WSPC

Space Economy Fund

Published July 9, 2026

Global Head of Research

For most of the modern era, space was something governments funded and engineers dreamed about. It produced extraordinary science, essential navigation infrastructure, and military capabilities, but it was not, in any meaningful commercial sense, an economy. The assets were too expensive, the access too rare, and the applications too narrow to attract the kind of sustained private capital that defines a real market.

That model has now changed in ways that are both measurable and, in some respects, still underappreciated. The global space economy reached approximately $613 billion in 2024, according to the Space Foundation, representing 7.8% year-over-year growth.1 Commercial activity, led by satellite services and broadband, now accounts for roughly 78% of that total, up from approximately 60% a decade ago.2 In 2025, orbital launch attempts exceeded 329 worldwide, more than double the pace of five years earlier.3 A satellite was reaching orbit, on average, every 28 hours in the first half of 2025, and this was six hours faster than the record pace set in 2024.4

Those numbers describe a sector in transition, but we think that the more useful frame is not the size of the market today, but rather the structural shift that made these numbers possible, as well as what it implies for how investors should think about the opportunities ahead.

That is the backdrop for the newly launched WisdomTree Space Economy Fund (WSPC), which provides targeted exposure to companies participating across the space economy value chain, including launch infrastructure, satellite data and connectivity, defense space systems, and emerging orbital technologies.

The Cost Revolution That Changed Everything

The enabling condition for the commercial space economy is a cost collapse that has no clean historical parallel. For most of the space age, delivering one kilogram of payload to low Earth orbit cost somewhere between $10,000 and $65,000 depending on the vehicle. That price range made space viable for governments and a narrow set of high-value telecommunications satellites, but it was prohibitive for nearly everything else.

Reusable launch vehicles changed that arithmetic. SpaceX's Falcon 9 reduced per-kilogram costs to roughly $2,700. The broader implication of full reusability, which is the stated goal of Starship, is a cost target below $200 per kilogram over the long run, a reduction of more than 95% compared to the expendable vehicles that dominated the market a decade ago.5

The consequences cascade through the entire value chain. Think about, for instance, internet access and uses of satellites:

SpaceX illustrates the scale of what this unlocks. The company completed 165 Falcon 9 and Heavy missions in 2025, accounting for more than half of global orbital launches by count and approximately 65% of mass delivered to orbit.6 Its Starlink broadband constellation crossed 10,000 active satellites and generated an estimated $11.4 billion in revenue during 2025, with projections approaching $20 billion in 2026.7 Starship, still in its development phase with 12 flights completed as of late May 2026, is targeting payload delivery to orbit in the second half of 2026, a milestone that, if achieved, would represent the entry of the world's most capable rocket into commercial service.8

The Launch Ecosystem Beyond SpaceX

The commercial space economy is not a single-company story. The emergence of a genuine multi-provider launch ecosystem is itself a structural development worth understanding, because it implies supply chain resilience, competitive pricing pressure, and the development of differentiated capabilities across vehicle classes.

Rocket Lab is the clearest example of what a scaled small-lift operator looks like. The company flew 21 Electron missions in 2025 with a 100% success rate, generating full-year revenue of $602 million, 38% growth year-over-year, and ending the year with a backlog of $1.85 billion.9 The backlog figure is particularly notable, and 37% of it is expected to convert within 12 months, representing approximately $685 million in locked-in revenue before a single new contract is signed.10 Rocket Lab's largest single contract to date, which was an $816 million award from the Space Development Agency for 18 satellites in the Tracking Layer Tranche 3 program, signals that it has crossed a threshold from launch subcontractor to national security prime.11

In Q1 2026, Rocket Lab posted record quarterly revenue of $200 million and reported that it had signed more new launch contracts in that single quarter than in all of 2025 combined, with a total launch manifest exceeding 70 contracted missions.12 Its Neutron medium-lift vehicle, targeting a first launch in Q4 2026, is designed to serve the constellation deployment and national security missions that sit between Electron's small-lift capacity and Falcon's heavy payload class.13

Firefly Aerospace, which successfully landed its Blue Ghost spacecraft on the lunar surface in early 2025, the first commercial lunar landing under NASA's CLPS program, is guiding full-year 2026 revenue of $420 to $450 million and is deepening its defense positioning across the Missile Defense Agency's SHIELD program.14 The fact that a company operating at that revenue scale is simultaneously a launch provider, a lunar lander operator, and a defense systems supplier illustrates how the boundaries between space sector categories are blurring.

The Data Layer: From Access to Intelligence

If launch is the access layer of the space economy, the data and connectivity layer is where a growing share of commercial value is being created. The proliferation of orbital assets is generating persistent, high-value data streams, and the question for investors is which business models can consistently convert that data into revenue.

