GGRA LN

WisdomTree Global Quality Dividend Growth UCITS ETF - USD Acc

Publié le 7 août 2024

Senior Associate, Quantitative Research and Multi Asset Solutions

It’s risk off with equities, bond yields, commodities and crypto down. A correction is underway. Bond yields have plunged on expectations of lower interest rates and safe-haven demand. H1 2024 saw risk assets perform well following better news on inflation than expected, increasing optimism about lower interest rates ahead and improving technology and artificial intelligence (AI) earnings. As we are now in the seasonally weak period of August and September a further correction in risk assets looks likely. A confluence of factors is behind the sell-off:

Our view remains that lower interest rates will boost equities over a 6-12 month time frame, assuming a recession is avoided. However, in the next few months, risk assets look vulnerable to further falls, suggesting that it may be too early to consider these as valuations are stretched, investment sentiment looks too optimistic, and recession risk appears high in the US. That being said, investors could position themselves to more opportunistic parts of the market within Equities.

Concerns around the breadth and sustainability of the mega cap narrative have been a critical factor supporting improving the performance of the equal-weighted version of the S&P 500 Index versus the market cap S&P 500 Index. Secondly, the gap in earnings growth expectations between the ‘Magnificent Seven1’ and the rest of the market is closing significantly towards the end of the year. While the Magnificent Seven exhibited considerably higher earnings growth in 2023 and the first half of 2024, the rest of the market is catching up. This should create opportunities for stocks outside those seven mega caps to capture investors’ attention and catch up. High-quality, dividend-growing companies historically tend to deliver good upside capture and defensiveness in uncertain periods, which could help investors weather the uncertainty of the next few months while benefitting from the equity rotation. The WisdomTree US Quality Dividend Growth UCITS ETF and WisdomTree Global Quality Dividend Growth UCITS ETF have both outperformed their market-cap-weighted benchmarks by 2.6% and 1.92%, respectively, as of 4 August 20242.

The Bank of Japan opens the door for a double hawkish surprise

The Bank of Japan (BOJ) not only presented a plan to reduce its bond purchases, as expected, but also somewhat surprisingly raised the key interest rate to 0.25% . On the same day, the US Federal Reserve (Fed) also prepared the path for the turnaround in interest rates. The narrowing of interest rate differentials between the US and Japan has been supported by the recent rally of the yen to the detriment of Japanese export-based equities. USD/JPY has corrected 10.8% off its highs4.

The BOJ has made a political decision to support the yen. This is evident as the Japanese economy’s growth in Q1 was weak and inflation has been falling. In such a scenario we would expect the BOJ to support the economy. By raising interest rates, the BOJ expects the economy to remain robust and inflation to remain high. However, if these expectations fail to materialise, the yen could reverse its recent appreciation compared to the US dollar.

The WisdomTree Japan Equity UCITS ETF has posted a strong start to the year on the back of strong earnings, corporate governance reforms, and its tilt toward dividend-paying export-oriented Japanese stocks. Though domestic fundamentals haven’t changed much since a few weeks ago, Japan’s equity market is unlikely to meaningfully reverse until the US market calms. Global investors see the Japanese market as a warrant on global trade. So, as markets are in de-risking mode over US recession fears and geopolitics, investors are taking profits from a market that has done well this year.

Fundamentally, large cap Japanese export stocks remain in pole position. The current company forex assumption is a conservative ¥144 per dollar, expecting a stronger yen. The yen’s fall from April to June 2024 (average of ¥156 per dollar) served as a reserve. The yen would need to average ¥140 per dollar over the last three quarters of the fiscal year to align with the corporate assumption for FY24. Given the current pace of appreciation of the yen, we don’t expect companies to have to lower their guidance.

Value stocks drove strong returns across emerging markets (EM) and have continued to outperform growth since 1990. The Fed's sharp re-pricing of monetary easing, alongside resilient economic growth in EM and supply chain rebalancing, is expected to support EM equities. The WisdomTree Emerging Markets Equity Income UCITS ETF is positioned towards dividend-paying EM equities poised to benefit from growth outside China with an overweight in Taiwan, Brazil and South Africa and an underweight in China5.

Semiconductors played a pivotal role in the tech sector correction. Despite many semiconductor companies, including AMD, Qualcomm, and TSMC, exceeding guidance and estimates in their recent earnings season, the market expressed concerns about the sustainability of their growth and US export restrictions on chips to China. Intel’s sales missed guidance, erasing around one-third of its market cap within two days from 31 July to 2 August. Mid and small cap tech sectors, which initially benefited from the anticipation of rate cuts in early July, were also pulled down by the general trend of the tech sectors. This pessimism across the tech sectors led to a downturn in tech-focused ETFs like WisdomTree Artificial Intelligence UCITS ETF, WisdomTree Cybersecurity UCITS ETF, and WisdomTree Cloud Computing UCITS ETF.

EM equities also declined during the recent correction from 31 July to 2 August, however they fell less compared to the developed markets. The MSCI ACWI declined by 3.31%, while the MSCI Emerging Market index declined by 2.17%. This generally helped themes with relatively higher exposure to emerging markets, such as WisdomTree Recycling Decarbonisation UCITS ETF, WisdomTree Energy Transition Metals and Rare Earths Miners UCITS ETF, WisdomTree Battery Solutions UCITS ETF and WisdomTree Renewable Energy UCITS ETF, to lose less than those tech themes. For instance, the China exposure of WisdomTree Battery Solutions UCITS ETF, representing around 22% of its weight, posted a -2.15% return from 31 July to 2 August, while US and Western Europe holdings posted returns of -10.0% and -5.0%, respectively, during the same period.

Source: Bloomberg. As of 2 August 2024. You cannot invest directly in an index. Historical performance is not an indication of future performance, and any investments may go down in value.

