WDEF

Europe Defense Fund

Published July 24, 2025

Global Head of Research

Macro Strategist, Model Portfolios

U.S. investors are just beginning to notice the shift. Europe's defense landscape is fragmenting and reforming in a pattern that looks far more like a startup ecosystem than a legacy industrial base. National champions like Leonardo and Thales are fusing legacy platforms with cutting-edge cyber assets. Quietly, smaller players—particularly in Finland, Germany, Italy and the Baltics—are becoming indispensable links in Europe's evolving defense tech stack. This is where the opportunity lies: in recognizing that Europe's next generation of defense is not simply an expansion of what already exists but a re-platforming of what defense even means. When the world's defense priorities shift toward autonomy, data resilience and AI-driven decision cycles, Europe's next-generation edge could become the core of a global investment thesis.

If there's one company that epitomizes Europe's redefinition of defense, it's Thales. Long seen as a quiet powerhouse behind radar systems, avionics and encrypted communications, Thales has become the cornerstone of Europe's digital shield. With roots in military electronics, the company has leaned hard into cyber, doubling down through acquisitions like Imperva and Tesserent, and quadrupling its cybersecurity revenues since 2016.2 Now ranked among the top five global players in cyber defense, Thales anchors sovereign cloud infrastructure, zero-trust architecture3 and AI-enabled threat intelligence for the North Atlantic Treaty Organization (NATO), the European Union (EU) and critical global enterprises. And this isn't aspirational—it's operational. In 2024 alone, Cyber & Digital sales rose nearly 15%, while EBIT4 margins in that segment hit an enviable 14.5%.5

But Thales is not just scaling cyber revenues—it's defining what modern defense looks like. Nearly €4.2 billion annually is pumped into R&D—20% of the company's entire sales base—funding everything from autonomous maritime drones to AI-powered data risk platforms. Their internal cortAIx initiative, now home to 800 AI experts and 100+ integrated products, is building the trusted AI layer for military and critical infrastructure across Europe.6 For investors, this is where the signal rises above the noise: Thales is not a niche cyber play or a legacy defense contractor—it's the connective tissue of European security, fusing software, sensors and systems into a tech-centric moat. With guidance for 5%–7% annual organic sales growth and record-high orders of €25.3 billion in 2024, Thales is building one of the most durable and defensible franchises in European defense tech.7

Figure 1: Trustworthy AI and Tactical Tech: Thales' Innovation Portfolio

Source: Thales Group, "2024 Full-Year Results: Investor Presentation," thalesgroup.com, 3/4/25. R&D stands for research and development. IFE stands for in-flight entertainment. AI refers to artificial intelligence.

For most U.S. investors, Leonardo is a name that rings faintly, if at all. Yet in Europe, it's the backbone of Italy's defense-industrial complex and a major player across aerospace, helicopters and secure communications. What's changing—and fast—is the company's DNA. Leonardo is no longer just building hardware; it's embedding itself into the software layer of 21st-century defense. In 2024, the company generated over €4 billion in revenue from its Cyber & Security Solutions division and announced a multi-year roadmap to double that figure.8 That plan includes targeted acquisitions of smaller cybersecurity firms and aggressive expansion in digital command-and-control infrastructure—an area where digital sovereignty and NATO interoperability are converging into a new must-have standard.

