WTPI

Equity Premium Income Fund

Published May 15, 2025

Global Head of Research

In recent months, equity markets have defied easy categorization. The S&P 500 Index posted its longest winning streak in 21 years, amid tariff overhangs, geopolitical tensions and growing uncertainty in corporate guidance.1 At the same time, U.S. gross domestic product (GDP) contracted by 0.3% in Q1,2 largely due to front-loaded imports ahead of tariff hikes, which may mask underlying domestic resilience. This mix of strong earnings, aggressive buybacks and persistent fragility in macroeconomic indicators has created a fog that even seasoned investors struggle to navigate. Are we witnessing the tail end of post-pandemic momentum or the early tremors of a larger reckoning?

Professional sentiment offers no clear resolution. According to Barron's Big Money poll, institutional investors are the most bearish they've been in nearly 30 years, with just 26% identifying as bullish and 32% as outright bearish.3 The skepticism is rooted in stretched valuations, tariff risks and an earnings outlook plagued by uncertainty. Even among companies posting solid results, there is widespread reluctance to issue firm guidance.4 In response, some investors have turned to more defensive or contrarian exposures—international value stocks, dividend plays and even precious metals. But none of these solutions addresses the core dilemma: the direction of equities from here remains inherently unpredictable.

Given this backdrop, it's not surprising that income-oriented strategies are gaining renewed attention. Notably, the surge in corporate buybacks—$500 billion and counting in 2025—signals that companies themselves are favoring cash-return mechanisms over new growth investments.5 With volatility remaining elevated and realized returns uncertain, many investors are now looking at the volatility market itself as a source of return. Selling options, particularly in well-constructed, risk-managed strategies, may offer a compelling profile: monetizing fear and indecision while staying agnostic about market direction.

Put differently, when directional conviction is low, the premium in uncertainty becomes an asset class. These approaches do not require the market to rise—they simply need it not to collapse. And if one believes that valuations will remain bounded by macroeconomic policy and earnings uncertainty, then harvesting premium from that bounded volatility could represent one of the most rational income strategies in today's market.

This is a fertile hunting ground for strategies that tend to sell options and generate income. The two largest strategies in this category are6:

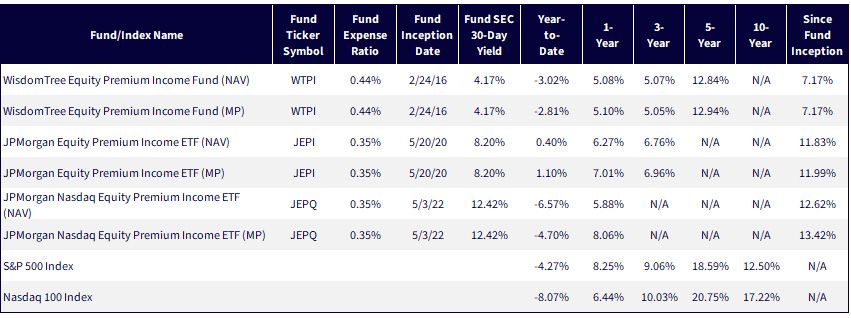

Both these strategies are selling call options and holding underlying equities. The WisdomTree Equity Premium Income Fund (WTPI) is also in the same Morningstar category, but it sells put options and then holds the premiums collected in U.S. Treasuries.

Have these three strategies delivered different return profiles or income levels? Let's see.

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 5/3/25, with returns as of 3/31/25. Fund SEC 30-Day Yield as of 3/31/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Prior to 4/4/25, WTPI was known as the WisdomTree PutWrite Strategy Fund (PUTW). On that date the Fund's investment policy changed. Prior to 10/24/22, the WisdomTree PutWrite Strategy Fund was named the WisdomTree CBOE S&P 500 PutWrite Strategy Fund and tracked the total return performance, before fees and expenses, of the CBOE S&P 500 PutWrite Index. The performance data quoted represents past performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: WTPI, JEPI, JEPQ.

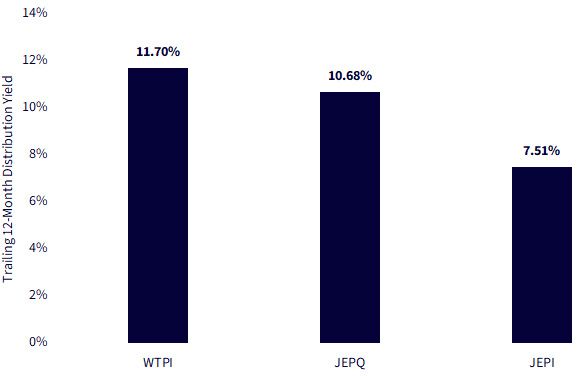

While we frequently discuss how income is merely one component of a strategy's total return, we know that many pay it particularly strong attention. Figure 2 looks at the trailing 12-month distribution yields of the aforementioned strategies as of April 30, 2025:

Sources: Specific fund pages on the WisdomTree and JPMorgan websites, with data as of 4/30/25, accessed on 5/5/25. Past performance is not indicative of future results.

