WDRN

Physical AI, Humanoids, and Drones Fund

Published July 1, 2026

Global Head of Research

The first article in this series made the case that drones may be the most investable near-term form of physical AI—machines that are already transitioning from specialized tools into mass-market robotic infrastructure. This article focuses on the harder questions:

Who makes them, who controls the supply chain, and what is changing?

The honest answer to the first two questions is uncomfortable for investors who prefer domestic exposure. China, and specifically DJI, dominates global drone production to an extent that has few parallels in any major technology sector. But the answer to the third question—what is changing—is where the investment thesis becomes interesting.. A combination of geopolitical pressure, regulatory action, targeted government financing, and private investment is beginning to construct a domestic U.S. drone supply chain. It is still early. The gaps are real. But the direction is clear, and the WisdomTree Physical AI, Humanoids, and Drones Fund (WDRN) is explicitly positioned around that thesis, and it haszero allocation to Chinese-domiciled companies.1

The Scope of Chinese Dominance

DJI, founded in Shenzhen in 2006, has achieved a market position with few parallels in any consumer technology sector. According to the Special Competitive Studies Project, a nonpartisan federal advisory body, DJI holds over 90% of the global consumer drone market, nearly 70% of the overall drone sector, and close to 80% of the U.S. commercial segment. In the public safety market, a 2021 survey by the Airborne International Response Team found that 90.4% of public safety agencies operated DJI drones, rising to 92.1% among law enforcement programs specifically. More recent data suggests DJI's global share has compressed slightly, to approximately 70% of the civilian market as of 2025, down from 74% in 2024, reflecting the early effects of regulatory pressure. The core dominance, however, remains intact.2

DJI's dominance is not difficult to explain. The company produces excellent products at competitive prices, backed by a deeply integrated Chinese manufacturing ecosystem.

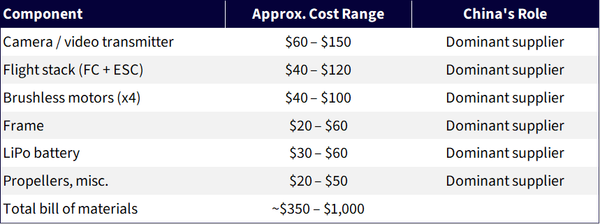

Figure 1: Component cost breakdown for a typical 6-10 inch First-Person View (FPV) Drone

Source: Morgan Stanley Global Embodied AI Team. (2025, December). The Robot Almanac: Vol. 4: Drones & Air Mobility. Morgan Stanley Research. FC: Flight Controller. ESC: Electronic Speed Controller. LiPo: Lithium Polymer.

The component picture matters because it illustrates where China's advantage actually lies. It is not primarily in AI software or cutting-edge semiconductors, areas where the U.S. and its allies retain significant leadership. It is in manufacturing density—the ability to produce high volumes of physical components at low cost, with rapid iteration, through tightly integrated supply chains built over decades.

The Regulatory Ratchet

U.S. policy toward Chinese drones has been tightening for several years, and the trajectory is unlikely to reverse. The sequence of actions illustrates a systematic effort to reduce dependence on Chinese drone hardware across both defense and civilian markets.

The cumulative effect of this regulatory ratchet is that the Chinese dominance described in the previous section is being contested, not by market forces alone, but by deliberate policy intervention. The question is no longer whether U.S. policy is moving in this direction. It clearly is. The question is how fast the gap can be closed and at what cost.

The Supply Chain as Investment Framework

The most useful way to think about drone investment exposure is not as a collection of drone companies but as a layered supply chain. Each layer has different economics, different competitive dynamics, and different exposure to the transition underway. WDRN holds companies across many of these layers.

Layer 1: Defense Drone Original Equipment Manufacturers (OEMs)7

These are the most direct plays on U.S. government demand, and they face the most direct pressure to meet production and cost targets. The competitive landscape is evolving rapidly, with both established defense primes and specialized startups competing for contracts.

Layer 2: Counter-Drone Systems7

A world with more drones is also a world that needs more sophisticated defenses against them. Counter-drone spending is growing as a direct consequence of drone proliferation, and it represents a structural hedge within the physical AI investment theme.

Layer 3: Enabling Components and Subsystems7

Component manufacturers often offer more diversified and defensible exposure than OEMs, because their products serve multiple platforms and customers. If drone volumes grow, component demand grows with them — regardless of which airframe wins any given procurement contest.

