NTSX

U.S. Efficient Core Fund

Published June 26, 2026

Director, Model Portfolios

Current Market Regime Revives an Original Case for Capital Efficiency

When we launched the WisdomTree U.S. Efficient Core Fund (NTSX) in 2018, the case was straightforward: a diversified stock/bond portfolio can be a better starting point than 100% equities on a return-per-unit-of-risk basis. If that more efficient portfolio can be scaled up modestly through the prudent use of leverage, it may also compete with or improve upon the return profile of a traditional all-equity allocation.

While the implementation in the ETF world was first of its kind and started a new wave of capital-efficient portfolio combinations, the underlying idea was not original. The academic roots trace back to Cliff Asness’s 1996 piece, titled “Why Not 100% Equities: A Diversified Portfolio Provides More Expected Return per Unit of Risk,” which argued that an “investor willing to bear the risk of 100% equities can do even better with a diversified portfolio.”

Asness showed how levering a traditional 60/40 strategy could target volatility similar to 100% equities while potentially improving returns.

His paper, using data from 1926 through 1993, applied 155% exposure to a 60/40 portfolio, rebalanced monthly, with leverage financed at the one-month Treasury bill rate. When we updated the figures for the next 30-plus years, we saw his results looked even stronger out of sample in the period after the paper was published than in the original 1926–1993 sample.

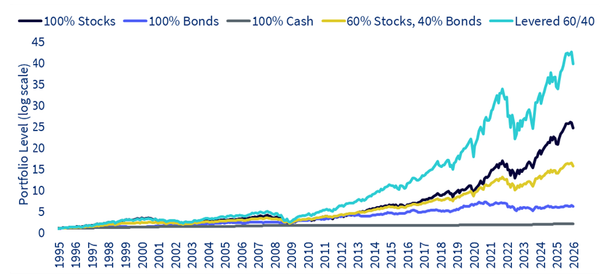

Figure 1: Growth of $1

Sources: WisdomTree, Ibbotson, Morningstar Direct, for the period 1/31/94 to 3/31/26. Past performance is not indicative of future results. You cannot directly invest in an index. The research shown is not a backtest or hypothetical representation of NTSX.

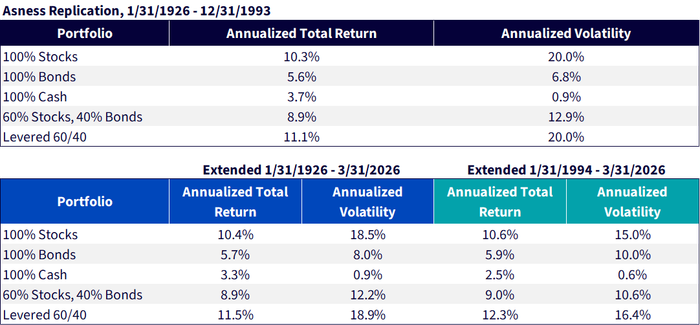

Figure 2: Annualized Returns and Volatility Across Portfolio Allocations

Sources: WisdomTree, Ibbotson, Morningstar Direct, as of 3/31/26. Past performance is not indicative of future results. You cannot directly invest in an index. The research shown is not a backtest or hypothetical representation of NTSX.

Adding Diversifiers or Equity Hedge

In discussing the portfolio use cases for our capital efficient product line, I always say NTSX was designed to be a portfolio building block that creates space for alternatives and diversifiers.

Investors often struggle to add alternatives to portfolios because they don’t know where to fund diversifying strategies from their standard stock/bond sleeves.

When used as intended, the capital-efficient family allows investors to keep their core stock and bond exposure and complement it with strategies like commodities, managed futures, long-short investing—really anything that can earn a return above cash can be accretive to the standard 60/40 allocations.

I usually argue against replacing traditional 100% equity funds with NTSX.

But in this piece, let’s consider the other side: how replacing a portion of traditional equities with NTSX could offer a solution for investors who want to become somewhat more defensive.

