Inflation Fears Are Rising Again. WTIP Was Ready.

Published April 7, 2026

Behnood Noei, CFA

Director, Fixed Income

Key Takeaways

- Escalating Middle East tensions and the Strait of Hormuz closure have reignited inflation fears, pushing oil higher and lifting short-term inflation expectations, creating a timely entry point for investors to consider inflation-hedging strategies such as the WisdomTree Inflation Plus Fund (WTIP).

- Despite a sharp drawdown in traditional hedges such as gold (down over 15%), WTIP has gained 6.54% during the conflict and approximately 12% year to date, highlighting how its dynamic commodity positioning and TIPS exposure may outperform in volatile, inflationary regimes.

- WTIP's momentum-driven commodity allocation—tilting into strength like crude oil while avoiding weak assets—demonstrates a differentiated, systematic approach to inflation protection that investors can use to navigate both expected and surprise inflation shocks.

Over the past month, markets have been rattled by the escalating conflict in the Middle East. Risk assets were the first to react, but the damage didn’t stop there. Even traditional safe havens, including gold and other precious metals, have fallen sharply. At the same time, the U.S. dollar has strengthened, and central banks across developed markets, including the Federal Reserve, have shifted toward a more hawkish tone. In a landscape where both risk and safety seem uncertain, it’s worth taking a closer look at how one of our strategies designed for turbulent inflationary environments, the WisdomTree Inflation Plus Fund (WTIP) has performed.

How Did We Get Here?

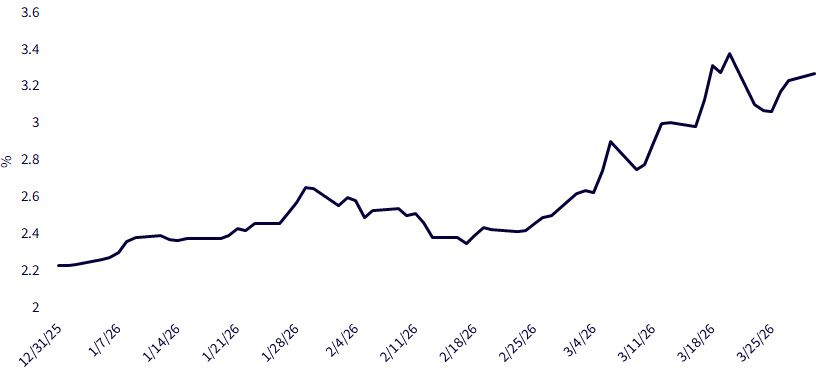

The recent closure of the Strait of Hormuz has pushed oil prices significantly higher, bringing inflation risk back to the top of the list of concerns for the market. For many investors, this feels uncomfortably familiar. The post-COVID inflation shock is still fresh, and the prospect of another prolonged inflationary period is enough to cause heartburn for investors who are not positioned appropriately. While the underlying cause of this inflation spike differs from the last time around (monetary response to COVID), the implications are similar: rising costs, shifting policy expectations, and a growing need for effective hedges. Near-term inflation expectations have already begun to climb, and if the conflict persists, those pressures may only intensify.

Figure 1: 1-Year Zero-Coupon Inflation Swaps

Source: WisdomTree, Bloomberg, as of 03/30/2026. 1-year Zero-coupon swap: A derivative used to transfer inflation risk from one party to another through an exchange of cash flows. In a zero-coupon inflation swap, only one payment is done at maturity where one party pays a fixed rate on a notional principal amount, while the other party pays a floating rate linked to an inflation index.

WTIP’s Performance

WTIP was designed for moments like this. The strategy blends commodities with U.S. Treasury Inflation-Protected Securities (TIPS) to address different types of inflationary shocks (expected and unexpected). TIPS tend to hedge expected inflation, though they usually react with a bit of a lag. Commodities, by contrast, have historically responded more quickly when inflation surprises to the upside (unexpected inflationary shocks) and often move ahead of broader trends. By combining the two, WTIP aims to create a more well-rounded hedge, rather than depending on any single approach to carry the load.

