WDIG

Efficient Rare Earth Plus Strategic Metals Fund

Published May 26, 2026

Global Head of Research

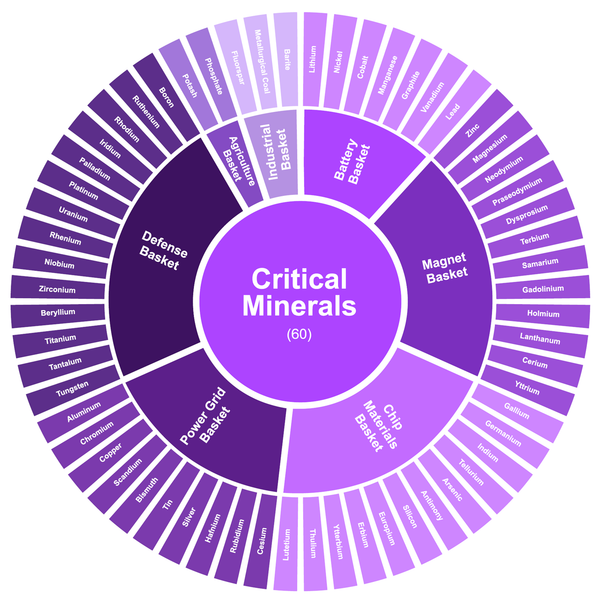

Of the roughly 94-98 elements that occur in nature, 60 now sit on a U.S. government watch list. They fall into seven groups — and together, they explain more about the global economy than most financial models ever will.

In the 1930s, artists used uranium to color ceramics. It produced a vivid orange glaze, and no one thought much more about it. When the United States government assembled its first strategic mineral stockpile in 1939, uranium was left off the list entirely. Six months later, a letter from Albert Einstein landed on President Roosevelt's desk. The ceramic pigment, it turned out, could end a war.1

That story, a mineral dismissed until the moment it becomes civilization-altering, is not a historical curiosity. It is the operating condition of the modern economy. Right now, there are dozens of elements most people have never heard of that sit at the foundation of electric vehicles, fighter jets, smartphones, data centers, and the electrical grid itself. They are not interchangeable. They are not optional. And for the vast majority of them, the United States depends on supply chains it does not control.

The U.S. Geological Survey maintains an official list of 60 critical minerals, in other words, materials deemed essential to economic and national security, and at risk of supply disruption.2 The list has grown over time as technology has advanced and geopolitical exposure has sharpened. Understanding it requires more than memorizing names from the periodic table. What makes the list genuinely illuminating is the underlying architecture: these 60 minerals are not a random collection. They fall into seven functional baskets, each one powering a distinct pillar of modern civilization.

Think of them the way you think of vitamins. Needed in relatively small quantities. No good substitutes. And without them, the entire system risks failure.

Figure 1: How 60 Critical Minerals Map to the Modern Economy

Sources: USGS, with specific image seen in Social Capital. (April 19, 2026). Critical minerals: The 60 minerals that power the modern world. Social Capital. Subject to change.

The Battery Basket

The basket most people encounter first, at least conceptually, is batteries. Nine minerals. One enormous industry. One in four new cars sold globally in 2025 was electric, a threshold that seemed far off not long ago. Every one of those 20 million vehicles requires lithium, graphite, cobalt, nickel, manganese, and four other critical minerals to move.3 A typical EV requires roughly six times the mineral inputs of a conventional gasoline car.4 The battery basket is the reason that transition is not simply a matter of swapping one powertrain for another.

The U.S. battery market reached $27 billion in 2025, with automotive batteries accounting for more than half. The exposure is acute: China processes 59% of the world's lithium, controls 95% of global magnesium production, and refines 79% of battery-grade graphite. Tesla, America's dominant EV maker, currently sources virtually all of the battery minerals inside its vehicles from supply chains running through Chinese processing facilities. A single export restriction could halt EV production across the Western world for years.5

The Power Grid Basket

Four minerals. Almost everything that moves electricity from where it is generated to where it is used. Aluminum carries power across long-distance transmission lines. Copper runs through virtually every wire, cable, and circuit in the built environment. Silicon and silicon ferroalloys underpin the grid's switching infrastructure. The power grid basket is, in a sense, the most foundational of all, because every other basket depends on electricity to function.

The scale is difficult to comprehend. AI data centers now consume as much electricity as entire nations. The buildout of charging infrastructure for EVs and the expansion of renewable generation represent what may be the largest infrastructure investment in American history. All of it runs on copper and aluminum. The U.S. imports a significant portion of both, with China controlling 45% of global copper refining and 84% of silicon metal production.6

The Magnet Basket

Ten minerals, mostly rare earth elements, that do one remarkable thing: convert electricity into motion, and motion into electricity. The magnets made from neodymium, praseodymium, dysprosium, and terbium are the most powerful permanent magnets on earth. They sit inside the electric motors of every EV, inside every wind turbine, inside hard drives, inside the guidance systems of missiles, and inside the actuators of submarine control surfaces.

