Stock Buybacks Can Battle the Bear

Published March 8, 2022

Jeff Weniger, CFA

Head of Equity Strategy

The true investment challenge is to perform well in difficult times.

–Seth Klarman

Navigating 2022 has been an exercise in managing volatility.

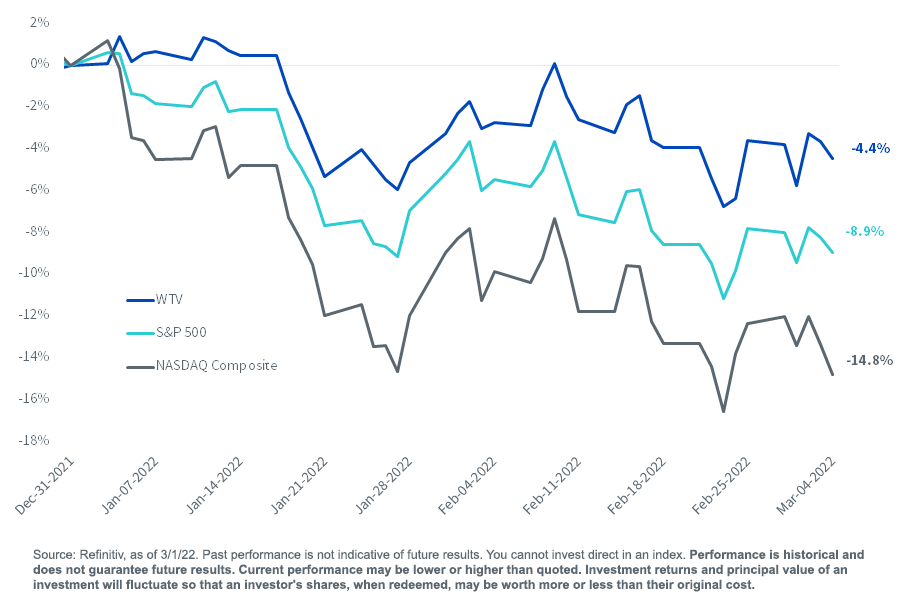

On top of ugly market action late last year, the pain has continued in this year’s first two months. Anything with a whiff of speculative flavor has a target on its back. While the NASDAQ Composite Index is off 14.8% YTD, and the S&P 500 has fallen 8.9%, our buyback-focused concept—the WisdomTree U.S. Value Fund (WTV)—has only given back 4.4% at NAV.

Figure 1: Year-to-Date Returns

For the most recent month-end and standardized performance click here.

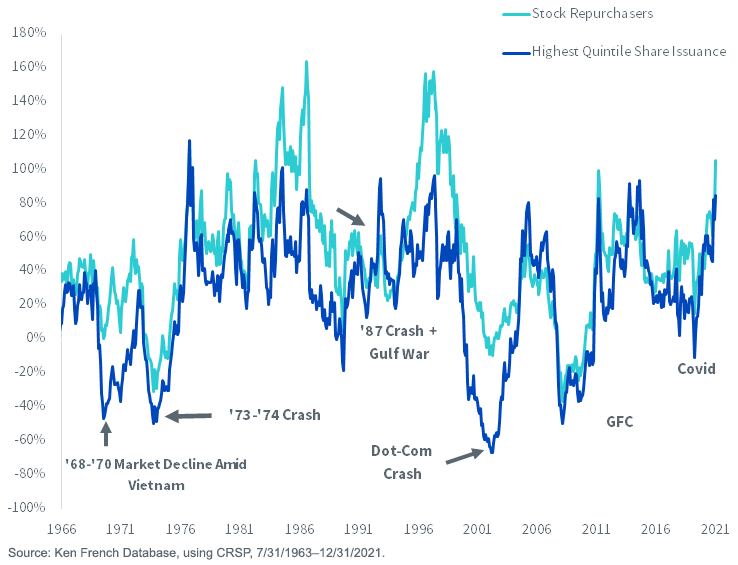

That isn’t surprising. The six major bear markets of the last half-century devastated companies that were heavy equity issuers, the kinds of stocks WTV's buyback screen tends to avoid. In crashes, the diluters plunged. While “nobody makes money in a bear market,” owners of the “buybackers” lived to see another day.

