HYIN

Private Credit & Alternative Income Fund

Published March 26, 2026

Director, Fixed Income

Over the past couple of months, private credit has moved from a relatively hot corner of the market into an area of concern. What was once viewed as a steady, income-generating segment is now facing a wave of scrutiny. Investors have begun to reassess their exposure, particularly to areas tied to software and technology, and the shift has been swift. Publicly traded investment companies focused on private credit have seen their shares fall between 25% and 40% year to date, reflecting a meaningful repricing of risk. In this blog post, we will take a look at how things started and how systematic we believe these concerns are.

Things really started to shift when Blue Owl put limits on quarterly redemptions for a couple of its non-traded BDCs. Other managers followed with their own restrictions, and around the same time, reports surfaced about fraud tied to a few private credit funds. Put all of that together, and it’s not surprising that investors, who had come to see this space as relatively stable, are starting to feel uneasy.

As worries have picked up, people have started looking back at past market stress for comparison. In some cases, the conversation has even drifted toward 2008 and sub-prime crisis, with questions about whether problems in private credit could spill over into the broader economy.

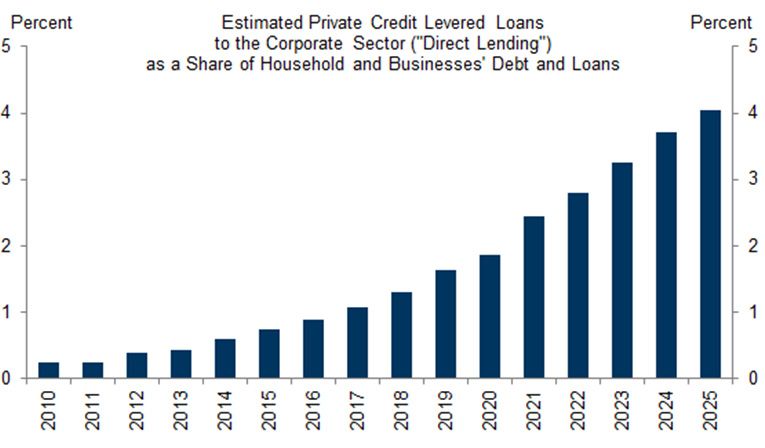

To understand the potential impact, it helps to start with the size of the market. The private credit industry currently holds about $1.7 trillion in leveraged loans to the corporate sector, accounting for roughly 4% of all credit to the private non-financial sector. That’s a meaningful figure, but still relatively modest in the context of the overall credit system. While transparency in private credit is limited compared to public markets, the data that is available suggests that loan performance as of the fourth quarter of 2025 has remained broadly in line with its average since 2023.

Source: Goldman Sachs Global Investment Research, Pichbook, LCD, Preqin, LSEG Data & Analytics, BDC Collateral, Federal Reserve

That said, the headlines didn’t just appear out of thin air. There have been a few cases of fraud linked to larger loans, and with how quickly private lending has grown in recent years, it’s fair to question how tight underwriting and oversight have really been. On top of that, the outlook for the software sector, where private credit has had meaningful exposure, has changed, which only adds to the uncertainty.

Even under more stressed scenarios, however, the broader economic impact appears contained. A modest increase in default rates to the 3–4% range would likely result in only a small drag on GDP. A more severe scenario, with defaults rising toward the 10% peak reached during the 2008 financial crisis, would have a larger effect. But even in that case, the impact remains limited relative to the scale of the economy.

There are a few reasons for this. First, the private credit sector is still relatively small compared to the broader financial system. Second, its funding structure is less prone to sudden withdrawals, reducing the risk of rapid, destabilizing outflows. And third, private credit funds generally operate with lower levels of leverage than traditional banks or other financial institutions. These characteristics help cushion the system from the kind of cascading effects that defined past crises.

Looking ahead, it’s reasonable to expect some tightening in private credit lending. Managers are likely to become more selective, and pricing may adjust to reflect the changing environment. At the same time, other parts of the credit market are showing resilience. Bank lending to businesses has picked up recently, and corporate balance sheets remain in solid shape. Demand tied to ongoing investment in AI is also likely to support credit growth, providing a counterbalance to weakness in other areas.

The more meaningful risk may not come from private credit alone, but from broader shifts in financial conditions. If uncertainty around AI or other macro factors leads to wider credit spreads across the board, the impact could extend beyond any single segment. In that context, private credit becomes part of a larger story rather than the central driver.

For investors navigating this environment, structure and diversification matter more than ever. This is where strategies like WisdomTree Private Credit and Alternative Income Fund (HYIN) come into focus. Rather than relying on exposure to a single manager or fund, HYIN invests in listed credit vehicles. Its performance is tied to the market prices of publicly traded alternative credit instruments, such as BDCs, credit closed-end funds, and mortgage REITs, rather than headlines surrounding any individual firm.

That distinction is important. Because HYIN trades in the public market, investors are not exposed to the same redemption constraints that have recently made news. Liquidity is determined by market trading, not by a manager’s decision to gate withdrawals. In addition, HYIN offers diversification across multiple sectors, reducing reliance on any one issuer or strategy. As of February month-end, HYIN had only around 25% allocation to BDCs and private credit.

In a moment when sentiment can shift quickly, having that kind of structure can make a meaningful difference. Private credit may continue to face scrutiny in the near term, but a closer look suggests that the risks, while real, are more contained than some of the louder comparisons might imply.

There are risks associated with investing, including the possible loss of principal. The Fund invests in private credit and alternative credit sectors through investments in underlying closed-end investment companies (“CEFs”), including those that have elected to be regulated as business development companies (“BDCs”), and real estate investment trusts (“REITs”). The value of the underlying securities held by a CEF could decrease or the portfolio could become illiquid. The value of a CEF can decrease due to movements in the overall financial markets. Federal securities laws impose restraints upon the organizations and operations of BDCs that can negatively impact the performance of a BDC. BDCs generally invest in less mature private companies, which involve greater risk than well-established, publicly traded companies and are subject to high failure rates among the companies in which they invest. By investing in REITs, the Fund is exposed to the risks of owning real estate, such as decreases in real estate values, overbuilding, increased competition and other risks related to local or general economic conditions. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Private Credit & Alternative Income Fund

Director, Fixed Income

Behnood Noei serves as Director of Fixed Income at WisdomTree Asset Management, where he develops the firm’s suite of fixed income and currency exchange-traded funds and enhances existing investment processes. Behnood has 11 years investment experience in portfolio management and quantitative research. Prior to joining WisdomTree in 2022, Behnood was a portfolio manager and developer of some of the fixed income ETFs at J.P.Morgan Asset Management, where he was directly responsible for managing more than 7 Fixed Income ETFs and multiple SMAs with more than $13Billion in assets. He graduated from The Ohio State University with Master of Science degree in Finance and is a CFA charter holder.