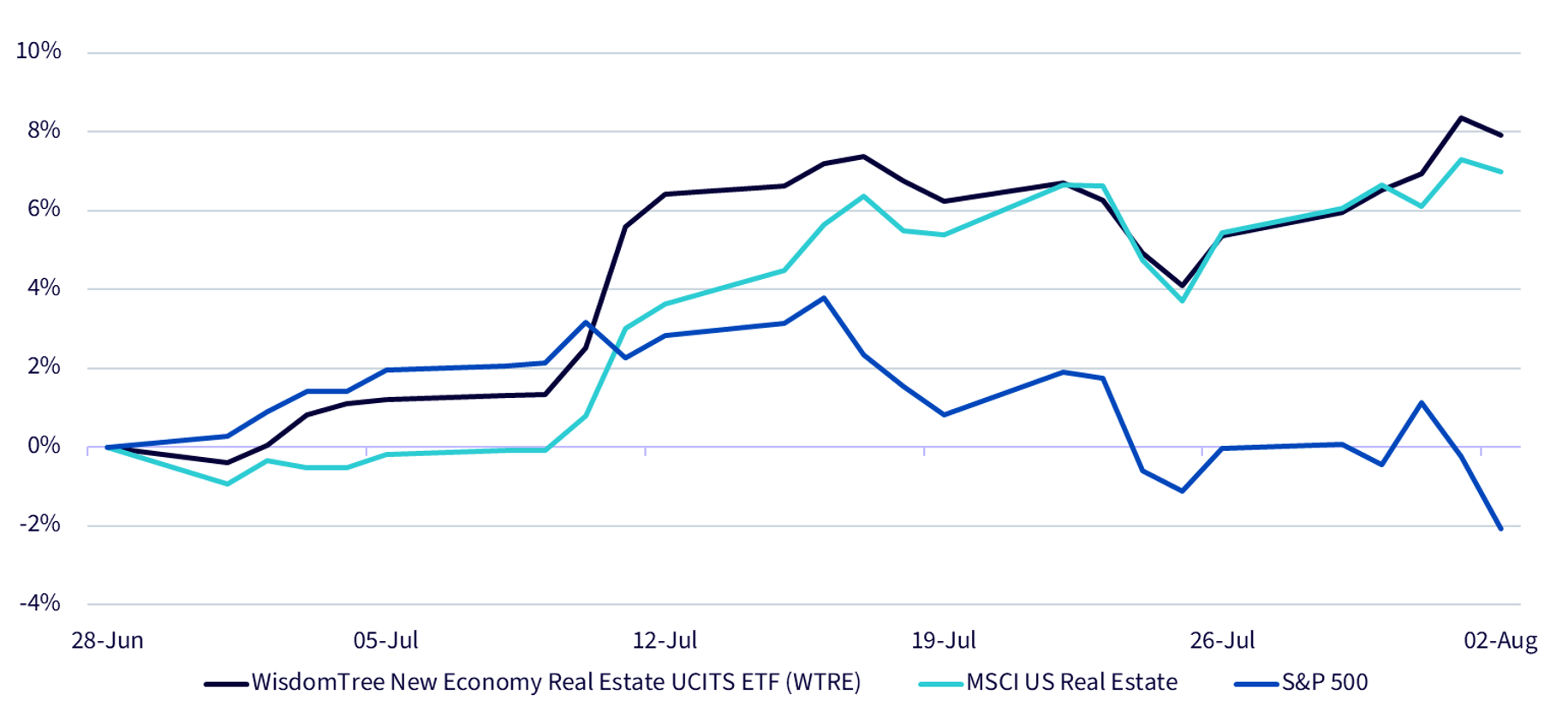

Real estate themes exhibit resilience amid market decline

There was also a segment that was exempt from the declining market. The real estate sectors performed well from 31 July to 2 August, with the MSCI US real estate index rising 0.84% and a 6.99% return from 28 June to 2 August. WisdomTree New Economy Real Estate UCITS ETF, which focuses on real estate companies with exposure to technology, science, and/or e-commerce-related business activities, returned 0.91% against the general correction from 31 July to 2 August and posted a 7.91% return since 28 June. Specialised real estate investment trust (REIT) holdings, accounting for around 25% of weight, posted a 3.9% return. With the anticipation of rate cuts and high market volatility (the VIX index reached 48.1 on 5 August, the highest level since early 2020), real estate could become increasingly attractive for investors seeking more stable investments.

Source: Bloomberg. As of 2 August 2024. WTRE’s performance is based on the fund’s NAV in USD. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

Source

1 Magnificent Seven is a group of mega cap stocks, including Apple, Alphabet, Microsoft, Amazon.com, Meta Platforms, Tesla, and Nvidia.

2 Bloomberg from 10 July to 4 August 2024. In USD. All indices are net TR.

3 Bank of Japan as of 31 July 2024

4 Bloomberg from 10 July to 5 August 2024

5 WisdomTree, Factset weighting versus MSCI Emerging Markets Index

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.

Senior Associate, Quantitative Research and Multi Asset Solutions

Baoqi Zhu joined WisdomTree in 2023 as a Senior Associate on the Research team. Baoqi focuses on quantitative research on thematic equity indices and portfolio solutions. Prior to WisdomTree, Baoqi spent over two years at Ernst & Young (EY) in their Quantitative Advisory Services, where he was involved in the research and development of quantitative risk models. Earlier in his career, Baoqi served as a quantitative analyst within a multi-asset structuring team at Maven Global for more than three years. His responsibilities included designing and optimising bespoke hedging strategies based on derivatives. Baoqi holds a MSc in Financial Engineering & Risk Management from Imperial College London and a BSc in Actuarial Science from Nankai University, China. He is also a certified Financial Risk Manager (FRM).