WDEF

Europe Defense Fund

Published August 18, 2025

Global Head of Research

Macro Strategist, Model Portfolios

If you're a U.S. investor, there's a good chance you've never heard of Rheinmetall. That's not a knock—it's a feature of the defense industry's regional segmentation. While American names like Lockheed Martin and General Dynamics dominate the Pentagon budget, Europe has its own giants. And Rheinmetall, headquartered in Düsseldorf, is arguably the most consequential player in Germany's defense-industrial complex. It designs and manufactures armored vehicles, artillery shells, loitering munitions, air defense systems and, increasingly, digital battlefield technology.

But beyond its catalog of capabilities, Rheinmetall has become something more: a proxy for Europe's rearmament. Since Russia's full-scale invasion of Ukraine in 2022, the company has positioned itself as the premier supplier of the systems and munitions required for a credible European deterrent. It's not just that Rheinmetall builds tanks. It's that Europe is rebuilding its military backbone—and Rheinmetall is the one holding the wrench.1

The company's strategic relevance is underpinned by the brute math of procurement. In many categories—Leopard tanks, Puma and Boxer infantry vehicles, 155-mm artillery shells—Rheinmetall is the only game in town. It has production monopolies or duopolies in core categories, vertically integrated supply chains and, increasingly, the political capital to influence how European governments allocate defense budgets. For investors, it represents something rare in European equities: a multi-year, government-backed growth story with expanding margins and asymmetric optionality.2

That's what makes last week's earnings reaction so intriguing. On August 7, 2025, Rheinmetall reported its second-quarter results and promptly saw its shares drop more than 6% in trading.3 The headlines cited a revenue miss and a lack of upward guidance revision. And yes—sales came in at €2.43 billion, about 4% below consensus, and the company chose to keep its full-year outlook unchanged despite a surge in order activity and ongoing political tailwinds.4

But the market's disappointment missed the forest for the trees. The earnings call revealed that much of the shortfall was tied to one-off delays: a €300 million truck delivery contract that slipped from Q2 into Q3, a temporary certification bottleneck for ammunition in Spain and the still-settling dynamics of Germany's newly formed government.5 These are not indicators of a demand slowdown. They're the artifacts of a rapidly scaling industrial platform trying to coordinate with governments that are still catching up to their own ambitions.

The key insight is this: Rheinmetall didn't lose business. It simply wasn't able to recognize it—yet. Management made it clear that most of the delayed deliveries are already built, sitting in inventory, and will ship in Q3 and Q4.6 That's not a revenue problem. It's a timing problem. And it sets the stage for a potentially massive back half of the year.

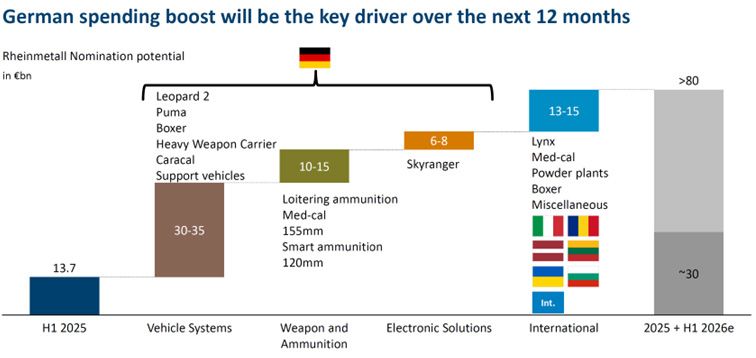

Let's talk about backlog. Rheinmetall's order backlog reached €63.2 billion at the end of June—up 30% year-over-year, and already equivalent to more than five full years of revenue at today's run rate. But that's just the tip of the spear. Management disclosed that the company is now tracking more than €80 billion in near-term nomination potential, and that it could breach €120 billion in backlog by mid-2026 if contract conversions proceed as expected.7

To put that in perspective: €120 billion in backlog would provide nearly seven years of forward sales coverage based on a 2026 revenue estimate of ~€17 billion.8 That's unprecedented in the context of European industrials, and it rivals the visibility you'd find in some U.S. prime contractors.

Crucially, the German government—Europe's largest defense buyer—has not yet fully executed on its promised spending. A €100 billion special fund was announced in 2022. Rheinmetall believes only a portion has been deployed. Legal frameworks now allow the government to expand existing framework agreements by 50% without re-tendering. That means €22 billion worth of current contracts could be expanded to €33 billion almost overnight.9

We saw figure 1 in Rheinmetall's most recent earnings presentation, and it led us to explore more about the process the company goes through to actually recognize revenues. The reason it attracted our attention—besides a big increase in the number from the left to the right—is that defense companies cannot take in an order and immediately deliver a tank or a plane or another type of system.

In Rheinmetall's terminology, a "nomination" refers to an official expression of intent from a government customer to procure a set of systems, typically under a framework agreement or early-stage contractual structure. It's not yet a firm order. It does not yet generate revenue. And it doesn't go into the order backlog until certain legal and financial steps are taken.

Here's a simplified hierarchy of the journey:

Even though nomination potential is pre-backlog, it's a powerful signal. Why?

High conversion likelihood

Rheinmetall has deep incumbency, especially in German programs. If the German government has nominated Rheinmetall to supply Boxer or Leopard 2 vehicles, it's not shopping around. The probability that this nomination becomes a signed order is high—especially in regulated, budget-allocated defense environments.