Figure 2: Three-Year Cumulative Return by Share Issuance

For example, look at the 1968–1970 bear market. The heaviest shareholder diluters were halved. Then they caught a three-year rally, only to be halved again in the 1973–1974 bear market.

Or the dot-com wreck. The big diluters declined by two-thirds over three years. In all three of those bear markets—and in the others—the stock repurchasers remained standing.

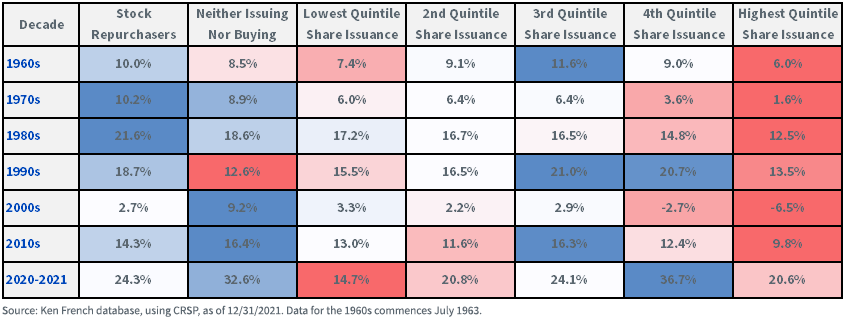

The red-and-blue color scheme of figure 3 speaks for itself.

Figure 3: Stock Market Returns, 1963–2021, Ranked by Share Buybacks vs. Share Issuance

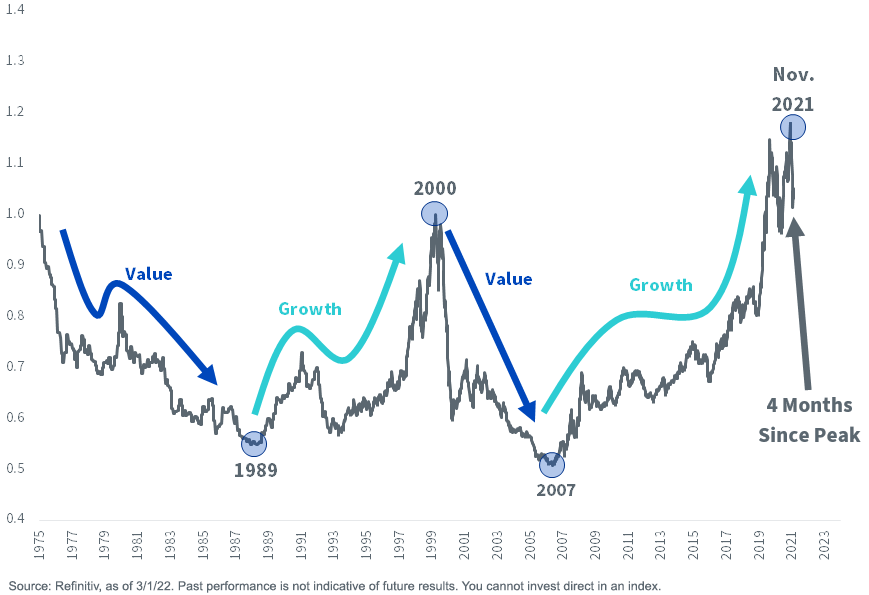

I’m thinking maybe we are in the first inning of a multiyear value cycle (figure 4). If I am right, the diluters are to be avoided.

