QGRW

U.S. Quality Growth Fund

Published April 6, 2026

Global Head of Research

This year’s keynote from Jensen Huang arrives at a moment when artificial intelligence is moving from experiment to infrastructure. The early phase of AI, often noted as the training of giant models, has already reshaped the technology landscape. But the next phase is about deploying intelligence everywhere: in enterprise software, robotics, autonomous systems, and global data centers.

The company is no longer simply a semiconductor firm. Nvidia has quietly become the operating system of the AI economy. In fact, thinking about Nvidia solely as a company that builds chips risks missing the broader vision articulated by Jensen Huang. Since ChatGPT’s release in 2022, Nvidia has positioned itself as being heavily involved in the entire technological stack that modern AI depends on: silicon, networking, software frameworks, developer platforms, and increasingly the tools for building autonomous agents.

And the company has trained us that GTC is where the blueprint is revealed.

The 2026 event showcased the next generation of Nvidia’s AI infrastructure roadmap,3 centered around the Vera Rubin platform, the successor to Blackwell, and its expansion into full-scale “AI factory” systems. Rather than focusing solely on raw compute, Rubin is designed to optimize the economics of inference, dramatically increasing token throughput while lowering cost per token. Nvidia highlighted gains far beyond traditional scaling expectations, with systems engineered to deliver step-function improvements in performance per watt and overall token production.

Critically, Nvidia also unveiled a new architectural direction by integrating Groq’s LPU4 technology, featuring massive on-chip SRAM5 and deterministic execution, into the Rubin ecosystem. This combination is designed to extend performance into ultra-low-latency, high-value inference workloads, reinforcing Nvidia’s strategy of co-optimizing hardware, software, and system design around the emerging “AI factory” model of computing.

The first wave of generative AI was about training models, an extremely compute-intensive process dominated by large technology firms. But the long-term opportunity lies in inference, the act of running those models billions or trillions of times every day in real-world applications. Many estimates suggest inference could represent the majority of the future AI compute market.

Nvidia reportedly spent roughly $20 billion to license Groq’s technology and bring its team in-house,6 a move that raised an obvious question heading into GTC: What, exactly, did they buy?

The keynote provided a clear answer. What Nvidia acquired was not just another chip, but a fundamentally different approach to inference. Groq’s Language Processing Unit (LPU) is built around deterministic execution and massive on-chip SRAM, minimizing reliance on external memory, such as High-Bandwidth Memory (HBM). The result is a system purpose-built for token generation, delivering ultra-low latency and extremely high tokens-per-second throughput for what were referenced as ‘AI factories’.

But the real insight is how Nvidia is deploying it. Rather than replacing GPUs, Groq’s architecture is being tightly integrated into the Vera Rubin platform, where it handles the most latency-sensitive portion of inference, token decoding, while GPUs manage the heavier compute and memory workloads.

This is a shift in how AI infrastructure is designed. Training created the first wave of AI demand, but inference, running models continuously at scale, is now the economic engine. By combining high-throughput GPUs with low-latency LPUs, Nvidia is effectively disaggregating inference itself.

What they bought wasn’t just speed. Nvidia bought a new layer in the AI stack—one optimized for the economics of intelligence at scale.

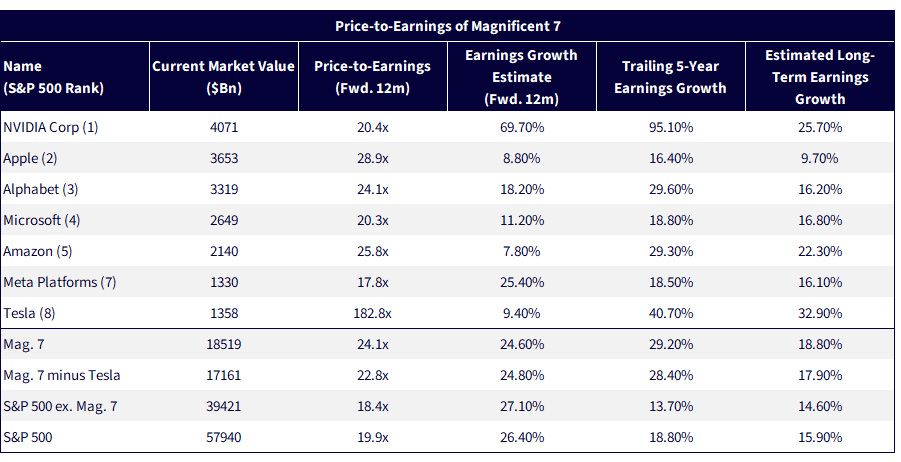

The company that we just noted is at the center of the AI story cannot possibly find itself in the ‘value’ style—or could it? In Figure 1, we look at certain statistics that may make a compelling case for this conclusion:

