WQTM

Quantum Computing Fund

Published July 8, 2026

Global Head of Research

Macro Strategist, Model Portfolios

When NVIDIA announced Ising, a family of AI models designed specifically for quantum calibration and error decoding,1 it was easy to file the news under 'interesting research project.'

In our view, it deserves to be thought of as a strategic declaration.

The company that became the infrastructure layer of classical AI is methodically positioning itself as the infrastructure layer for quantum computing. That repositioning, more than any single qubit milestone, is what this piece is about.

In part 1 of this series, we explored how quantum computing could extend the so-called ‘AI trade’ in equities, adding new layers of demand to the component suppliers, cybersecurity vendors, cloud providers, and classical compute architects already benefiting from the AI buildout. That framing deliberately ran counter to the conventional narrative, which tends to ask how quantum might eventually help AI. This piece takes on that conventional question directly. But our answer, we think, is less conventional than it first appears.

The short version

AI is likely to help quantum computing sooner, and more concretely, than quantum computing will help AI. That asymmetry in timing is, itself, the investment insight.

NVIDIA's product roadmap, including Ising, NVQLink, and CUDA-Q, is a clear piece of evidence. It may be that sitting with the uncertainty rather than resolving it prematurely turns out to be the more intellectually honest, and also strategically useful, posture for investors trying to navigate both themes.

It is not immensely helpful to ask simply, 'will AI help quantum?' The more precise framework of questions could be:

NVIDIA, characteristically, is not waiting for the answer.

Why AI Helps Quantum First

Quantum computers are, at their core, extraordinarily fragile physical systems. Qubits lose coherence due to thermal fluctuations, electromagnetic interference, and the unavoidable disturbance introduced by measurement. Building a useful machine means fighting that fragility continuously. For example, by measuring errors, correcting them, recalibrating drifting hardware, and doing all of this faster than the errors accumulate. This is precisely the kind of high-dimensional, noisy, pattern-recognition problem where AI has demonstrated consistent practical value in other domains.

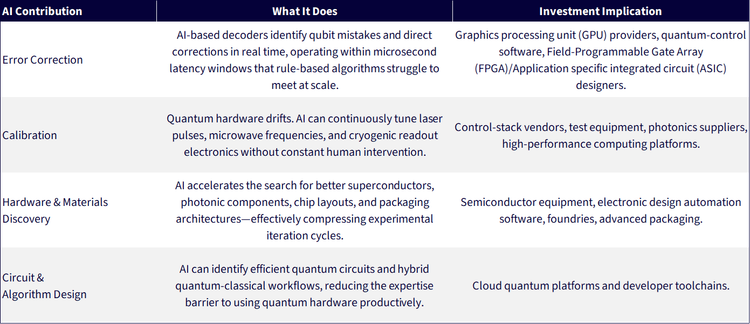

There are four concrete pathways through which AI is already contributing.

Figure 1: AI May Already Be Helping Quantum Computing

Sources: Bausch, J., Senior, A. W., Heras, F. J. H., Edlich, T., Davies, A., Newman, M., Jones, C., Satzinger, K., Niu, M. Y., Blackwell, S., et al. (2024). Learning high-accuracy error decoding for quantum processors. Nature, 636(8040); NVIDIA. (2026, April 14). NVIDIA launches Ising, the world's first open AI models to accelerate the path to useful quantum computers. NVIDIA Newsroom; Alexeev, Y., Farag, M. H., Patti, T. L., Wolf, M. E., Ares, N., Aspuru-Guzik, A., Benjamin, S. C., Cai, Z., Cao, S., Chamberland, C., Chandani, Z., Fedele, F., Hamamura, I., Harrigan, N., Kim, J.-S., Kyoseva, E., Lietz, J. G., Lubowe, T., McCaskey, A., Melko, R. G., Nakaji, K., Peruzzo, A., Rao, P., Schmitt, B., Stanwyck, S., Tubman, N. M., Wang, H., & Costa, T. (2025). Artificial intelligence for quantum computing. Nature Communications, 16, Article 10829.

These are not speculative projections.

Taken together, these products outline a GPU/QPU integration platform, effectively the same playbook NVIDIA ran with CUDA for classical AI, now being run for quantum.

