WDRN

Physical AI, Humanoids, and Drones Fund

Published July 6, 2026

Global Head of Research

When Barron's devotes its cover story to drones, as it did over the weekend from June 27 and 28th, 2026, investment professionals take notice. The piece, titled "Cheap Drones Are Upending the Defense Sector," is not a speculative technology preview.1 It is a dispatch from an active revolution. Cheap unmanned systems have already demonstrated the ability to hold superpowers at bay, neutralize $30 million tanks with $5,000 quadcopters, and force powerful countries to negotiating tables.

The implications for defense investment are structural, not cyclical.

For investors, the WisdomTree Physical AI, Humanoids, and Drones Fund (WDRN) deserves a closer look. Several of the companies Barron's singles out as ‘battle-tested leaders’ are names already inside the fund. Also, the broader analytical framework the article advances, which such criteria as battlefield credibility as the new gold standard, antidrone as the equal and opposite force, and supplier picks-and-shovels as the most durable layer of the stack, maps almost directly onto critical ideas within the strategy.

The 'Battle-Tested' Standard

The Barron's piece advances a standard that should resonate with any serious investor in this space:

companies whose systems have actually been deployed in Ukraine are likely to represent some of the strongest investment opportunities in the drone sector.

It makes sense that battlefield deployment is the ultimate proof-of-concept, and that it is more rigorous than any laboratory test, and more demanding than any government evaluation process. The drone landscape today includes dozens of publicly traded companies making compelling claims. What separates those claims from demonstrated capability is the crucible of actual combat.

By that standard, we can look to four publicly traded companies that were directly mentioned:

Two of those four, AeroVironment and Red Cat Holdings, are current holdings in WDRN. AeroVironment has been a fixture in military unmanned systems for decades; its Switchblade loitering munition has been among the most discussed systems in the Ukraine conflict. Red Cat, through its Black Widow micro-drone, has become a go-to platform for small unit reconnaissance in contested environments.

The two Barron's picks not, presently, in WDRN, Aevex and Swarmer, are both very recent initial public offerings (IPOs). Aevex, maker of the Phoenix Ghost kamikaze drone, went public in April 2026. Swarmer, which builds AI-driven command-and-control software for autonomous drone swarms, went public in March 2026. Both companies are compelling additions to the conversation around battlefield-proven drone technology, and both will be evaluated as part of WDRN's next scheduled quarterly rebalance in August 2026. That process is precisely how the index methodology is designed to work, identifying and incorporating emerging leaders as their track records and liquidity profiles mature. It is entirely possible that one or both names could be included at that point.

The Other Half of the Battle: Antidrone and Counter-Unmanned Aircraft System (UAS)

One of the more underappreciated angles in the Barron's piece was its treatment of antidrone technology. As the article noted, drones have created their own demand signal on the defensive side. Radar jamming, edge computing that severs global positioning system (GPS) links, directed-energy weapons, and drone interceptors are all growing alongside the offensive drone market itself. This isn't a niche, and it is becoming as commercially significant as the platforms it counters.

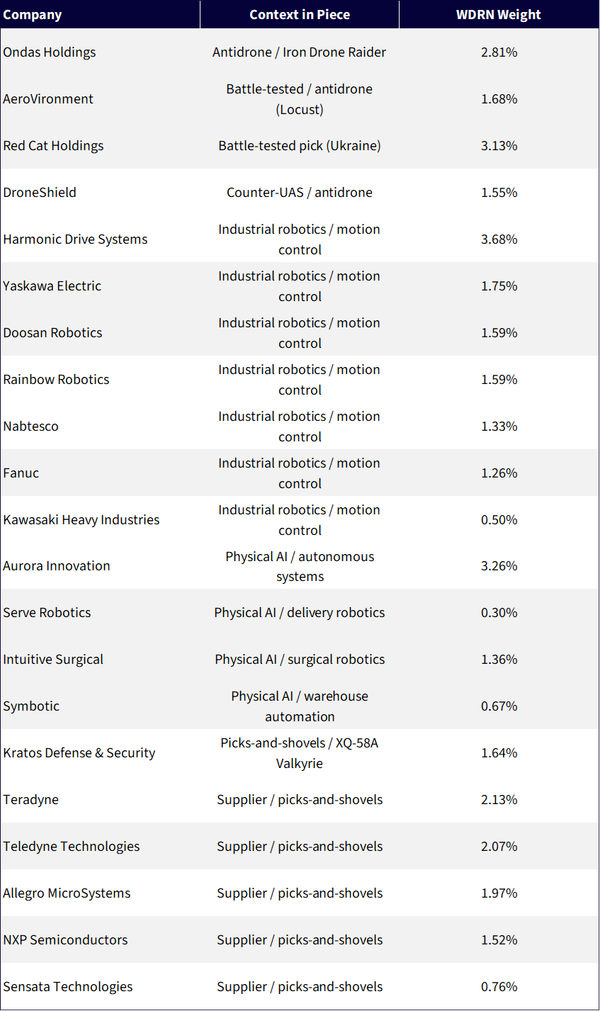

WDRN holds two companies the article specifically highlights in this context. Ondas Holdings, with a weight of approximately 2.8% in the fund, is cited for its Iron Drone Raider system, which is a reusable interceptor that physically nets incoming drones, alongside its radio-frequency jamming capabilities. DroneShield, an Australian-listed counter-UAS specialist, appears in the fund at roughly 1.6% and focuses on radio frequency (RF) detection and neutralization systems used by militaries and critical infrastructure operators worldwide.