Long lead times in defense

Governments must sequence procurement years in advance. For instance, if Berlin wants a brigade equipped with new Puma IFVs in 2028, that nomination must exist in 2025 or earlier. The nomination is part of that long-cycle planning process, and it's often supported by funding discussions already underway.

Industrial planning signal

Rheinmetall uses nomination visibility to justify capital expenditures (capex), mergers & acquisitions (M&A) and plant conversion. The ammunition factory in Unterlüß was built on the back of nomination-level visibility—not signed orders. Nomination is strong enough for Rheinmetall to start spending money.

Source: "Q2 2025 conference call presentation" [slide deck], Rheinmetall AG, 8/7/25. https://www.rheinmetall.com

The sheer scale of what Germany is attempting is underappreciated. The Bundeswehr, long seen as underfunded and underequipped, is being rebuilt into the largest standing army in continental Europe. Berlin has committed to lifting defense spending from ~1.6% of gross domestic product (GDP) to 3.5% by 2035, with intermediate targets implying a €162 billion annual defense budget by 2029—up more than 70% from today.10

Rheinmetall is at the center of this transformation. It is not just winning contracts—it is being asked to manufacture at an entirely different scale. The company is building a new 155-mm ammunition plant in Unterlüß with a maximum capacity of 350,000 rounds per year. That facility went from idea to near-operational in under 16 months. The third production shift there will be run by robots. Elsewhere, Rheinmetall is rolling out automated vehicle assembly lines and drone manufacturing capabilities in northern Germany. These are not proposals. These are factories, either built or being built.11

International demand is accelerating as well. Rheinmetall has visibility into orders from Italy, Romania, Lithuania and the UK. It's expanding its footprint through joint ventures and acquisitions, including partnerships with Lockheed Martin (missiles), Anduril (drones and autonomy) and ICEYE (satellites). This isn't just a tank maker—it's becoming a full-spectrum integrator of land-based defense capabilities.12

The market has a habit of overreacting to quarterly results, especially when the stock has run. Rheinmetall had rallied nearly 60% year-to-date before the August pullback. Investors were primed for a beat-and-raise quarter. Instead, they got a beat-on-orders and delay-on-deliveries quarter, and the market treated that as a reset.13

But the underlying growth engine hasn't changed. If anything, it's gaining momentum. Rheinmetall now has more than €1 billion worth of finished goods sitting in inventory, including trucks, ammunition and air defense systems, simply waiting for approval and logistics coordination before shipping.14 As these approvals come through—likely in Q3 and Q4—that inventory becomes revenue. That revenue becomes cash. And that cash will close what now looks like a temporary hole in operating free cash flow.

This is why management maintained guidance but flagged that it's conservative. They fully expect to reassess once German procurement is clarified in September. That's a pragmatic approach, not a defensive one.

At a glance, Rheinmetall may seem like a niche European defense contractor. But the more you look, the clearer it becomes: This company sits at the heart of the most profound defense reorientation in Europe since the Cold War. It's not just aligned with the trend—it is the trend. From ammunition production and vehicle manufacturing to digital systems and missile propulsion, Rheinmetall is building the scaffolding for a self-sufficient European security architecture.

NATO's 3.5% target is more than a number. It's a directive. And Rheinmetall is one of the few firms with the capacity, capability and credibility to deliver on it.

So, while the stock may have stumbled post-earnings, the long-term story remains intact. More than that—it's accelerating. Investors willing to look past one quarter's logistics noise will find themselves holding an industrial compounder in the early stages of a massive demand curve. Rheinmetall might not be a household name in the U.S.—yet. But for those betting on the defense of democracy, it deserves a place in the conversation.

1 Source: L. Pitel, "Rheinmetall order growth slows amid change of government in Berlin," Financial Times, 8/7/25.

2 Source: M.-A. Riggio and R. Law, "Rheinmetall AG: Buy the dip – thesis intact" [equity research update], Morgan Stanley & Co. International plc., 8/8/25.

3 Source: Pitel, 2025.

4 Source: Riggio & Law, 2025.

5 Source: "Half-year 2025 earnings conference call transcript," Rheinmetall AG, Refinitiv StreetEvents, 8/7/25.

6 Source: Rheinmetall AG, 2025.

7 Source: Rheinmetall AG, 2025.

8 Source: Riggio & Law, 2025.

9 Source: M.-A. Riggio and R. Law, "Rheinmetall AG: 2Q25 results—low as expected; no guidance update seen as conservative" [equity research update], Morgan Stanley & Co. International plc., 8/7/25.

10 Source: Pitel, 2025.

11 Sources: "Q2 2025 conference call presentation" [slide deck], Rheinmetall AG, 8/7/25; "Half-year 2025 earnings conference call transcript," Rheinmetall AG, Refinitiv StreetEvents, 8/7/25.

12 Sources: "Q2 2025 conference call presentation" [slide deck], Rheinmetall AG, 8/7/25; "Half-year 2025 earnings conference call transcript," Rheinmetall AG, Refinitiv StreetEvents, 8/7/25.

13 Source: Riggio & Law, 2025.

14 Source: "Half-year 2025 earnings conference call transcript," Rheinmetall AG. Refinitiv StreetEvents, 8/7/25.

Europe Defense Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.