Figure 4: S&P 500 Growth Relative to S&P 500 Value

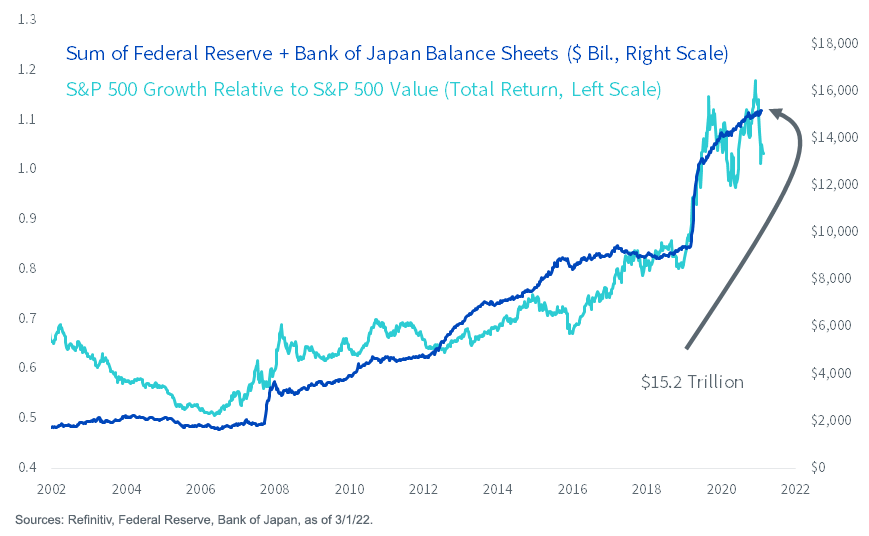

Many market watchers, including myself, suspect figure 5 explains growth versus value since the global financial crisis. So long as the Fed and other central banks were expanding their balance sheets to maintain zero interest rates, the present value math on growth stocks’ distant cash flows could justify big valuations (figure 5). A few months ago, when investors came to realize the monetary regime was set to flip, the tables turned.

Figure 5: Growth vs. Value: Dependent on Central Banks’ Bond Purchases

We recently cut WTV's expense ratio to 0.12%.

It has a net buyback yield of 5.6%, which is akin to a $10 billion market cap company buying back $560 million worth of stock in a year. That is four times as high as the S&P 500’s net buyback yield of 1.4%.

WTV has annually beaten both the S&P 500 Value and the Russell 1000 Value Indexes by more than a percentage point since its inception a generation ago through March 7, 2022. It has zero exposure to share diluters.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. While the Fund is actively managed, the Fund’s investment process is expected to be heavily dependent on quantitative models, and the models may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

Related articles

Two Prices, One Fund: Understanding NAV and Market Price in ETFs

Built for Any Market: How Blending Growth and Value Creates a Stronger Core

When AI Leaves the Screen and Enters the Physical World

Behind the Charts: Is the Energy Trade Running Out of Fuel?

Quality as a Foundation in an Uncertain World

The Company at the Center of the AI Economy

A Dog, a Diagnosis and a Different Way to Understand AI

The Market's Pendulum May Be Swinging Back to Value

Rising Through Discipline: Why DGRW and DDWM Are Earning Their Upgrades

About the contributor

Jeff Weniger, CFA

Head of Equity Strategy

Jeff Weniger, CFA, has been with WisdomTree since 2017 and serves as the Head of Equities. He shapes the firm’s market outlook through a combination of macroeconomic and fundamental analysis. With more than two decades in investment strategy, Jeff is known for his work on market cycles and valuations. Before joining WisdomTree, Jeff was with BMO Private Bank and BMO Global Asset Management for 11 years. At BMO, he sat on the firm’s Asset Allocation Committee and co-managed ETF model portfolios across the U.S. and Canada. In 2013, at age 32, he became the youngest member of BMO’s Global Investment Forum. When he left BMO to come to WisdomTree, his final role was Director, Senior Strategist in the Office of the CIO in 2017.

Jeff is a frequent television guest on networks such as CNBC, Bloomberg, and Schwab, with regular print appearances in The Wall Street Journal, Barron’s and Reuters. He also appears weekly on the Behind the Markets podcast and is a regular on SiriusXM’s The Business Briefing. On X, Jeff has developed one of the larger followings in financial media. He earned a B.S. in Finance from the University of Florida and an MBA from the University of Notre Dame. He has held the CFA charter since 2006.