AeroVironment's presence in the fund also spans both sides of this equation. The Barron's article specifically called out the company's Locust laser, which is a directed-energy weapon already deployed in operational contexts, as an example of how the most sophisticated drone companies are becoming full-spectrum solutions providers. A company that makes both the offensive platform and the defensive countermeasure occupies a structurally resilient position regardless of which side of the threat curve dominates defense budgets in a given year.

Picks and Shovels: The Supplier Layer

The Barron's article made an argument that any experienced thematic investor in recent years will be likely to recognize:

When technology is changing quickly and the competitive landscape among platform companies is uncertain, the suppliers often offer the most durable returns.

Kratos, which is the developer of the XQ-58A Valkyrie collaborative combat aircraft and a manufacturer of propulsion systems for drones and missiles, is a holding in WDRN at approximately 1.6%. The article notes that Kratos trades like a high-growth drone company, at roughly 50 times estimated 2027 earnings, reflecting the market's view that its position in the autonomous military aircraft market is differentiated enough to resist disruption from lower-cost munitions makers.

The supplier logic extends well beyond defense primes. WDRN holds a range of component and systems providers whose technology flows into drone and autonomous systems platforms regardless of which end-platform wins commercially.

Beyond Drones: Physical AI Is a Broader Mandate

It would be a mistake to read WDRN solely through the lens of a Barron's drone cover story, because the fund's mandate is deliberately wider. The "Physical AI" framing in the fund's name is not decorative, and it reflects the insight that the intelligence layer enabling autonomous drones is the same intelligence layer enabling humanoid robots, autonomous vehicles, and industrial automation systems. The fund is structured to capture the convergence of AI and physical systems across multiple form factors.

This shows up in a number of holdings that are not drone companies in any conventional sense.

These companies share the same technological DNA as drone platforms, which is to say things like real-time sensor fusion, edge inference, and closed-loop control systems, but their end markets are commercial rather than defense.

The industrial robotics layer of the fund, which includes Harmonic Drive Systems, Yaskawa Electric, Fanuc, Nabtesco, Doosan Robotics, Rainbow Robotics, and Kawasaki Heavy Industries, represents the global supply chain for precision motion control that underlies nearly every category of autonomous system, from surgical robots to manufacturing cells to drone actuators. These are not exciting names from a press-release standpoint, but they are the mechanical infrastructure of the Physical AI economy.

The Investment Thesis, Synthesized

The Barron's cover story is useful for investors in WDRN not because it validates specific stock picks, though the overlap is meaningful, but because it articulates why the drone and autonomous systems market could be at an inflection point. Battlefield deployment is the most demanding test any technology can face, and multiple systems in WDRN's portfolio have passed it. The antidrone market has emerged as a structural companion to drone proliferation, creating a second wave of demand within the same ecosystem. And the supplier layer, including semiconductors, sensors, propulsion, and motion control, provides exposure to the megatrend without requiring a bet on which specific platforms will dominate.

WDRN is designed to hold all three layers simultaneously, while also extending the investment thesis beyond drones into the broader Physical AI economy. The fund's top holdings span pure-play drone companies with battle-tested credentials, counter-UAS specialists operating on the other side of the same threat environment, defense-adjacent suppliers too embedded to be disrupted by any single platform shift, and Physical AI companies in non-defense verticals where the same autonomous systems technology is finding commercial traction.

One structural element of the fund deserves explicit attention:

WDRN carries zero weight to Chinese companies.9

This is not an oversight. The dominant narrative in drone hardware over the past decade has been DJI's commanding share of the commercial market, and China's broader drone industrial base remains formidable. But the policy and security environment has shifted decisively. The U.S. government has moved aggressively to restrict Chinese drone technology from federal procurement and critical infrastructure, and the broader onshoring of the drone and autonomous systems supply chain, from airframes to semiconductors to software, is now a stated national priority backed by executive action and congressional appropriations.10 WDRN is built to reflect that reality. The companies in the portfolio are the beneficiaries of that supply chain realignment, not bystanders to it. Investing in WDRN is, in part, a bet that the United States is serious about building a domestic Physical AI industrial base, and that the companies doing that work will be rewarded accordingly.