Layer 4: Semiconductor and Sensor Enablers7

Drones require compute, sensing, and processing capabilities that draw on the broader semiconductor and sensor ecosystem. Several fund holdings provide this exposure.

Layer 5: Autonomous Systems and Software Infrastructure7

The software that enables drone autonomy — flight planning, obstacle avoidance, mission management, swarm coordination — may be the most defensible layer of the stack over time. Companies that own the operating layer for drone fleets could have durable advantages as hardware commoditizes.

Layer 6: Defense and Aerospace Primes with Drone Programs7

Several large defense companies in the fund have significant drone or unmanned systems programs embedded within broader portfolios.

The Zero-China Stance: Bold or Obvious?

WDRN’s current 0% allocation to Chinese-domiciled companies is worth examining directly. It is not a passive outcome of screening; it is a deliberate investment stance, and one with meaningful implications.

In our view, as of mid-2026, it is the only coherent position for a fund aligned with U.S. defense and industrial policy. The regulatory trajectory described earlier in this article points in the direction of reducing, not increasing, U.S. reliance on Chinese drone technology. A fund that owns DJI or other Chinese-domiciled drone companies while positioning as a domestic-drone-industry thesis is working at cross purposes with itself.

We believe the geopolitical logic is durable. The industries the U.S. government has identified as strategically indispensable, such as semiconductors, batteries, shipbuilding, and now drones, have all moved toward domestic supply chain development regardless of short-term commercial cost. The pattern is consistent.

1 As of May 29, 2026, WDRN, which tracks the total return performance of the WisdomTree Physical AI, Humanoids and Drones Index before fees and expenses, did not have exposure to any companies domiciled in China. Holdings subject to change.

2 Sources: Special Competitive Studies Project. (2025, January 7). Commercial drones: 2025 gaps analysis; Airborne International Response Team & DRONERESPONDERS. (2021). 2021 public safety UAS survey. As reported in: DRONELIFE. (2021, August 9). DJI still dominates public safety sector, survey finds; BusinessWire / ElectroIQ. (2025, October 23). DJI statistics by usage, sales, revenue and facts (2025).

3 Source: Axon Enterprise. (2025, December 10). New drone laws take effect: What public safety agencies need to know.

4 Source: DroneDJ. (2025, October 1). DJI fires back after court upholds Pentagon's drone blacklist label.

5 Source: Morgan Lewis. (2026, January 26). FCC exempts certain drones and components from covered list to address national security risks.

6 Source: Government Technology. (2025, January 10). Drones in 2025: What state and local governments should know.

7 Percentages reference the weight in WDRN as of May 27, 2026. Holdings subject to change.

There are risks associated with investing, including possible loss of principal. Companies engaged in Physical AI Activities are subject to unique regulatory, operational and technological risks, such as intense competition and potentially rapid product obsolescence. The regulation of such companies in the United States and other countries is diverse and rapidly evolving, which may inhibit or delay adoption. These companies are also heavily dependent on intellectual property rights and may be adversely affected by loss or impairment of those rights. Companies engaged in Physical AI Activities typically invest significant amounts of spending on research and development, and there is no guarantee that the products or services produced by these companies will be successful. Humanoid robotics companies are sensitive to trends in industrial production, capital-expenditure cycles, supply-chain conditions, and adoption rates of automation technologies across varied sectors including business and industrial end-users.

Humanoid robotics companies may have long and capital-intensive development timelines, highly uncertain paths to profitability and large-scale deployment, and limited product lines, markets, financial resources or personnel. Drone companies may be dependent on the U.S. Government and its agencies for a significant portion of their revenues, and the commercial and military adoption of drone technologies remains subject to extensive and evolving governmental oversight, including aviation safety standards, airworthiness certification requirements, export controls, and national security reviews. A fund that has a portfolio that is concentrated in the securities of issuers in a particular industry or group of related industries, may be adversely affected by the performance of those securities, and more susceptible to adverse economic, market, political, or regulatory occurrences affecting that industry or group of related industries.

Investments in non-U.S. securities involve political, regulatory, and economic risks that may not be present in U.S. securities. For example, foreign securities may be subject to risk of loss due to foreign currency fluctuations, political or economic instability, or geographic events that adversely impact issuers of foreign securities. Investments in securities and instruments traded in developing or emerging markets, or that provide exposure to such securities or markets, can involve additional risks relating to political, economic, or regulatory conditions not associated with investments in U.S. securities and instruments or investments in more developed international markets.

The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Physical AI, Humanoids, and Drones Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.