China mines approximately 69% of the world's rare earth elements and processes 91% of them. That processing dominance is what makes the magnet basket particularly precarious, the ore can come from many places, but the chemistry required to separate rare earths from each other and refine them to usable purity is extraordinarily difficult to replicate. The U.S. lost most of its rare earth processing capacity in the 1980s and 1990s, when Western companies relocated to China chasing cheap labor and lax environmental regulations. They handed China the industry. It took 15 years for China to fully consolidate control. By 2010, they owned it.7

The Chip and Display Basket

Eighteen minerals. That is the semiconductor supply chain in elemental form. Silicon is the obvious entry point, but the basket extends well beyond it: gallium and germanium for high-speed chips; arsenic for 5G radio-frequency components; indium for touchscreens and flat panels; hafnium for the gate dielectrics inside every modern central processing unit (CPU); antimony for phase-change memory. Each of these materials has properties no other element can replicate at the required scale and precision.

China controls 99% of global gallium production and 99% of germanium refining, and both are 100% import-dependent for the United States. In August 2024, China announced that companies would need export licenses to ship antimony abroad. By December 2024, it had banned all antimony exports to the U.S. entirely. The response was a $80 million Department of Defense award to a mining company in Idaho to restart domestic production. Expected start date: 2028.8

China does not need to control chip fabrication plants to pressure the semiconductor supply chain. It already controls the minerals those fabs depend on.

The Defense Basket

Fourteen minerals, and the one basket where the consequences of disruption are measured not in dollars but in military readiness. Tungsten for armor-piercing munitions and jet engine components. Beryllium for missile guidance structures and aerospace alloys. Titanium for aircraft frames and armor plating. Rhenium for the high-performance turbine blades inside fighter jet engines. Uranium for both nuclear reactors and weapons. Tantalum for the capacitors inside military electronics.

A single F-35 Lightning II requires more than 400 kilograms of rare earth elements for its targeting systems, radar, and lasers.9 The defense basket is not a standalone category, it cuts across all the others. The same dysprosium in an EV motor is in a missile guidance system. The same gallium in a smartphone chip is in radar electronics. Defense urgency transforms the entire mineral map into something with an additional, non-negotiable layer of strategic weight.

The Agriculture and Industrial Baskets

Two minerals for agriculture, phosphate and potash, that have no substitutes in farming and underpin the food supply of the entire planet. Unlike every other basket, there is no alternative chemistry waiting in reserve. Potash was not elevated to critical status until 2025, added after bipartisan pressure and a U.S. Department of Agriculture (USDA) recommendation.10 The episode illustrated something important: the list is not static, and the criteria for what counts as critical can shift faster than the policy apparatus can respond.

The industrial basket is three minerals, specifically fluorspar, metallurgical coal, and barite, that never make headlines and keep everything else running. Fluorspar becomes hydrofluoric acid, which etches silicon wafers in every semiconductor fabrication plant on earth. Barite goes into drilling fluid that prevents oil well blowouts; more than 75% of U.S. consumption is imported every year, with no large-scale substitute available.11 These are the invisible inputs. They are also, in their quiet way, the most irreplaceable.

The Pattern Underneath

Look across all seven baskets and a single pattern emerges with near-total consistency: the ore is global, the processing is Chinese, and the United States has limited capabilities for most of it. China controls somewhere between 60% and 95% of processing capacity across the majority of critical minerals. In the U.S., it currently takes an average of 29 years from mineral discovery to commercial production, the second-longest timeline in the world. It takes 7 to 10 years just to permit a new mine. In Canada or Australia, countries with comparable environmental standards, permitting takes two years.12

The USGS ranking model assigns a probability to each potential supply disruption and then estimates the downstream gross domestic product (GDP) impact. Seventeen minerals have already been assigned a 100% probability of disruption from China, because China has already imposed export restrictions or outright bans on them. Samarium, a rare earth essential to the most powerful permanent magnets used in jet engines and missiles, carries a modeled probability-weighted GDP impact of $4.5 billion, and China has imposed a 100% export restriction on it.13

The uranium story from 1939 resonated not because uranium was unique, but because it was first. The question the seven-basket framework poses, quietly and insistently, is which mineral will be next, and whether the answer will arrive in a letter, or in an export ban.

Conclusion: One Strategy with Two Types of Strategic Metal Exposure

The seven baskets described above are not an abstract taxonomy. They are a live map of where the modern economy is most exposed, and where the next decade of industrial competition will be fought. The minerals powering EV motors, missile guidance systems, semiconductor fabs, and AI data centers share a common vulnerability: demand is accelerating while supply remains geographically hostage to a single dominant processor.

For investors, that tension is not simply a risk to manage. It is a structural opportunity to understand.