Earth observation is the clearest example of this dynamic. Planet Labs operates a constellation of approximately 200 satellites, imaging the entire land surface of Earth every single day. That temporal frequency, daily global coverage, creates something no prior remote sensing system could offer:

A continuous, machine-readable record of how the planet's surface changes over time.15

The company reported full-year revenue of $307.7 million for its fiscal year 2026, representing 26% year-over-year growth and, for the first time, annual adjusted EBITDA profitability of $15.5 million and positive free cash flow of $52.9 million. Backlog reached $900 million by March 2026.16

The shift in Planet's revenue composition is as significant as the headline numbers. Defense and intelligence revenue grew more than 70% year-over-year in one recent quarter, with contracts spanning the National Geospatial-Intelligence Agency, the National Reconnaissance Office, the U.S. Navy, and NATO.17 Planet's next-generation Pelican satellites feature on-orbit AI processing via NVIDIA chips, enabling the satellite itself to identify a specific target, which could mean a vessel, a vehicle, or a structural change, and transmit the processed result rather than the raw image.18 That shift from data provider to intelligence provider is the margin-expansion story embedded in the subscription model.

Satellite broadband represents a parallel data-layer opportunity with a different scale of addressable market. AST SpaceMobile is building what it describes as the first space-based cellular broadband network designed to work with unmodified smartphones, no specialized terminal hardware required.19

BlueBird 6, launched in December 2025, was the largest commercial communications phased array ever deployed in low Earth orbit, designed to deliver peak data rates exceeding 120 Mbps directly to standard devices.14 The company is targeting 45 satellites in orbit by the end of 2026, with launches approximately every one to two months on average, supported by partnerships with AT&T, T-Mobile, Verizon, and Vodafone among others.15 Over $1.2 billion in aggregate contracted revenue commitments have been secured from partner mobile network operators and the U.S. Government.20

Defense and Sovereignty: The Structural Floor

The commercial narrative tends to attract most of the investment media attention, but defense and sovereignty demand represents a structurally important and often underappreciated driver of the space economy. Every major military power has formally designated space as a warfighting domain. That designation translates into procurement that is largely independent of commercial market sentiment.

U.S. government space spending reached approximately $77 billion in 2024, with combined military and intelligence space budgets exceeding $29 billion focused on missile warning, GPS resilience, secure satellite communications, and space domain awareness.21 The U.S. Space Force's procurement through Other Transaction Authority agreements, bypassing traditional defense acquisition bureaucracy, has created a new and expanding government customer whose programmatic flexibility has specifically enabled the rise of dual-use commercial space companies as national security suppliers.

That dynamic is not limited to the United States. The Space Foundation's data shows government space spending grew 6.7% in 2024 globally,22 with allied nations accelerating investment in indigenous space capabilities. Airbus Defence and Space reported 11% revenue growth to $14.5 billion in 2025; Leonardo's Space division grew 11% to $1.08 billion over the same period.23 Japan, South Korea, France, and Germany are each investing in sovereign launch capabilities, satellite manufacturing, and space situational awareness systems, a geographic broadening of the demand base that is less visible in headline market size figures but important for the long-duration investment thesis.

The Next Chapter

The space economy is at an inflection point that shares structural characteristics with earlier technology transitions, the commercialization of the internet, the proliferation of mobile broadband, while remaining genuinely distinct in its physical constraints and capital intensity.

The Space Foundation projects the global space economy could cross the $1 trillion threshold as early as 2032.24 That forecast is built on the compounding of launch cost reduction, satellite constellation scale, and AI-enabled data monetization into a set of markets that are only beginning to attract the kind of recurring, subscription-based revenue that supports durable equity valuation.

The investment opportunity is not a single bet on a single company or technology. It is an attempt to own the access layer, which is to say the vehicles and infrastructure that make the rest possible, alongside the data layer where commercial value is accumulating, and the defense layer that provides structural demand independent of commercial cycles. Those three layers are interdependent: access enables data, data enables defense applications, defense spending subsidizes infrastructure development, and the cycle compounds.

The space economy is not a future technology story. It is a current infrastructure buildout with measurable revenue, growing backlogs, and compounding applications. The question for investors is not whether this transition is happening. It is whether their portfolios are positioned to benefit from it.

Introducing the WisdomTree Space Economy Fund

The WisdomTree Space Economy Fund (WSPC) provides investors with targeted exposure to this transition by capturing companies across the full space economy value chain, from launch vehicles and spacecraft infrastructure to satellite data services, connectivity, and defense space systems.

The strategy is organized around four primary thematic layers, each representing a distinct segment of the space economy's value chain:

These categories together represent the transition from space as a government program to space as a multi-layer commercial economy, one in which the access layer, the data layer, the security layer, and the frontier layer are compounding simultaneously and often interdependently.

It is an important moment to introduce a focused space economy exposure to the market. The cost revolution in launch has already happened. The data monetization models are proving themselves. The defense procurement cycle is accelerating. The question now is which investors are positioned to benefit from the buildout that follows.