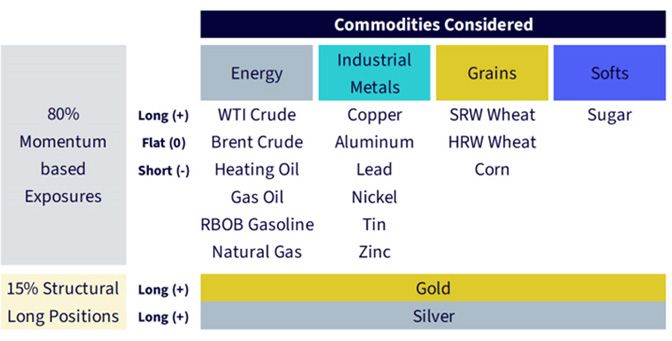

The commodity component of the strategy is particularly dynamic. Eighty percent of the allocation is driven by momentum-based models that evaluate 16 commodity futures. Each is assigned a signal—long, short or flat— based on its own price behavior. Exposure is then distributed evenly across commodities with active signals, allowing the portfolio to adapt as conditions change. Alongside this, there is a structural allocation to precious metals, with 7.5% each dedicated to gold and silver.

Figure 2: WTIP Commodity Allocation Framework

Source: WisdomTree.

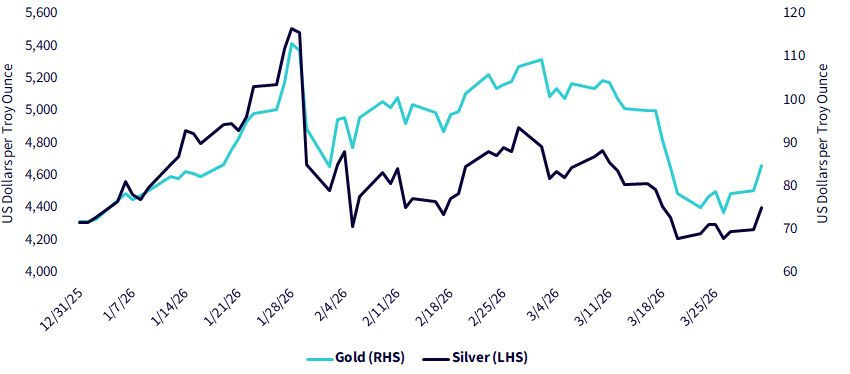

The current environment is a perfect example of how this design has translated into performance. Despite the significant declines in gold and silver, down more than 13% and 35%, respectively, from their all-time highs at the beginning of the conflict, WTIP has managed to post a gain of 6.54% over the same period. That brings its year-to-date return to around 12%. In a market where many asset classes are firmly in bear territory, this outcome is extraordinary.

Figure 3: Gold and Silver Prices YTD

Source: WisdomTree, Bloomberg, as of 03/30/2026. RHS = Right-hand side. LHS = Left-hand side.

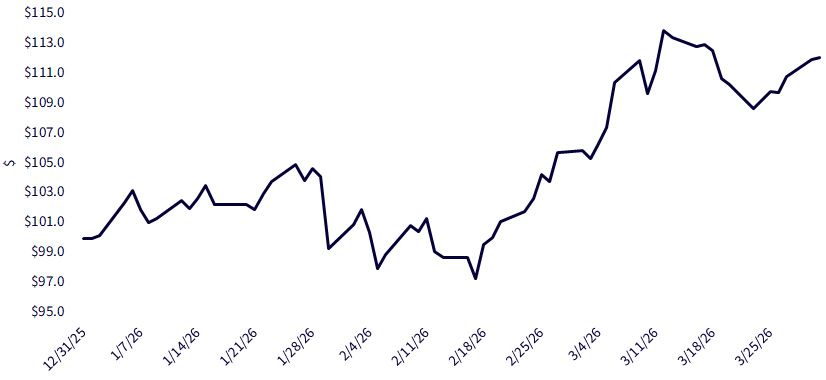

Figure 4: Growth of $100 Invested in WTIP at the Beginning of the Year

Source: WisdomTree, as of 03/29/2026.