The WisdomTree Efficient Rare Earth Plus Strategic Metals Fund (WDIG) was built precisely for this environment. By combining equity exposure to the global companies mining and refining these critical materials with direct commodity exposure through a diversified metals futures basket, WDIG offers participation in both the producers building new supply chains and the underlying metals those chains depend on, within a single, capital-efficient structure.

The uranium story ended with a letter to Roosevelt. The rare earth story, the gallium story, the antimony story — those are still being written. WDIG is designed for investors who want to be positioned before the next chapter is dictated by an export ban rather than discovered after one.

1 Sources: Einstein, A. (1939, August 2). Letter to President Franklin D. Roosevelt. Franklin D. Roosevelt Presidential Library and Museum; U.S. Congress. (1939). Strategic and Critical Materials Stock Piling Act (Public Law 76-117); U.S. Atomic Energy Commission. (1947). The story of uranium. U.S. Government Printing Office.

2 Sources: U.S. Department of the Interior. (2022). Final list of critical minerals 2022. Federal Register, 87(44), 10381–10382; U.S. Geological Survey. (2025). Critical minerals list (latest update). U.S. Department of the Interior.

3 Source: International Energy Agency (IEA). (2025). Global EV Outlook 2025.

4 Source: International Energy Agency. (2021). The role of critical minerals in clean energy transitions. IEA.

5 Sources: IMARC Group. (2025). United States battery market size, share & forecast 2026–2034;

Fortune Business Insights. (2025). U.S. battery market size, share & industry analysis;

Council on Strategic Risks. (2025). The devil is in the details: Minerals, batteries, and U.S. dependence on Chinese imports.

6 Sources: S&P Global. (2025). Global data center power demand to double by 2030 on AI surge; International Energy Agency. (2025). Share of top refining country for energy-related minerals; U.S. Geological Survey. (2025). Mineral commodity summaries 2025. U.S. Department of the Interior.

7 Sources: U.S. Department of Energy. (2022). Rare earth elements: A review of production, processing, recycling, and associated environmental issues; Mancheri, N. A., Sprecher, B., Bailey, G., Ge, J., & Tukker, A. (2019). Effect of Chinese policies on rare earth supply chain resilience. Resources, Conservation and Recycling, 142, 101–112; Humphries, M. (2013). Rare earth elements: The global supply chain (CRS Report R41347). Congressional Research Service.

8 Sources: Reuters. (2024, August 15). China to restrict exports of antimony, gallium, and germanium citing national security; Reuters. (2024, December 3). China bans antimony exports to the United States amid escalating trade tensions; U.S. Department of Defense. (2024). Defense Production Act Title III: Investments in critical minerals supply chains; Perpetua Resources Corp. (2024). Perpetua Resources receives Department of Defense award to advance antimony production.

9 Source: U.S. Department of Defense. (2024). DoD looks to establish “mine-to-magnet” supply chain for rare earth materials.

10 Source: U.S. Department of the Interior. (2025). Final 2025 list of critical minerals. Federal Register.

11 Sources: U.S. Geological Survey. (2024). Fluorspar statistics and information. U.S. Department of the Interior; U.S. Geological Survey. (2024). Barite statistics and information. U.S. Department of the Interior.

12 Sources: S&P Global Market Intelligence. (2023). Mine development times: The long road from discovery to production; National Mining Association. (2023). Permitting, economic value and mining in the United States.

13 Source: U.S. Geological Survey. (2025). Methodology and technical input for the 2025 U.S. list of critical minerals (Open-File Report 2025–1047). U.S. Department of the Interior.

There are risks associated with investing, including possible loss of principal. The Fund is actively managed and invests in commodity metals futures contracts from an eligible exchange, and equity securities issued by global companies primarily involved in strategic metals and rare earths mining activities.

The value of metal commodities, such as various mined metals and commodity-linked derivative instruments, such as commodity metals futures contracts, typically is based upon the price movements of the physical commodity or an economic variable linked to such price movements. Price movements in metals and commodity metals futures contracts may fluctuate quickly and dramatically, have a historically low correlation with the returns of the stock and bond markets, and may not correlate to price movements in other asset classes. By investing in the equity securities of metal miners, the Fund may be susceptible to financial, economic, political, or market events that impact the metal mining industry. Derivatives are used by the Fund to gain exposure to strategic metals and rare earth mining activities. Derivative investments can be volatile and may be less liquid than other investments. As a result, the value of an investment in the Fund may change quickly and without warning you may lose money. A fund that has a portfolio that is concentrated in the securities of issuers in a particular industry or group of related industries, may be adversely affected by the performance of those securities, and more susceptible to adverse economic, market, political, or regulatory occurrences affecting that industry or group of related industries.

While the Fund is actively managed, the Fund’s investment process is heavily dependent on quantitative models and the models may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Efficient Rare Earth Plus Strategic Metals Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.