When a publication with Barron's credibility puts drones on its cover and identifies the same companies as battle-tested leaders, it is reasonable to ask whether the investment case is already priced in. The more interesting question for WDRN investors may be the opposite one:

How much of the Physical AI economy beyond drones remains underappreciated, and what happens when the same AI-and-autonomy narrative that has electrified the defense drone market begins to permeate warehouse logistics, last-mile delivery, surgical robotics, and industrial automation at comparable scale?

Figure 1: Companies Mentioned that Are Current WDRN Holdings

Source: WisdomTree, specifically the WDRN fund page, with holdings and weights as of June 26, 2026. Subject to change.

1 Unless otherwise noted, the source for this information is Root, A. (2026, June 24). Cheap drones are upending the defense sector. These 4 battle-tested stocks are leading the charge. Barron's.

2 Sources: Teledyne FLIR Defense. (2026, June 4). Teledyne FLIR Defense awarded $11.2 million U.S. Army contract for advanced CBRN sensor drone kits [Press release]. Business Wire; Teledyne FLIR OEM. (2026, April 28). Teledyne FLIR launches counter-drone detection software. Investing.com.

3 Sources: Allegro MicroSystems. (2026). Fiscal Year 2026 Annual Report; NXP Semiconductors. (2026, March 16). NXP delivers new innovations for advanced physical AI with NVIDIA.

4 Sources: Teradyne Robotics. (2025, December 9). Teradyne will expand its global robotics presence with new U.S. operations hub in Metro Detroit, Michigan [Press release]. Business Wire; Teradyne Robotics & Vention. (2026, June 22). Vention and Teradyne Robotics collaborate on digital twin creation platform [Press release]. PR Newswire.

5 Source: Intuitive Surgical. (2026, April 21). Intuitive announces first quarter earnings [Form 8-K, Exhibit 99.1]. U.S. Securities and Exchange Commission.

6 Source: Aurora Innovation. (2026, May 6). First Quarter 2026 Shareholder Letter [Form 8-K, Exhibit 99.1]. U.S. Securities and Exchange Commission.

7 Source: Serve Robotics. (2026, June 2). Serve Robotics continues expansion beyond food delivery, launches robotics laundry delivery with NoScrubs [Press release]. Globe Newswire.

8 Sources: Medline. (2026, April 16). Medline announces first-in-healthcare AI robotics partnership with Symbotic. Medline Newsroom; Unteachable Courses. (2026, April 7). Warehouse robots in 2026: Amazon, Ocado, Symbotic.

9 Source: WDRN fund page. As of June 26, 2026, there were no Chinese companies in WDRN. Subject to change.

10 Sources: Trump, D. J. (2025, June 6). Executive Order 14307: Unleashing American Drone Dominance. The White House; U.S. Congress. (2023). American Security Drone Act of 2023, Section 1821, National Defense Authorization Act for Fiscal Year 2024, Pub. L. No. 118-31; U.S. Congress. (2025). National Defense Authorization Act for Fiscal Year 2026, Subtitle I, Sections 899A–C.

There are risks associated with investing, including possible loss of principal. Companies engaged in Physical AI Activities are subject to unique regulatory, operational and technological risks, such as intense competition and potentially rapid product obsolescence. The regulation of such companies in the United States and other countries is diverse and rapidly evolving, which may inhibit or delay adoption. These companies are also heavily dependent on intellectual property rights and may be adversely affected by loss or impairment of those rights. Companies engaged in Physical AI Activities typically invest significant amounts of spending on research and development, and there is no guarantee that the products or services produced by these companies will be successful. Humanoid robotics companies are sensitive to trends in industrial production, capital-expenditure cycles, supply-chain conditions, and adoption rates of automation technologies across varied sectors including business and industrial end-users.

Humanoid robotics companies may have long and capital-intensive development timelines, highly uncertain paths to profitability and large-scale deployment, and limited product lines, markets, financial resources or personnel. Drone companies may be dependent on the U.S. Government and its agencies for a significant portion of their revenues, and the commercial and military adoption of drone technologies remains subject to extensive and evolving governmental oversight, including aviation safety standards, airworthiness certification requirements, export controls, and national security reviews. A fund that has a portfolio that is concentrated in the securities of issuers in a particular industry or group of related industries, may be adversely affected by the performance of those securities, and more susceptible to adverse economic, market, political, or regulatory occurrences affecting that industry or group of related industries.

Investments in non-U.S. securities involve political, regulatory, and economic risks that may not be present in U.S. securities. For example, foreign securities may be subject to risk of loss due to foreign currency fluctuations, political or economic instability, or geographic events that adversely impact issuers of foreign securities. Investments in securities and instruments traded in developing or emerging markets, or that provide exposure to such securities or markets, can involve additional risks relating to political, economic, or regulatory conditions not associated with investments in U.S. securities and instruments or investments in more developed international markets.

The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Physical AI, Humanoids, and Drones Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.