WTLS

Efficient Long/Short U.S. Equity Fund

Published May 21, 2026

Global Chief Investment Officer

Most investors understand the case for diversification. The challenge is not the theory. It is the implementation.

Every dollar allocated to a diversifying strategy is often a dollar taken away from a core equity allocation. That trade-off can be painful. Such things as:

Each of these may help improve risk metrics, but they also create a familiar behavioral problem:

When equities are rising, investors often feel like they are falling behind.

That “fear of missing out” is one reason many diversifying strategies are difficult to hold and often get sold at exactly the wrong times. They may reduce volatility or add differentiated return streams, but if they replace core equity exposure, investors can become impatient during bull markets.

The WisdomTree Efficient Long/Short U.S. Equity Fund (WTLS) was designed to address that problem directly.

WTLS seeks to maintain broad U.S. equity market exposure while adding a systematic long/short equity overlay on top. In simple terms, it is designed as a true portable alpha strategy:

Combine broad market beta with a separate, diversified alpha engine.

The structure matters. For every hypothetical $100 invested, WTLS seeks to invest approximately $90 in S&P 500 exposure to provide core U.S. equity market beta. On top of that, the Fund layers a long/short U.S. equity strategy, creating roughly $180 of total notional exposure: $90 of S&P 500 market exposure plus $90 of long/short equity exposure.

That is the capital-efficient idea: do not ask investors to choose between equity beta and diversifying alpha. Add the alpha on top of beta.

Long/short equity sounds attractive in theory. But the category has often disappointed investors when used as a replacement for equities.

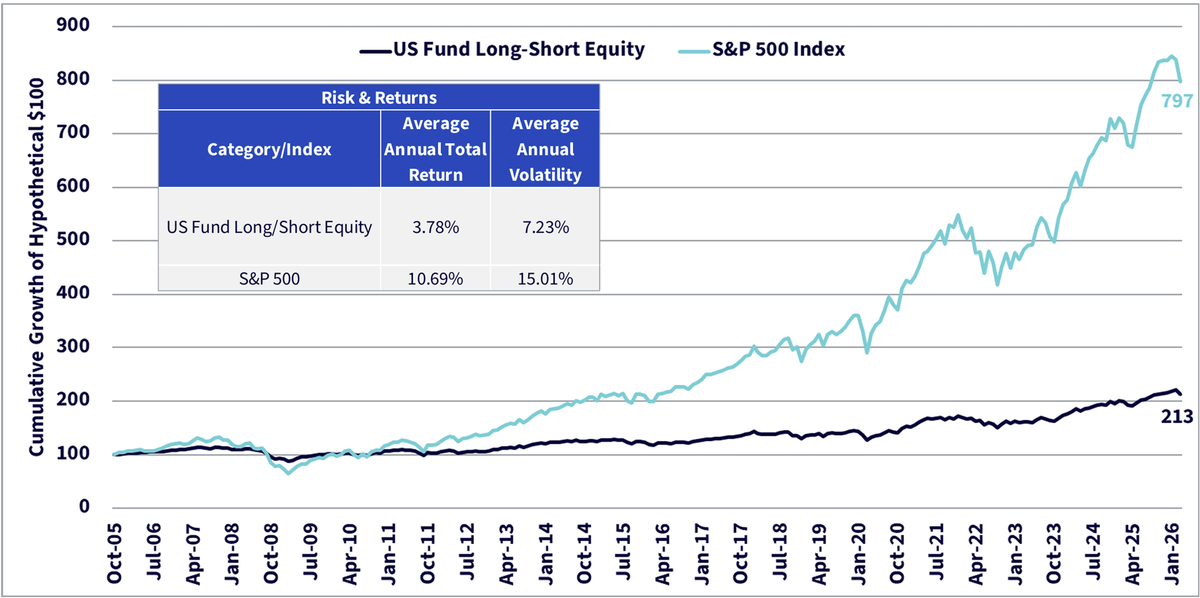

The U.S. Fund Long/Short Equity category generated an average annual total return of 3.78% from November 2005 through March 31, 2026, versus 10.69% for the S&P 500 Index. Volatility was lower, but the opportunity cost versus broad equity beta was substantial.1

Sources: WisdomTree, Bloomberg, Morningstar Direct. Data is from November 30, 2005 through March 31, 2026. U.S. Fund Long-Short Equity is a Morningstar Category, and the return represents the average return of all managers within that category, not any single strategy. Past performance is not indicative of future results. You cannot invest directly in an index.

The problem may not be long/short equity itself. Used as a replacement for equities, long/short can create regret during strong equity markets. Used as an overlay on top of an equity allocation, it can become a complementary alpha source.

WTLS is built around that use case.

The long/short overlay in WTLS is not a discretionary stock-picking sleeve. It is systematic and model-driven.