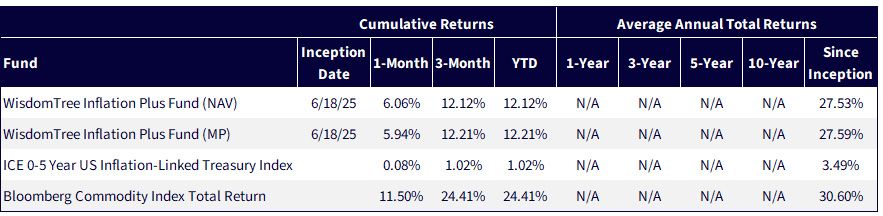

Figure 5: Performance

Source: WisdomTree, as of 03/31/2026. Figure 5 presents performance for the WisdomTree Inflation Plus Fund (WTIP). The Fund’s Total Annual Fund Operating Expenses, before fee waivers or expense reimbursements, are 0.66% as stated in the prospectus. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

Much of this can be attributed to the aforementioned systematic, momentum-based approach embedded in the strategy. By evaluating each commodity relative to its own price history, the model determines whether to take a long or short position, striving to sidestep areas of weakness while leaning into strength. This has helped the fund avoid big drawdowns in certain assets, such as bitcoin exposure, while increasing exposure to areas benefiting from the current environment, including crude oil. The diversification across commodities, combined with the complementary role of TIPS, has further contributed to the performance during a highly volatile period.

Conclusion

In moments like these, when markets are extremely volatile, the value of thoughtful portfolio construction becomes increasingly clear. WTIP's performance this year underscores how a well-designed strategy may help absorb shocks rather than amplify them.

By combining different inflation-sensitive assets and layering in a disciplined, systematic approach, WTIP has held up in an environment where most asset classes, including traditional safe havens, have bled lower. More importantly, it aims to provide investors with a measure of stability at a time when stability has been in short supply.

Important Risks Related to this Article

Performance is historical and does not guarantee future results.

There are risks associated with investing including possible loss of principal. Inflation-protected U.S. Treasury Bonds (“TIPS”), can provide a hedge against inflation, as the inflation adjustment feature helps preserve the purchasing power of the investment. Because of this inflation adjustment feature, inflation protected bonds typically have lower yields than conventional fixed rate bonds and will likely decline in price during periods of deflation, which could result in losses. Fixed income securities are subject to interest rate, credit, inflation, and reinvestment risks. Generally, as interest rates rise, the value of fixed-income securities falls. The value of commodities and commodity-linked derivative instruments typically is based upon the price movements in other asset classes. An active trading market may not exist for certain commodities. The Fund is subject to risks related to rolling futures contracts. The price of futures contracts further from expiration may be higher (“contango”) or lower (“backwardation”), which can impact the Fund’s returns. Because of the frequency with which the Fund expects to roll futures contracts, the impact of such contango or backwardation may be greater than the impact would be if the Fund experienced less portfolio turnover. In addition, bitcoin exchange-traded products (ETPs) and bitcoin futures are relatively new and the markets may be less developed. They are subject to unique and substantial risks, and historically, have been subject to significant price volatility. As a result, the markets for bitcoin futures and bitcoin ETPs may be less developed, and at times, potentially less liquid and more volatile, than more established commodity futures and ETP markets. While the bitcoin futures market has grown substantially since bitcoin futures commenced trading, there can be no assurance that this growth will continue. The Fund may invest in the WisdomTree Bitcoin Fund, a bitcoin exchange traded product, sponsored by an affiliate of the Fund’s adviser. The Fund will not invest in bitcoin directly. Please read the Fund's prospectus for specific details regarding the Fund's risk profile.

Categories

About the contributor

Behnood Noei, CFA

Director, Fixed Income

Behnood Noei serves as Director of Fixed Income at WisdomTree Asset Management, where he develops the firm’s suite of fixed income and currency exchange-traded funds and enhances existing investment processes. Behnood has 11 years investment experience in portfolio management and quantitative research. Prior to joining WisdomTree in 2022, Behnood was a portfolio manager and developer of some of the fixed income ETFs at J.P.Morgan Asset Management, where he was directly responsible for managing more than 7 Fixed Income ETFs and multiple SMAs with more than $13Billion in assets. He graduated from The Ohio State University with Master of Science degree in Finance and is a CFA charter holder.