NTSX delivers approximately 90% of the equity exposure of a traditional 100% equity allocation, while adding a 60% notional allocation to U.S. Treasury futures. As a result, NTSX can help incorporate more bond duration (interest rate sensitivity) into equity portfolios while slightly reducing equity market participation.

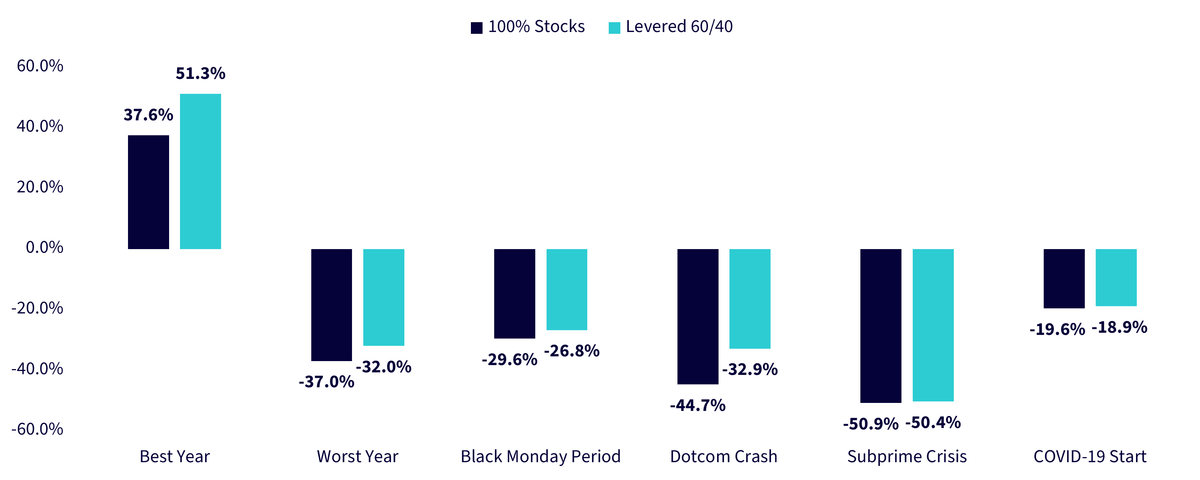

When used in this manner, leverage applied to a diversified portfolio does not necessarily result in greater portfolio risk. Across a range of historical market environments, the leveraged 60/40 framework has often produced a risk profile comparable to 100% equities while providing additional portfolio diversification.

Figure 3: Scenario Analysis

Sources: WisdomTree, Ibbotson, Morningstar Direct, as of 3/31/26. Past performance is not indicative of future results. You cannot invest directly in an index. The research shown is not a backtest or hypothetical representation of NTSX.

In the current market environment, that capital efficient bond exposure could reassert itself as a more effective hedge to equity risk.

The Evolving Market Backdrop

For a while, as bonds soared in price and yields fell to all-time lows in 2020, this diversification case became harder to make. A persistent inflation regime post pandemic relief measures turned stocks and bonds into fellow travelers.

Bonds went from being a diversifier to a risk creator for equities—as the Fed raised rates significantly and rising long-term discount rates pressured stocks—particularly in 2022 when both sides of the classic 60/40 came under immense pressure. Bonds did not provide enough current income at the start of that move higher to offset the sharply rising rates.

This regime looks to be changing again.

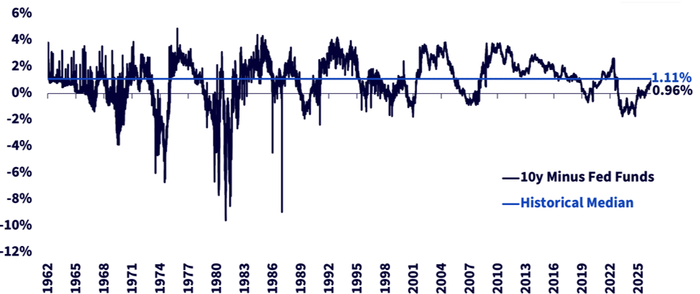

Figure 4: Current and Historical Median 10-Year Treasury Yield vs. Fed Funds Effective Rate

Source: WisdomTree, FRED, for the period 1/2/62 to 5/15/26.

