How to Mitigate Software Exposure in Bonds

Published March 25, 2026

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Andrew Okrongly, CFA

Director, Model Portfolios

Key Takeaways

- Rising credit spread volatility and renewed liquidity concerns, particularly in private credit and BDCs are refocusing investors on structure, where more liquid high yield exposure via HYZD may offer a timely defensive pivot with enhanced yield potential.

- AI-driven disruption is increasing dispersion in software credit fundamentals, disproportionately impacting private credit and leveraged loans, while high yield’s approximately 2% software exposure in HYZD provides a strategic way to mitigate sector-specific downside risk.

- As retail capital flows into less liquid credit structures amplifying hidden risks, investors may consider exposure to high yield through HYZD to gain transparency, daily liquidity and higher quality issuer exposure without sacrificing income opportunities.

Prior to the war in the Middle East, the U.S. financial markets were being confronted with headlines and attendant concerns surrounding the credit markets. Obviously, the storyline involving the Middle East conflict is still taking center stage and will likely continue to impact markets in the weeks ahead. However, we continue to believe that once the markets get a sense that the situation in the Middle East begins to de-escalate, the market focus could shift back to a pre-conflict setting.

After several months of relative calm, credit markets have been a bit noisier. Spreads have drifted wider, and questions around liquidity and fundamentals—especially in private credit and BDCs—have resurfaced.

Two forces are driving most of the conversation. The first is a structural shift in liquidity, as more capital—particularly retail—has moved into less liquid credit vehicles. The second is AI-driven disruption, which is beginning to reshape parts of the economy, especially software.

These forces do not impact all credit equally. To see why, it helps to break credit into three broad buckets: high yield (HY), broadly syndicated/leveraged loans (BSL) and private credit (PC)—and focus less on labels and more on structure.

Structure Drives Outcomes: Liquidity and Credit Quality

High yield is the most liquid and accessible, widely held through mutual funds and ETFs. It also tends to be higher quality, with larger issuers. The benefit is daily liquidity and real-time pricing; the tradeoff is more visible volatility as markets adjust quickly.

Leveraged loans are somewhat less liquid and more institutional, but still broadly accessible. Their floating-rate structure reduces interest rate sensitivity, while strong CLO demand provides a steady source of support. This creates a middle ground: less rate risk, but greater exposure to credit fundamentals and default cycles.

Private credit looks similar to leveraged loans—senior, floating-rate lending to corporate borrowers—but without a liquid secondary market. Returns are based on periodic NAV marks rather than continuous pricing. The result is a different experience: smoother returns day to day, but less immediate price discovery, with risk tending to be realized over time rather than instantly.

AI, Software and Where Risk Concentrates

Software has historically supported higher leverage due to recurring revenues and strong margins. AI doesn’t necessarily change that overnight, but it does introduce more dispersion—across pricing power, growth, and competitive dynamics.

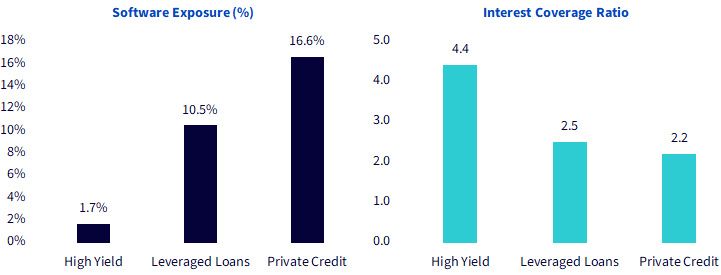

That matters because exposure to software varies across credit:

- High yield has relatively limited direct exposure

- Leveraged loans have moderate exposure

- Private credit tends to have the highest concentration, especially in middle-market borrowers

Figure 1: High Yield Offers Lower Exposure to Software and Higher Interest Coverage Ratios Than BSL, PC

Sources: BofA Global Research, ICE Data Indices, LLC, LCD, Preqin, Bloomberg.

It is not just about exposure—it is about borrower profile. Software companies financed in private credit tend to be smaller, more leveraged, and more dependent on growth assumptions. Loan issuers are generally larger but still below high yield in diversification and resilience. High yield issuers, on average, are the largest and most diversified.

Credit is often treated as a single allocation, but structure matters.

High yield offers liquidity, transparency, and generally higher-quality exposure. Leveraged loans provide floating-rate income with strong technical support, sitting higher in the capital structure but with more exposure to fundamental credit risk. Private credit extends that same lending into less liquid structures, with more concentrated exposures and a different timing of return realization.

Solution

For investors looking for that ‘plus’ component in their fixed income portfolio, we believe the U.S. high yield sector offers a way to mitigate software exposure while enhancing yield opportunities.

The WisdomTree Interest Rate Hedged High Yield Bond Fund (HYZD) is an approach that fits these criteria and can serve as an alternative exposure to bank loans in a bond portfolio. As of this writing, HYZD's exposure to software and technology stands at only 2%, well below the figure one typically finds in the leveraged loan space.

As liquidity evolves and AI begins to reshape certain sectors, the distinctions between high yield, loans, and private credit are becoming more important.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. High-yield or “junk” bonds have lower credit ratings and involve a greater risk to principal. Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. The Fund seeks to mitigate interest rate risk by taking short positions in U.S. Treasuries (or futures providing exposure to U.S. Treasuries), but there is no guarantee this will be achieved. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effects of varied economic conditions.

Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner, or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. The Fund may engage in “short sale” transactions where losses may be exaggerated, potentially losing more money than the actual cost of the investment and the third party to the short sale may fail to honor its contract terms, causing a loss to the Fund. While the Fund attempts to limit credit and counterparty exposure, the value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Due to the investment strategy of the Fund, it may make higher capital gain distributions than other ETFs. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

About the contributors

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.

Andrew Okrongly, CFA

Director, Model Portfolios

Andrew Okrongly joined WisdomTree in 2022 as a Director on the Model Portfolios Team. He is responsible for the design and ongoing management of model portfolios and custom solutions for portfolio managers and advisors. Andrew is also a member of the Model Portfolio Investment Committee. Prior to joining WisdomTree, Andrew was a Director on the Outsourced Chief Investment Officer (OCIO) team at Commonfund, where he was responsible for macro-economic analysis and advising institutional clients on strategic and tactical asset allocation. Andrew began his career at BlackRock where he held a variety of fixed income and multi-asset investment roles. Andrew received a BBA degree from the University of Michigan and is a holder of the Chartered Financial Analyst designation.