Our bottom line is this—even if the growth forecasts for Nvidia’s earnings are too high, there is still such a gap between what is predicted for the company versus what is predicted for the broad S&P 500 Index that for investors to impute a similar forward P/E ratio for both, in our opinion, tilts the potential risk/reward trade-off towards Nvidia. Each of the so-called Magnificent 7 companies that has a higher forward P/E ratio than Nvidia also has a significantly lower forward-looking earnings growth forecast. Tesla, admittedly, is a bit of an outlier in that the forward P/E ratio is 182.8x, the estimated earnings growth for the forward 12 months is 9.4%, and then the estimated long-term earnings growth for Tesla shows around 32.9%. While this is higher than Nvidia’s figure, we recognize that Tesla is bringing all sorts of new things to the market to give this a chance to happen. Nvidia is delivering on a more established stream of business execution.

Sources: WisdomTree, FactSet, S&P, as of 3/30/26. *Calendar year price-to-earnings and earnings growth based on median analyst estimates. **Trailing 3-year where 5-year is not available. Growth is annualized. ***Estimated Long-Term Growth is annualized and based on median analyst earnings growth estimates over the next 3 years. Trailing 5-year Earnings Growth and Estimated Long-Term Earnings Growth as of 2/28/26. All other data as of 3/29/26. Aggregate metrics in italics shown as weighted averages. You cannot invest directly in an index.

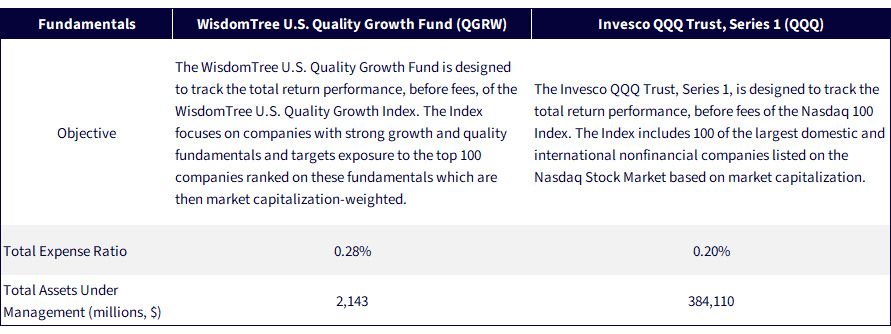

For many, the Nasdaq 100 Index, the total returns of which are tracked by Invesco QQQ Trust, Series 1 (QQQ), has been synonymous with exposure to big tech. But there's an important nuance hiding in plain sight: the Nasdaq 100 Index doesn't explicitly target growth or quality. It simply selects the 100 largest non-financial stocks trading on the Nasdaq exchange.7 This means that while QQQ gives investors access to scale, it does not optimize for company fundamentals. As the market begins to differentiate more sharply within the mega cap cohort, index design can become an active decision, even in passive wrappers.

Enter the WisdomTree U.S. Quality Growth Fund (QGRW), a fundamentally driven alternative, designed to track the total return performance of the WisdomTree U.S. Quality Growth Index, which focuses toward the more profitable, higher-growth names in large-cap U.S. equities. There is a direct emphasis on return on equity, return on assets and earnings growth, as compared to Nasdaq 100 Index constituents, which are not included due to any direct requirements like this. For investors who believe the AI boom still has legs, but want a basket built on enduring fundamentals, not just market cap, QGRW may offer the right lens for this next leg of the tech trade.