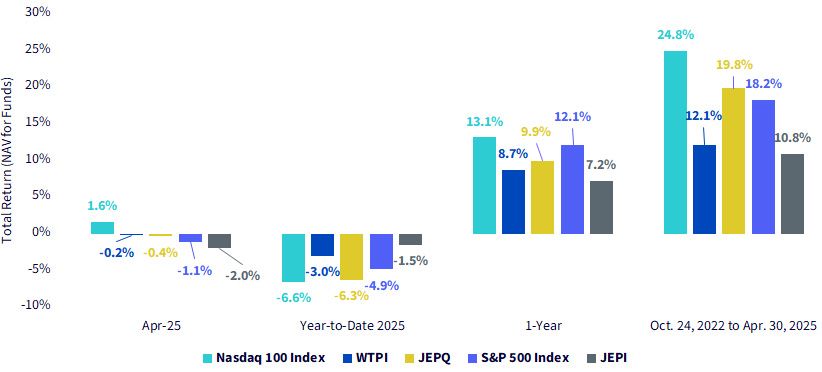

Figure 3 allows us to look at four distinct periods, recognizing that we are confined to a period from October 24, 2022, onwards. Prior to this date, WTPI was tracking a different underlying index that employed a different investment strategy.

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 5/3/25, with returns as of 4/30/25. NAV denotes total return performance at net asset value. Prior to 4/4/25, WTPI was known as the WisdomTree PutWrite Strategy Fund (PUTW). On that date the Fund's investment policy changed. Prior to 10/24/22, the WisdomTree PutWrite Strategy Fund was named the WisdomTree CBOE S&P 500 PutWrite Strategy Fund and tracked the total return performance, before fees and expenses, of the CBOE S&P 500 PutWrite Index. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: WTPI, JEPI, JEPQ.

In early May 2025, we have many investors searching for direction. Tariff policy is constantly evolving. While there is never certainty in markets, the double-digit returns experienced in 2023 and 2024 likely created a feeling of comfort that has long since dissipated. We note that a strategy of selling put options and collecting premium income has strong potential if the behavior of U.S. equities is more one of searching for direction and less one of excessive trending. A trailing 12-month distribution yield above 10% is also quite interesting for many.

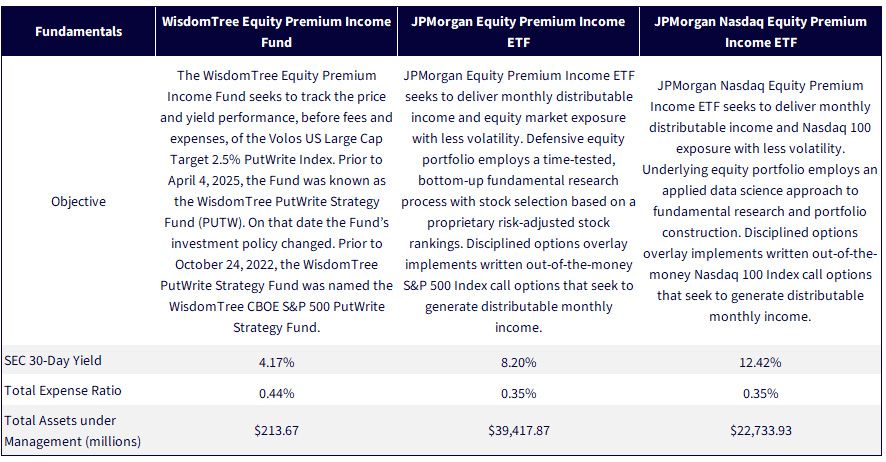

Figure 4: Additional Information

Sources: WisdomTree's Fund Compare tool and JPMorgan's specific fund pages on the JPMorgan website. Assets under management data is as of 3/31/25. Subject to change.

1 Source: M. Horan, "Stock Market Winning Streak Best in 21 Years. Why It's Looking Fragile," Barron's, 5/3/25.

2 Refers specifically to U.S. real GDP on a seasonally adjusted annual rate (SAAR) basis. This figure is for Q1 2025, based on the initial estimate released by the U.S. Bureau of Economic Analysis.

3 Source: V. Subbaraman, "America's Money Managers Are Bearish. That's Bullish," Barron's, 5/3/25.

4 Source: Horan, 5/3/25.

5 Source: C. Smith, "U.S. Companies Launch $500bn Share Buyback Spree in First Four Months of 2025," Financial Times, 5/5/25.

6 Ranking by assets under management as of most recent quarter-end, 3/31/25, with source Morningstar Direct.

WTPI: There are risks associated with investing, including the possible loss of principal. The Fund will invest in derivatives, including S&P 500 Index put options (SPX Puts). Derivative investments can be volatile, and these investments may be less liquid than securities, and more sensitive to the effects of varied economic conditions. The value of the SPX Puts in which the Fund invests is partly based on the volatility used by market participants to price such options (i.e., implied volatility). The options values are partly based on the volatility used by dealers to price such options, so increases in the implied volatility of such options will cause the value of such options to increase, which will result in a corresponding increase in the liabilities of the Fund and a decrease in the Fund’s NAV. Options may be subject to volatile swings in price influenced by changes in the value of the underlying instrument. The potential return to the Fund is limited to the amount of option premiums it receives; however, the Fund can potentially lose up to the entire strike price of each option it sells. Due to the investment strategy of the Fund, it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

JEPQ/JEPI: The price of equity securities may fluctuate rapidly or unpredictably due to factors affecting individual companies, as well as changes in economic or political conditions. These price movements may result in loss of your investment. Investments in equity-linked notes (ELNs) are subject to liquidity risk, which may make ELNs difficult to sell and value. Lack of liquidity may also cause the value of the ELN to decline. Since ELNs are in note form, and are subject to certain debt securities risks, such as credit or counterparty risk. Should the prices of the underlying instruments move in an unexpected manner, the Fund may not achieve the anticipated benefits of an investment in an ELN, and may realize losses, which could be significant and could include the Fund’s entire principal investment.

Equity Premium Income Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.