PHPM LN

WisdomTree Physical Precious Metals

Publié le 8 janvier 2026

The best performers this year are not simply those aided by cyclical catalysts; they are the beneficiaries of major structural shifts that could sustain performance for years to come.

On what is known as ‘Liberation Day’ (April 2, 2025), US tariffs surged to their highest levels in nearly a century. In parallel, the Trump administration signalled a strategic re-prioritisation of foreign policy, scaling back US security commitments to Europe. Many expected such shocks to trigger an economic contraction as supply chains adjusted, alongside financial-market turbulence as companies digested higher import costs. Yet the S&P 500 is up 17.5% year-to-date (YTD)1, and there is no sign of recession in any major economy. While the cyclical backdrop remains firm, the events of 2025 have reshaped several sectors, propelling them to new highs.

Fund | Ticker | YTD Performance |

|---|---|---|

PHPM | 88% | |

RARE | 114% | |

NCLR | 103%* | |

DXJZ | 29% | |

WDEF | 16%* |

Source: WisdomTree, Bloomberg. 31/12/2024 to 31/12/2025 for all funds except NCLR and WDEF. *12/03/2025 to 31/12/2025 for NCLR and WDEF (i.e. after inception dates of the funds). Historical performance is not an indication of future performance and any investments may go down in value.

Precious metals have excelled in 2025. Gold, up 67% year-to-date (YTD), initially led the rally before being overtaken by other metals. The Liberation Day shock sent investors seeking defensive assets, and gold benefitted as the Economic Policy Uncertainty Index2 surged to record highs. Yet trade uncertainty was only one driver. President Trump’s public criticism of the Federal Reserve (Fed) Chair and Governor Cook, the removal of the Head of the Bureau of Labor Statistics (BLS), and hints of a politically aligned successor all unsettled markets. Rising and potentially unsustainable government debts in the United States and Europe have also heightened concerns about fiscal dominance, where fiscal needs constrain monetary policy and raise the risk of currency debasement. Central banks, wary of these dynamics and of potential fiat currency ‘weaponisation’, have been major buyers, further supporting prices.

Silver, up 164% YTD, has gained from its high correlation with gold and a persistent supply deficit. Its inclusion on the US Geological Survey’s Critical Minerals list in November 2025 has tightened non-US inventories as traders shifted metal into the United States ahead of possible tariffs.

Platinum and palladium, up 147% and 92% YTD respectively, remain supported by structural supply deficits and resilient demand from internal combustion engine and hybrid vehicles. These underlying forces suggest precious-metal strength could extend into 2026.

