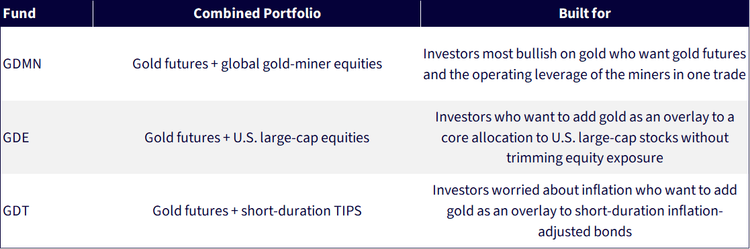

GDMN

Efficient Gold Plus Gold Miners Strategy Fund

Published July 7, 2026

Global Chief Investment Officer

After a historic run that carried gold above $5,500, the metal spent roughly five months giving some of its large move back, printing a low near $3,959 in late June. A cluster of signals my friend at MacroCharts.com (MC) has been writing about suggests gold appears to be completing a textbook capitulation—in time, price, positioning, sentiment and flows all at once.

What makes the setup worth a serious look is the asymmetry.

1. Price Is Testing the Exact Window for a Turn

Gold’s pullback has landed inside a cycle “turn window” that MC flagged in advance (the vertical lines), and it did so right on a price shelf around $3,950–$4,000. The recent low of $3,959 sits almost exactly on that level, and price has so far refused to follow through lower—the “bear trap reversal” annotation. The structure is nearly identical to prior historic turns.

The point isn’t the upside target, it’s that the downside is tightly defined while the potential payoff is not.

Gold price, cycle turn window (vertical lines), and the bear-trap reversal at the $3,950–$4,000 shelf. Period is from November 14, 2025 to July 1, 2026. Source, as stated, is MacroCharts.com. Past performance is not indicative of future results.

2. The Forces Behind the Bottom Call

What elevates this from “a level held” to “a turn worth respecting” is that four largely independent forces appear to have capitulated together.

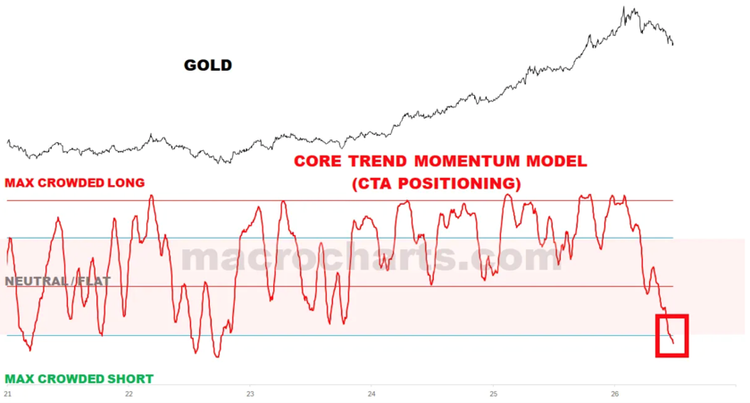

Positioning has flushed. MacroChart’s Core Trend Momentum Model—a proxy for commodity trading advisor (CTA) and trend-follower positioning—has collapsed from crowded-long toward Max Crowded Short. In plain terms, the systematic sellers who pile pressure on a falling market have already sold. That removes a major potential source of mechanical downside, and it is the kind of reading that has historically lined up with exhaustion of selling pressures.

Core Trend Momentum Model (CTA positioning) has plunged toward the Max Crowded Short extreme. Period is from January 2021 to June 30, 2026. Past performance is not indicative of future results.

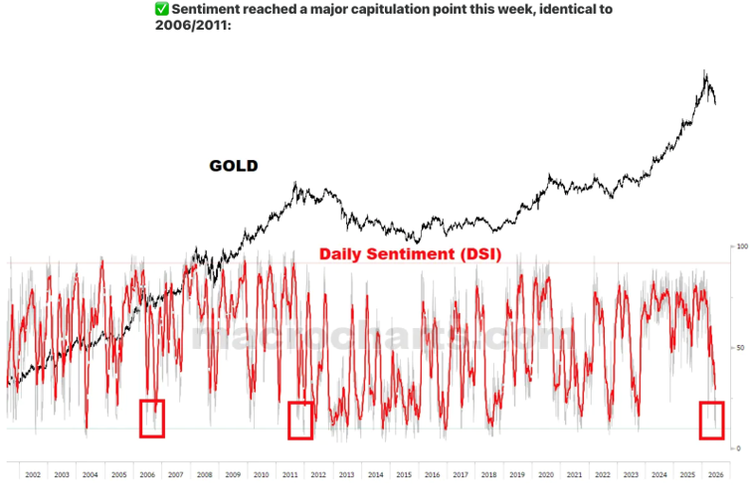

Sentiment has capitulated to levels last seen at major bottoms. Daily Sentiment (DSI) for gold and silver plunged to 10—a full-blown washout that lines up against the 2006 and 2011 lows, two of the more durable bottoms of the modern gold era. The mood shift matters as much as the number: five months ago, at the highs, “debasement” was the consensus trade; today it is openly mocked, with the dollar declared a one-way bet higher. That 180-degree reversal in narrative is itself classic bottoming behavior.

Daily Sentiment (DSI) capitulation today mirrors the 2006 and 2011 major bottoms. Period shown from November 2001 to June 30, 2026. Past performance is not indicative of future results.