The strategy starts with the 2,000 largest and most liquid U.S. stocks and evaluates securities using more than 150 equity features, including valuation, momentum, quality, profitability, liquidity, investment and risk-related characteristics. The portfolio typically holds around 600 stocks, approximately 300 long and 300 short, and is rebalanced monthly.

The goal is not simply to buy “cheap” stocks or short “expensive” stocks. Markets are more complicated than that. Factor relationships evolve. A signal that works well in one environment may decay, reverse or become crowded in another.

That is where the machine-learning framework becomes useful.

WTLS uses complementary models, including Instrumented Principal Component Analysis (IPCA) and autoencoders. IPCA is a linear machine-learning technique designed to extract latent factors from large financial datasets. Autoencoders are deep-learning models that can identify more complex, non-linear patterns.

A plain-English way to describe the models:

The model is trying to separate signal from noise across a very large universe of stock characteristics, then build a diversified long/short portfolio that emphasizes the strongest relative-return opportunities.

WTLS is not trying to time the S&P 500. The long/short sleeve is designed to seek alpha through relative stock selection.

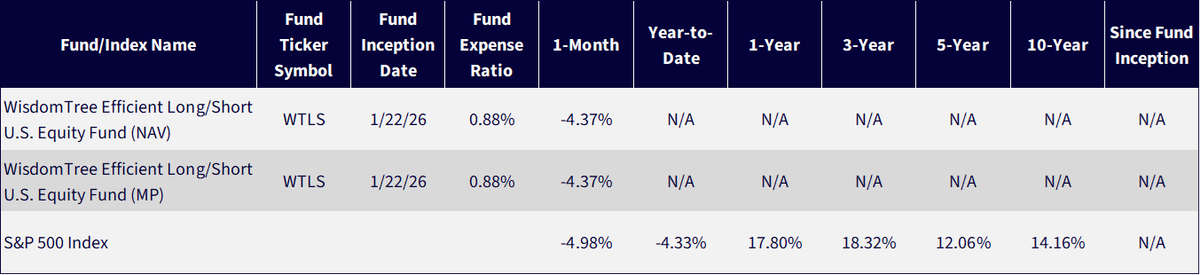

Since inception through May 13, 2026, WTLS was up 13.2%, versus 8.7% for the S&P 500, with 4.5% excess return.2

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of May 14, 2026, but showing returns for the period ended March 31, 2026. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

That is the intended profile: core market participation plus a distinct overlay that can add value through stock selection.

This is a short live period. No investor should extrapolate a few months of performance into a permanent expectation. But the early result is useful because it illustrates what the structure is designed to do: participate in broad equity gains while seeking additional return from a systematic long/short engine.

The Allocation Case

WTLS is best understood as a tool for investors who want to keep U.S. equity exposure but make that equity allocation work harder within a portfolio context.

Instead of asking, “Should I replace part of my equity portfolio with a long/short fund?” the better question is:

Can I add a diversifying alpha source while preserving the role of equities as the core growth engine of the portfolio?

WTLS was built to answer yes. WTLS offers a way to introduce a differentiated return driver. For investors who struggled to hold diversifiers because they lag in bull markets, WTLS offers a structure that keeps the equity beta in place.

The case for WTLS is not that it eliminates risk. It does not. The Fund uses derivatives, leverage and quantitative models, and those models may not perform as intended. Investors can lose money. But the portfolio construction problem it addresses is real:

How to add diversifying return potential without sacrificing core equity exposure.

That is the potential of capital-efficient investing, and this is the role WTLS is designed to play.

1 Source: Morningstar Direct. (2026). U.S. Fund Long/Short Equity category average annual total return, November 2005–March 2026 [Database]. Morningstar, Inc.

2 Sources: WisdomTree, Alphabet and FactSet, with data as of May 13, 2026 and the inception of WTLS being January 22, 2026. Standardized performance is available in Figure 2. ‘The Market’ refers to the S&P 500 Index.

There are risks associated with investing, including possible loss of principal. The Fund invests in a basket of equity securities of large capitalization U.S. companies generally weighted by market capitalization. The Fund expects to invest most of its assets in the securities of U.S. companies and is therefore, more likely to be impacted by events or conditions affecting the United States. The Fund invests in derivatives to gain exposure to U.S. equity securities. The return on a derivative instrument may not correlate with the return of its underlying reference asset. The Fund’s use of derivatives will give rise to leverage. Derivatives can be volatile and may be less liquid than other securities. As a result, the value of an investment in the Fund may change quickly and without warning and you may lose money. While the Fund is actively managed, the Fund's investment process is heavily dependent on quantitative models and the models may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Efficient Long/Short U.S. Equity Fund

Global Chief Investment Officer

Jeremy Schwartz has served as Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Behind the Markets podcast. Jeremy is a member of the CFA Society of Philadelphia.