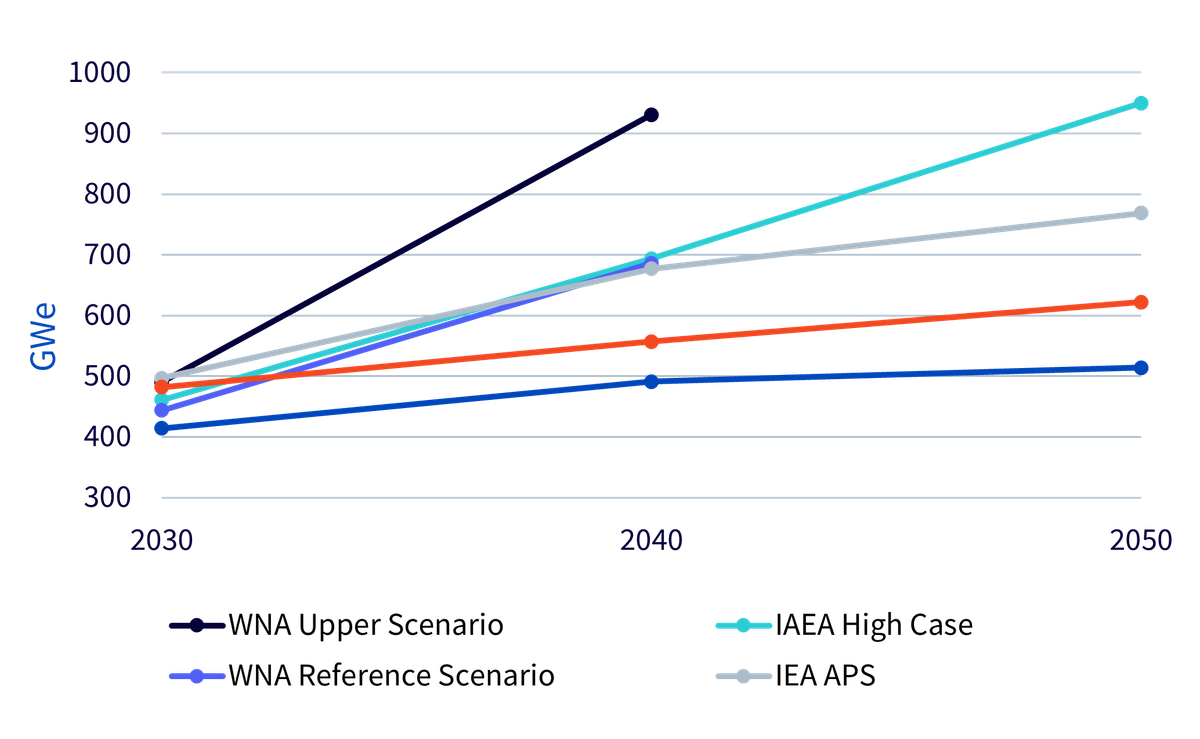

In November, the Swedish government announced it was lifting its ban on uranium mining that had been in effect since 2018. Sweden is believed to possess 27% of Europe’s known uranium reserves3, making this decision not just economically consequential for the country, but meaningful for the global supply of this very powerful rock. Sweden has also, like many other countries, announced its decision to invest in small modular reactors.

Sweden is worth highlighting because it is not just countries like the US and China that are turning to nuclear to power technologies like artificial intelligence (AI). Many countries around the world are rekindling their interest in nuclear energy in the face of rapidly rising energy needs. Tech companies building power-hungry data centres are striking long-term deals to secure nuclear energy. Most forecasts, see figure below, point to rapid global expansion of nuclear energy in the years ahead.

The WisdomTree Uranium and Nuclear Energy UCITS ETF, a strong performer in 2025, provides investors with thoughtful exposure across the value chain that stands to benefit from the nuclear energy renaissance. This includes upstream miners of uranium, midstream companies serving the nuclear industry, and innovators developing advanced technologies like small modular reactors.

Source: World Nuclear Association, December 2025, IAEA and World Nuclear Association scenario figures are net electrical capacity. IEA scenario figures are gross electrical capacity. IAEA is International Atomic Energy Agency, IEA is the International Energy Agency. The Stated Policies Scenario (STEPS) aims to describe the prevailing direction of the energy system, based on a sector-by-sector and country-by-country assessment of energy-related policies that are in place and under development. The Announced Pledges Scenario (APS) assumes that all climate commitments made by governments and industries around the world will be met in full and on time. Gigawatt-electric (GWe). Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

