position.

Categories

Related articles

Fed Watch: The Changing of the Guard Finally Arrives

Private Credit Beyond the Headlines: Why Diversification and Liquidity Matter More Than Ever

Are Bessent’s Hands Tied?

‘Warsh’ and Dry

What’s ‘Under the Hood’ of Your Core Bond Position?

Powell Stays…Should the Dot Plot?

Fed Watch: Powell’s Last Stand & What Comes Next?

Inflation’s First Official Debut

Nowhere to Hide…Except Maybe Treasury Floating Rate Notes

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.