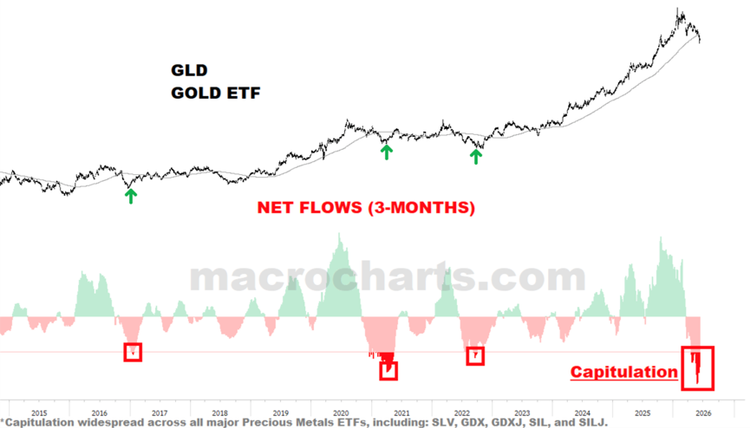

Flows have washed out across the complex. Three-month net flows into the broader precious-metals (PM) ETF complex have swung to capitulation, matching the troughs that preceded prior advances. Once the marginal holder has finished selling, the supply overhang that drives a downtrend tends to clear.

GLD three-month net flows have reached capitulation, with the washout widespread across the PM ETF complex. Period shown from November 2014 to June 30, 2026. Past performance is not indicative of future results.

Price action is starting to confirm. Finally, the tape is beginning to diverge constructively: some of the miner-related equities have not confirmed gold’s latest lows and several of these ETFs are printing what technicians refer to as “inverted hammers”—an exhaustion candle and signal sometimes seen at important bottoms.

3. Putting It Together

Any one of these signals in isolation is noise. The reason the setup merits attention is the confluence: cycle timing, a defended price shelf, flushed positioning, capitulated sentiment, washed-out flows, and the first hints of positive price divergence, all arriving in the same window, and all rhyming with 2006 and 2011. That does not guarantee that the low is in. It does mean the risk-reward has shifted meaningfully—and, in the end, that asymmetry is the only thing that ever really matters.

Expressing the View: Capital-Efficient Gold Solutions

For investors who find the setup compelling, the practical question is how to add gold without giving up the exposures already doing work in a portfolio. WisdomTree’s capital-efficient suite is designed to add gold as an overlay to a portfolio sleeve, creating room without requiring investors to sell an important asset.

WisdomTree Capital-Efficient Gold ETFs

GDMN refers to the WisdomTree Efficient Gold Plus Gold Miners Strategy Fund, which is a strategy designed to provide exposure to 90% equities of gold mining companies, 10% short-term U.S. treasuries to serve as collateral for a position that provides 90% notional exposure to gold futures. For each hypothetical $100 invested, there is $180 of notional exposure. GDE refers to the WisdomTree Efficient Gold Plus Equities Strategy Fund, which is a strategy designed to provide exposure to 90% equities of the 500 largest U.S. companies by market capitalization, 10% short-term U.S. treasuries to serve as collateral for a position that provides 90% notional exposure to gold futures. For each hypothetical $100 invested, there is $180 of notional exposure. GDT refers to the WisdomTree Efficient Gold Plus TIPS Strategy Fund, which is a strategy designed to provide exposure to 90% U.S. Treasury Inflation Protected bonds, 10% short term U.S. treasuries which serve as collateral for 90% notional exposure to gold futures.

Each fund uses U.S.-listed gold futures—collateralized by the fund’s core holdings—to layer roughly 90% notional gold exposure on top of an existing ~90% allocation, for about 1.8x total asset exposure per dollar invested.

Because the gold sits on top of the large-cap equity, gold miners, or TIPS sleeve rather than replacing it, an investor can introduce a meaningful gold position without selling down the stocks or bonds they already own.

The Case for the Baskets:

Unless otherwise stated, the source for this piece, including all technical charts, is MacroCharts.com. See the full market research and analysis on Substack.

There are risks associated with investing, including possible loss of principal. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

GDMN: The Fund is actively managed and invests in U.S.-listed gold futures and global equity securities issued by companies that derive at least 50% of their revenue from the gold mining business (“Gold Miners”). The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. By investing in the equity securities of Gold Miners, the Fund may be susceptible to financial, economic, political, or market events that impact the gold mining sub-industry, including commodity prices and the success of exploration projects. The Fund may invest a significant portion of its assets in the securities of companies of a single country or region, including emerging markets, and thus, the Fund is more likely to be impacted by events and political, economic, or regulatory conditions affecting that country or region, or emerging markets generally. While the Fund is actively managed, the Fund’s investment process is heavily dependent on quantitative models and the models may not perform as intended.

GDE: The Fund is actively managed and invests in U.S. listed gold futures and U.S. equity securities. The Fund’s use of U.S. listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. While the Fund is actively managed, the Fund's investment process is heavily dependent on quantitative models and the models may not perform as intended.

GDT: The Fund invests in a portfolio composed of Inflation-protected U.S. Treasury Bonds (“TIPS”) and U.S. listed gold futures contracts. The interest and principal payments of TIPS are adjusted for inflation and typically have lower yields than conventional fixed-rate bonds. The Fund’s income from TIPS may decline due to deflation or changes in inflation expectations. The value of gold and commodity-linked derivative instruments such as gold futures contracts typically is based upon the price movements of the physical commodity or an economic variable linked to such price movement. Price movements in gold and gold futures contracts may fluctuate quickly and dramatically, have a historically low correlation with the returns of the stock and bond markets. Derivatives are used by the Fund to gain exposure to inflation swaps and U.S. listed gold future contracts. Derivative investments can be volatile and may be less liquid than other investments. As a result, the value of an investment in the Fund may change quickly and without warning you may lose money. While the Fund is actively managed, the Fund's investment process is heavily dependent on quantitative models and the models may not perform as intended.

Global Chief Investment Officer

Jeremy Schwartz has served as Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Behind the Markets podcast. Jeremy is a member of the CFA Society of Philadelphia.