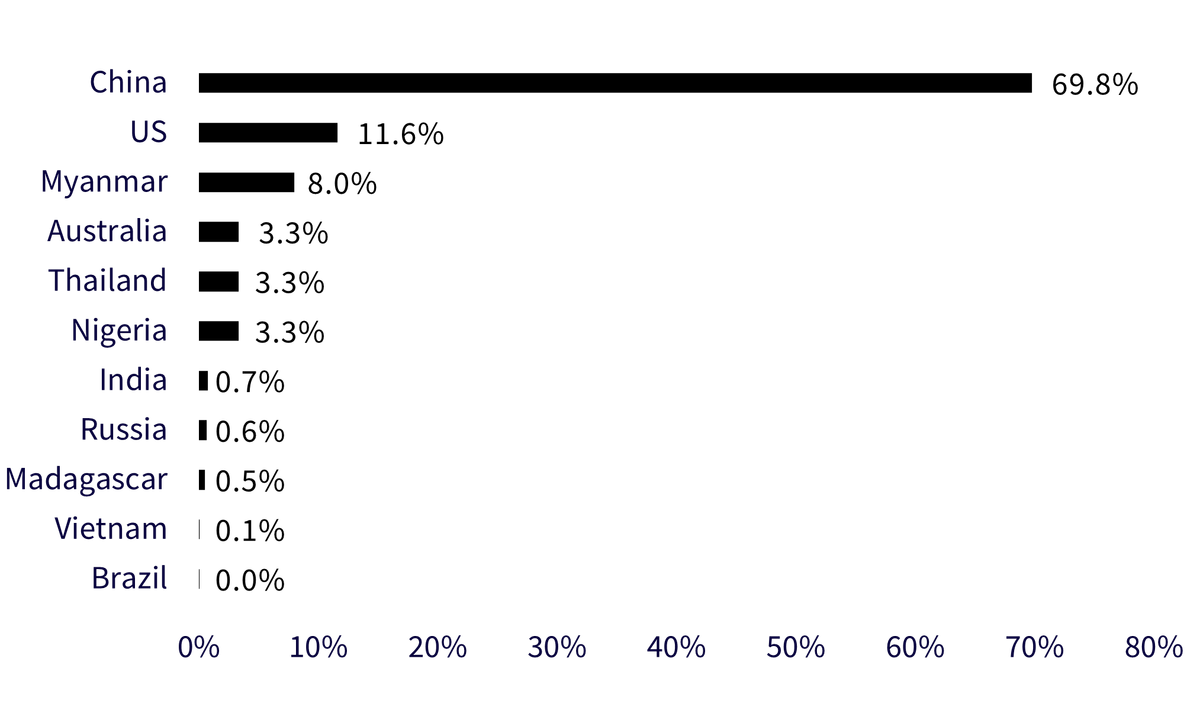

In November, MP Materials struck a major three-way deal with the US Department of Defence and Saudi miner Maaden to build a rare earth processing plant in Saudi Arabia. The US and MP will hold up to 49% of the venture, with Maaden owning at least 51%4. The agreement is strategically important because it creates a non-Chinese supply chain for critical rare earths, supporting defence, energy, and technology industries in both countries.

This development signifies how the US is looking to contend with China’s dominance in rare earths, which are essential for technologies across virtually every modern industry. This includes AI hardware, electric vehicles, consumer electronics, renewable energy systems, and advanced defence equipment. China produces around 70% of the world’s rare earths (see figure below) and processes around 90%. Building new supply chains will take time and any disruption in supply could cause prices to rise. Meanwhile, rapidly rising demand for these materials in new technologies will keep the market focus high.

The WisdomTree Strategic Metals and Rare Earths Miners UCITS ETF, another strong performer in 2025, provides investors access to ten different strategic metals including rare earths, with companies selected by industry experts Wood Mackenzie across the respective value chains of each metal.

Source: Statista, February 2025. Historical performance is not an indication of future performance and any investments may go down in value.

European defence captivated investors in 2025 as the theme shifted from headlines to hard orders and delivered strong equity market performance, up 80.2%5. Three forces did the heavy lifting. First, policy clarity. The North Atlantic Treaty Organisation (NATO) set higher targets for defence and security spending set a durable glide path, while the EU’s financing tools and national budgets made it actionable, as discussed here. Most notably, Germany loosened its debt brake, exempting defence and security outlays above roughly 1% of GDP. That decision was transmitted into procurement plans, advance payments and multi-year framework contracts.

Second, operating momentum. Across defence primes the average backlog to monthly sales ratio remained robust.