The near-term thesis, then, is relatively direct: AI infrastructure, such as GPUs, control software, HPC interconnects, and cloud orchestration layers, becomes a required input for scaling quantum hardware. Investors already own much of this for AI reasons. Quantum adoption represents a second demand vector from the same underlying assets.

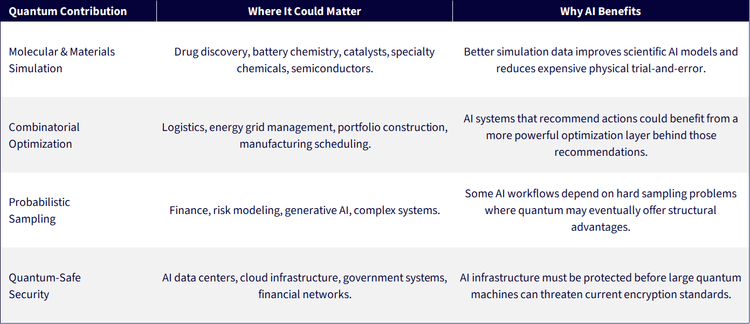

The Harder Question: How Quantum Might Eventually Help AI

The reverse leg, quantum improving AI, is where careful framing matters most. The temptation is to oversell a future that is technically plausible but practically distant. Quantum computers are not going to train the next generation of large language models more cheaply next year. The more defensible thesis is that quantum computing could eventually help AI applications in specific domains where the hard problem is physical simulation, combinatorial optimization, or high-dimensional probabilistic sampling, not general-purpose pattern recognition.

The strongest eventual use cases may cluster around a few areas.

Figure 2: Where Quantum Computing May Contribute to AI

Source: Alexeev, Y., Farag, M. H., Patti, T. L., Wolf, M. E., Ares, N., Aspuru-Guzik, A., Benjamin, S. C., Cai, Z., Cao, S., Chamberland, C., Chandani, Z., Fedele, F., Hamamura, I., Harrigan, N., Kim, J.-S., Kyoseva, E., Lietz, J. G., Lubowe, T., McCaskey, A., Melko, R. G., Nakaji, K., Peruzzo, A., Rao, P., Schmitt, B., Stanwyck, S., Tubman, N. M., Wang, H., & Costa, T. (2025). Artificial intelligence for quantum computing. Nature Communications, 16, Article 10829.

McKinsey's 2026 Quantum Technology Monitor projects that the internal quantum computing market—covering hardware, software and services—could reach $43 to $71 billion by 2035, with broader economic value creation potentially far exceeding that figure.2 These figures should be treated as directional rather than precise. Academic reviews of quantum machine learning remain cautious, and practical advantage is constrained today by hardware limitations, benchmarking challenges, and the difficulty of state preparation at scale. The honest framing is that quantum may not replace GPUs for general AI workloads, but could make specific AI-driven industrial workflows meaningfully more powerful.

A Framework for Living with Uncertainty

One of the most important things an investor can do in this space right now is resist the pressure to resolve the uncertainty prematurely. The architecture of useful quantum computers is not settled. The winning qubit modality, by which we mean superconducting, trapped ion, neutral atom, photonic, silicon spin, annealing or topological, is genuinely unknown. The U.S. Department of Commerce's recent $2 billion in proposed CHIPS Act incentives for quantum companies deliberately spans multiple approaches, which is itself a signal.3 The government does not know which architecture wins, and neither does the market.

What investors can do is build a framework for monitoring how the thesis evolves. Four concrete indicators could be worth monitoring:

The first indicator is logical qubit progress. Physical qubit counts make headlines, but useful quantum computing depends on error-corrected logical qubits. Google's Willow work is significant precisely because it demonstrated below-threshold error rates and improved logical performance as code distance increased,4 a necessary (though not sufficient) proof point.

The second is repeatable customer revenue: chemistry, materials, pharma, optimization, finance use cases where customers pay because quantum measurably improves their answer, not because they are running a proof of concept.

The third is AI-controlled quantum operations appearing in production environments, which would be evidence that the AI-to-quantum thesis is generating real engineering value, not just research papers.

The fourth, and most near-term, is post-quantum cryptography budget growth, b because PQC migration does not require a fault-tolerant quantum computer to exist; it is already commercially urgent.

The Risks Worth Taking Seriously

Two structural risks deserve direct acknowledgment.