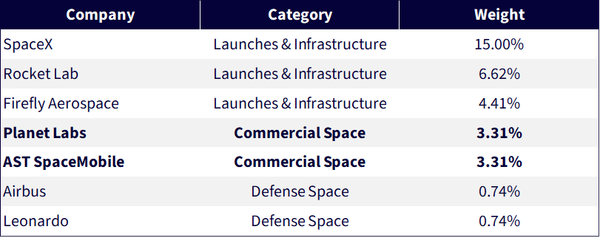

Figure 1: Table of Companies and Strategy Weights

Source: WisdomTree. Weights represent the targeted weights as of the launch of the WisdomTree Space Economy Fund. Holdings subject to change.

1 Source: Space Foundation. (2025, July 22). The Space Report 2025 Q2 Highlights Record $613 Billion Global Space Economy for 2024. Space Foundation.

2 Source: Orbital Radar. (2026). The Global Space Economy 2026: $626B Market Size, Live Data & $1T Forecast.

3 Source: Sci-Tech Today. (2026). Commercial Space Industry Statistics by Market Size and Country.

4 Source: Space Foundation. (2025, July 22).

5 Source: New Market Pitch. (2026, January 12). Space Economy Market Size 2026.

6 Source: Sci-Tech Today. (2026).

7 Source: Sci-Tech Today. (2026).

8 Sources: Wikipedia. (2026, May 27). List of Starship Launches; Berger, E. (2026, May 21). Starship underpins SpaceX's growth ambitions. SpaceNews.

9 Source: Rocket Lab USA, Inc. (2026, February 26). Rocket Lab Announces Fourth Quarter and Full Year 2025 Financial Results. [Press release.]

10 Source: Cyclops Space Tech. (2026, February 27). Rocket Lab Q4 2025 Earnings: The Tank Failed, the Timeline Slipped and the Stock Shrugged.

11 Source: Rocket Lab USA, Inc. (2026, February 26).

12 Source: Rocket Lab USA, Inc. (2026, May 7). Rocket Lab Announces First Quarter 2026 Financial Results. [Press release.]

13 Source: Rocket Lab USA, Inc. (2026, February 26).

14 Source: Firefly Aerospace Inc. (2026). Form 8-K, FY2026. [Press release.] U.S. Securities and Exchange Commission.

15 Source: Planet Labs PBC Investor Relations. (2026). Overview.

16 Source: Anand Capital. (2026, March 23). Planet Labs PBC (PL) Investment Thesis.

17 Source: Planet Labs PBC Investor Relations. (2026). Overview.

18 Source: FinancialContent/Finterra. (2026, March 20). The Bloomberg of Earth Data: A 2026 Deep Dive into Planet Labs.

19 Source: AST SpaceMobile, Inc. (2026, March 2). AST SpaceMobile Provides Business Update and Fourth Quarter and Full Year 2025 Results. [Press release.] U.S. Securities and Exchange Commission.

20 Source: AST SpaceMobile, Inc. (2026, March 2).

21 Source: SpaceNexus. (2026). Space Industry Statistics & Facts 2026.

22 Source: Space Foundation. (2025, July 22).

23 Source: Global Market Insights. (2026). Space Economy Market Report.

24 Source: Space Foundation. (2025, July 22).

The Fund concentrates its investments in the Capital Goods international markets.

There are risks associated with investing, including possible loss of principal. The Fund invests primarily in equity securities that provide exposure to global companies involved in activities that form the space economy (“Space Economy Companies”), which are subject to significant technological complexity, high capital requirements, extended development cycles, and uncertainty regarding the commercial adoption of space-based products and services. These companies face intense competition, rapid technological change, and evolving domestic and international regulatory requirements, which may adversely affect their operations and financial performance. The Fund’s exposure to certain sectors may increase its vulnerability to any single economic or regulatory development related to such sector. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers.

The Fund concentrates its investments in the Capital Goods and Technology Hardware & Equipment groups of industries and expects to have significant exposure to the Industrials, Information Technology, and Communication Services sectors, making it more susceptible to developments affecting those industries and sectors.

Investments in non-U.S. securities involve political, regulatory, and economic risks that may not be present in U.S. securities. For example, foreign securities may be subject to risk of loss due to foreign currency fluctuations, political or economic instability, or geographic events that adversely impact issuers of foreign securities. Investments in securities and instruments traded in developing or emerging markets, or that provide exposure to such securities or markets, can involve additional risks relating to political, economic, or regulatory conditions not associated with investments in U.S. securities and instruments or investments in more developed international markets

While the Fund is actively managed, the Fund's investment process is heavily dependent on quantitative models, including artificial intelligence-based models, and the models may not perform as intended.

Please read the Fund's prospectus for specific details regarding the Fund's risk profile.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.