Source: WisdomTree, Bloomberg. For each holding, backlog to monthly sales ratio calculated as Order Backlog Value / (Trailing 12M Net Sales/12). Data as of 21 November 2025. All holdings in the WisdomTree Europe Defence UCITS Index with available data are included in the calculation. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

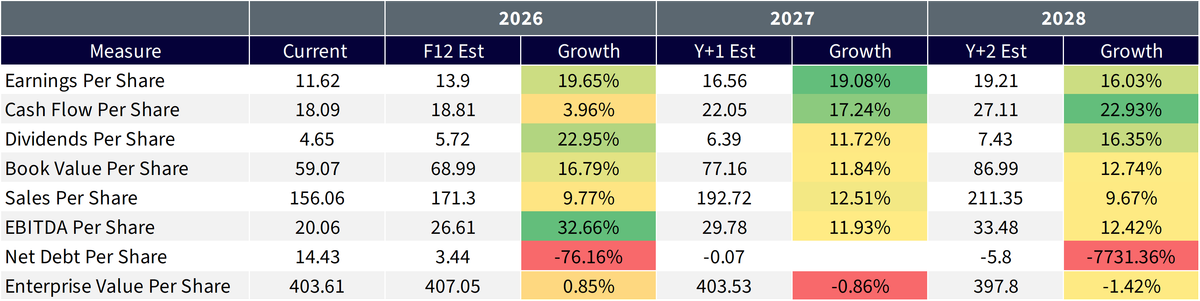

Third, expected long term growth in earnings. The WisdomTree Europe Defence UCITS Index is positioned for strong earnings growth, with earnings per share expected to rise by 19.65% in 2026 and 19.08% in 20276. This reflects expanding market share, multi-year procurement cycles, and increasing defence budgets across Europe. While cash flow per share is expected to increase as companies scale operations, debt levels are projected to decline, ensuring financial stability.

Source: Bloomberg, WisdomTree as of 31 December 2025. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Japan stood out in 2025 as cyclical improvement met structural change. The Tokyo Stock Exchange’s governance drive prompted companies to utilise excess cash, enhance their return on equity, and address low price-to-book valuations. Political developments added further support. Sanae Takaichi’s election victory pointed to targeted fiscal expansion, particularly in strategic areas such as semiconductors, energy security and defence. These priorities supported domestic demand while remaining consistent with a commitment to fiscal discipline. Trade-related uncertainty also eased. The introduction of a 15% tariff ceiling, alongside ongoing efforts by exporters to localise production, improved visibility and planning across global supply chains.

Monetary policy is expected to shift from supportive to moderately restrictive. The Bank of Japan (BOJ) has prepared the ground to raise rates again, while emphasising a gradual pace that keeps financial conditions accommodative. A careful path higher for the policy rate can anchor inflation expectations, support corporate earnings and still leave the yen contained enough to favour exporters' margins and translation.

The outlook remains optimistic. Governance reforms are raising the quality of earnings, expected stimulus should support consumption and a moderate yen supports global manufacturers. With lower trade risk and a measured BOJ path, Japanese equities enter 2026 positioned for broader earnings growth across exporters and domestic companies as real wages improve.

1 All YTD performance in this note are from 31/12/2024 to 30/12/2025 and taken from Bloomberg

2 Baker, Bloom and David designed index

3 The Geological Survey of Sweden, 2025

4 Financial Times, November 2025

5 Bloomberg, Performance of the WisdomTree Europe Defence UCITS Index from 31 December 2024 to 31 December 2025

6 Bloomberg, WisdomTree as of 31 December 2025

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.

Director, Research

@MobeenTahirWTMobeen is a member of WisdomTree’s research team where he focuses on a wide range of asset classes to offer strategic and tactical insights to our clients on global markets and investment products. Before joining WisdomTree in December 2018, Mobeen worked at Willis Towers Watson as an investment consultant advising institutional clients as well as their in-house fund business on asset allocation and portfolio construction with his research focus being equity and multi-asset smart beta. Mobeen has a BSc (Hons) in Accounting and Financial Management from Loughborough University and an MSc in Accounting and Finance from the London School of Economics and Political Science. He is also a CFA Charterholder.

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.