There is also a market-structure risk that cuts across both themes. The best economic returns from quantum computing may ultimately accrue to the large cloud and chip platforms rather than to hardware startups, in the same way that the largest AI profits have so far concentrated at the infrastructure layer rather than being distributed across every model developer and application company. Quantum could become another chapter in a familiar story, where the infrastructure owners capture the value, and most of the platforms built on top of them are commoditized over time.

Putting Both Pieces Together

Read alongside part one of this series, a clearer picture emerges. The AI trade and the quantum trade are not parallel stories running on separate tracks. They are increasingly entangled, sharing supply chains, engineering talent, capital allocation logic and investment narratives.

The near-term expression of this entanglement is that AI infrastructure enables quantum development:

The medium-term expression is that quantum-specific demand, for cryogenic components, specialized photonics, FPGA-based control systems, and eventually purpose-built ASICs, adds incremental revenue to companies already embedded in the AI infrastructure trade.

The long-term expression, more speculative but worth monitoring, is that quantum computers become specialized accelerators for the subset of AI-adjacent problems, which may include molecular simulation, combinatorial optimization, and cryptography, where classical methods hit fundamental limits.

The investment implication is not 'buy quantum stocks.' It is to own the interface layer where AI infrastructure, high-performance computing, semiconductors, quantum control, error correction, and quantum-safe cybersecurity converge, and then to hold a small, disciplined, diversified option on the hardware layer that may define the next phase.

The uncertainty is real. The scenarios are genuinely multiple. But the mental model that treats these two themes as separate bets, each requiring a binary call on timing, is likely the wrong frame. The more durable approach is to recognize that the same infrastructure buildout that is already underway for AI also could lay the physical and commercial foundation for quantum, and that the companies best positioned for one are often, by design, best positioned for the other.

At WisdomTree, we have two strategies:

As of April 30, 2026, the holdings overlap between the two funds was 23%, making, in our opinion, a strong argument for complementarity. If the goal of society is ever stronger computation per unit of power, both strategies include companies that attack this question quite differently.

1 Source: NVIDIA. (2026, April 14). NVIDIA launches Ising, the world's first open AI models to accelerate the path to useful quantum computers. NVIDIA Newsroom.

2 Source: McKinsey & Company. (2026, April). McKinsey quantum technology monitor 2026: A commercial tipping point.

3 Source: National Institute of Standards and Technology. (2026, May 21). Department of Commerce announces letters of intent with 9 companies for $2 billion to accelerate U.S. leadership in quantum computing [Press release]. U.S. Department of Commerce.

4 Source: Neven, H. (2024, December 9). Meet Willow, our state-of-the-art quantum chip [Blog post]. Google.

There are risks associated with investing, including potential loss of principal. Please read the Fund's prospectus for specific details regarding the Fund's risk profile.

WTAI: The Fund invests in companies primarily involved in the investment theme of Artificial Intelligence (AI) and Innovation. Companies engaged in AI typically face intense competition and potentially rapid product obsolescence. These companies are also heavily dependent on intellectual property rights and may be adversely affected by loss or impairment of those rights. Additionally, AI companies typically invest significant amounts of spending on research and development, and there is no guarantee that the products or services produced by these companies will be successful. Companies that are capitalizing on Innovation and developing technologies to displace older technologies or create new markets may not be successful. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended.

WQTM: To the extent the Fund invests a significant portion of its assets in the securities of companies of a single country or region, it is more likely to be impacted by events or conditions affecting that country or region. The economic, political, regulatory, and other events and conditions that affect issuers and investments in the United States differ significantly from those associated with other countries and regions. U.S. financial markets have become increasingly globalized becoming more integrated with financial markets around the world and as a result, U.S. financial markets are increasingly vulnerable to the risks that may affect non-U.S. financial markets. The Fund’s investments in the U.S. are subject to the risk that they, and the U.S. economy more generally, will be adversely affected by a decrease in imports or exports, changes in trade regulations, inflation, and/or an economic recession in the U.S. The Fund invests primarily in the securities of quantum computing companies. Companies engaged in the development of quantum computing or machine learning technology may be significantly impacted by rapid technological advancements, product obsolescence, intense competition, consumer demand, and government regulation. Such companies are also heavily dependent upon patent and intellectual property rights. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.