The 10-year Treasury yield currently sits just under 4.5% and the effective fed funds rate was 3.62%, putting the 10-year yield less than 100 basis points above the federal funds rate again after a long yield curve inversion. A positively sloped yield curve also improves the economics of Treasury futures exposure, as the yield earned on longer-duration Treasuries is now above the short-term funding rates that typically underpin futures financing costs.

This positive and upward sloping yield curve spread also reflects a healthy economy. When the yield curve was inverted, we wanted to see the Fed cut rates more aggressively and adding duration to portfolios was costly in terms of current income rates.

Ten-year inflation-adjusted real yields are currently over 2%. Using the Rule of 72, investors can now roughly double inflation adjusted purchasing power in about 33 years. That is not exciting as a standalone return or measured relative to equities, but it is a very different world from the negative-real-yield regime investors lived through for a number of years where one was paying via negative real rates to get inflation adjustments in TIPS bonds.

Bonds today can act again as effective ‘hedges’ to growth and recession risk.

The S&P 500, at a 20.9x forward 12-month P/E, implies an earnings yield of about 4.8%—roughly a 15-year rule-of-72 doubling pace.

But against a 2.18% 10-year TIPS yield, the simple earnings-yield-minus-real-yield spread is only about 2.6 percentage points.

In other words, stocks still look superior for growth, but real bonds are back in the asset-allocation conversation as real competitors for their diversification properties.

A diversified stock/bond portfolio like a 60/40 is not supposed to beat 100% equities on raw, unlevered return. It is supposed to deliver a better return for the risk taken.

Modest leverage applied to the better diversified portfolio can compete with 100% equity positions and the regime setup today could be setting up for a 90/60 combination of stocks and bonds to offer an interesting alternative to equity risk.

This logic gets stronger as bonds become a better hedge for recession risk. Downside growth surprises usually hurt equities while also pulling down expected policy rates, which supports bond prices and produces the classic risk-off, negative stock/bond correlation where bonds hedge equity risk.

If the next move is a sharp climb in the 10-year through 5% because of inflation, fiscal term premium, or a broader bond-market repricing, that is still a regime where both stocks and bonds can struggle together.

The case today is not just that bonds look more useful again. It is that the combination of a positive term structure, meaningfully positive real yields, and a more growth-sensitive cross-asset regime makes one of the original capital-efficient investment cases easier to defend again.

Stocks are still an ideal long-run growth engine. Bonds are starting to do their recession-hedge job again. And when those two statements are both true at the same time, the old question returns in force: why own 100% equities when you may be able to own a better diversified portfolio and then scale the risk more intelligently?

There are risks associated with investing, including possible loss of principal. While the Fund is actively managed, the Fund’s investment process is heavily dependent on quantitative models and the models may not perform as intended. The Fund invests in derivatives to gain exposure to U.S. Treasuries. The return on a derivative instrument may not correlate with the return of its underlying reference asset. The Fund’s use of derivatives will give rise to leverage and derivatives can be volatile and may be less liquid than other securities. As a result, the value of an investment in the Fund may change quickly and without warning and you may lose money. Interest rate risk is the risk that fixed income securities, and financial instruments related to fixed income securities, will decline in value because of an increase in interest rates and changes to other factors, such as perception of an issuer’s creditworthiness. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

U.S. Efficient Core Fund

Director, Model Portfolios

Andrew Okrongly joined WisdomTree in 2022 as a Director on the Model Portfolios Team. He is responsible for the design and ongoing management of model portfolios and custom solutions for portfolio managers and advisors. Andrew is also a member of the Model Portfolio Investment Committee. Prior to joining WisdomTree, Andrew was a Director on the Outsourced Chief Investment Officer (OCIO) team at Commonfund, where he was responsible for macro-economic analysis and advising institutional clients on strategic and tactical asset allocation. Andrew began his career at BlackRock where he held a variety of fixed income and multi-asset investment roles. Andrew received a BBA degree from the University of Michigan and is a holder of the Chartered Financial Analyst designation.