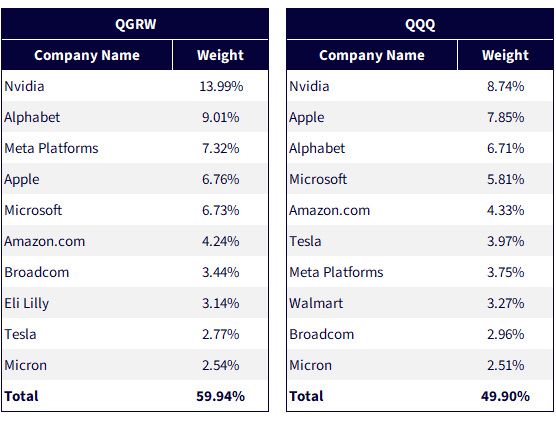

In Figure 2, we look at the top 10 holdings of QGRW against those of QQQ. What stands out starkly is the difference in weight for Nvidia, as of February 28, 2026:

The reality is we do not know what Nvidia’s return will be, but it is clear that the two strategies have significantly different exposure which could lead to a greater potential for differentiated returns.

Sources: WisdomTree, FactSet and Morningstar, with data as of February 28, 2026. Holdings subject to change.

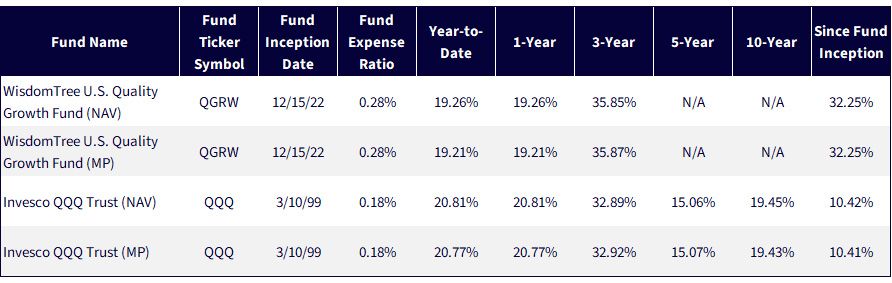

Figures 3a and 3b paint the picture of returns. Since QGRW's inception, which corresponds to the longest common period, QGRW was able to outperform QQQ by nearly 2% per year, it is clear in Figure 3a. However, in the early part of 2026, which has been characterized by a potential rotation away from growth stocks and more towards value stocks, QGRW has underperformed QQQ by about 2%, though both strategies were negative year-to-date as of this writing.

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of March 31, 2026, but showing returns for the period ended March 30, 2026 for Figure 3a and December 31, 2025 for Figure 3b. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: QGRW, QQQ.

Nvidia’s GTC 2026 keynote reinforced a simple but powerful idea: we are no longer investing in companies, but in the infrastructure of intelligence itself. As AI shifts from training to inference, from models to agents, and from tools to autonomous systems, the economic center of gravity is moving toward platforms that can scale intelligence efficiently. Nvidia sits at that center. But as leadership within mega-cap technology begins to differentiate, how investors access that exposure matters. Strategies like QGRW, which emphasize quality and growth alongside scale, may offer a more intentional way to participate in what could be one of the most consequential technology cycles of our time.

Sources: WisdomTree, Invesco, with Assets Under management as of March 13, 2025. Subject to change.

1 Graphics processing unit.

2 Source: NVIDIA Corporation. (2026, March 3). NVIDIA CEO Jensen Huang and global technology leaders to showcase age of AI at GTC 2026. NVIDIA Newsroom.

3 References to the 2026 Nvidia GTC keynote are sourced from: Huang, J. (2026, March 16).

4 LPU stands for language processing unit.

5 SRAM stands for static random access memory.

6 Source: Financial Times. (2026, March).

7 Source: Nasdaq, Inc. (2024). Nasdaq-100 Index methodology. Nasdaq Global Indexes.

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund to fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund.

QGRW: There are risks associated with investing, including possible loss of principal. Growth stocks, as a group, may be out of favor with the market and underperform value stocks or the overall equity market. Growth stocks are generally more sensitive to market movements than other types of stocks. The Fund is non-diversified, as a result, changes in the market value of a single security could cause greater fluctuations in the value of Fund shares than would occur in a diversified fund. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

For QQQ’s risk disclosures, click here.

U.S. Quality Growth Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.