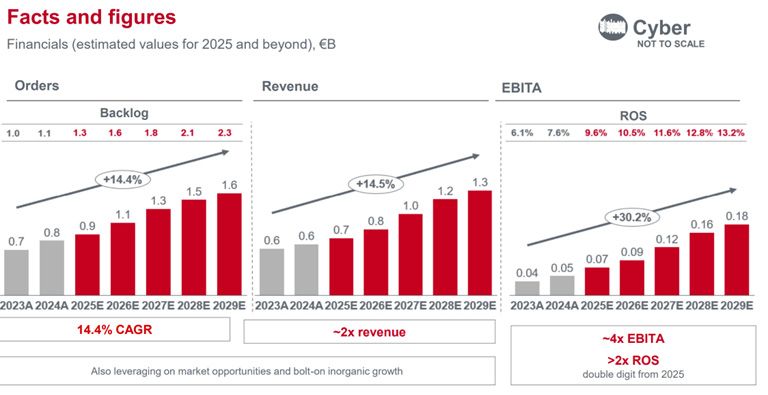

The shift is not cosmetic. Leonardo's cyber push is central to its transformation into a full-spectrum aerospace, defense and security provider. It's backing that ambition with real capital: in July 2025, it acquired a 24.55% stake in Finland's SSH Communications Security, a specialist in quantum-safe encryption and privileged access management—technologies that will likely define the next decade of defense-grade network architecture.9 The company's roadmap points to a cyber division growing at a 14.4% CAGR, with EBITA10 forecasted to quadruple by 2028.11 What Thales is to Franco-European cyber infrastructure, Leonardo is fast becoming for southern Europe—a digital anchor tied to real hardware, trusted by governments and strategically built to secure the future battlefield.

Figure 2: Doubling Down on Digital: Leonardo's Cyber Trajectory

Source: Leonardo S.p.A., "Annual Shareholder Meeting 2025: Investor Presentation," leonardo.com, 5/6/25. €B stands for euros, in billions. An ‘A' after a year is actual. An ‘E' after a year is an estimate made by the company, in this case, Leonardo. CAGR refers to compound annual growth rate. EBITA refers to earnings before interest, taxes and amortization. ROS refers to return on sales.

Most U.S. investors still associate the name "Saab" with quirky Scandinavian cars. But the brand exited the auto business over a decade ago, and what emerged is one of Europe's most advanced, software-integrated defense platforms. With Sweden and Finland now in NATO, Saab's order book is surging—its SEK 197.6 billion backlog reflects growing global demand for electronic warfare suites, networked sensors and advanced air defense systems.12 The company has ramped up investment in "software-defined" and AI-enabled defense infrastructure, including new capabilities in collaborative autonomous drones (Gnadd), passive EW systems (Sirius Compact) and AI-based command and control architectures.

If you're looking for a case study in how shifting geopolitical realities translate into corporate performance, Saab is writing a textbook in real time. The backdrop couldn't be clearer: NATO's post-summit commitment to 5% of gross domestic product (GDP) defense spending by 2035 is no longer theoretical—it's becoming operational.13 Sweden, now a NATO member, is putting SEK 300 billion behind that shift.14 Saab finds itself not just participating in this environment but increasingly defining the categories that matter: long-range surveillance, multi-domain deterrence and aerial sovereignty. The GlobalEye and Gripen E/F platforms are now being discussed not just with Thailand and Colombia, but as part of NATO interoperability frameworks, with France publicly aligning on future procurements. You don't get into those conversations unless your product is not just good, but uniquely valuable. That's what makes Saab's order intake so telling—SEK 28.4 billion this quarter, skewed toward small- and medium-sized deals.15 That's how you know the demand is real and urgent. Countries aren't waiting. They're buying now.

And Saab is executing on the opportunity. Organic revenue up 32%—yes, that's the real number. Dynamics posted 73% top-line growth, with EBIT margins leaping to 20.9%, and Surveillance wasn't far behind with 21% growth and margin expansion to 9.0%. What's powering that isn't just sales, but throughput. They're delivering systems, not just talking about them. It's worth pausing on what that does to the P&L: EBIT up 49%, margins to 10.0% and a full-year sales growth guide raised to 16%–20%. Importantly, they're doing this while ramping up R&D—SEK 1.7 billion in H1—and still improving profitability.16 They ran their first AI-enabled Gripen test flight this quarter. Their counter-drone solution landed its first export deal. These aren't speculative R&D projects. They're live. Cash flow was negative, but for good reasons: capacity buildouts, inventory to meet future demand and a supply chain being proactively fortified. Returns on capital and equity rose to 15.3% and 14.0%, respectively.17 This isn't a quarter you celebrate. It's one you build from. Saab knows where defense is headed, and it's moving there with speed and precision.

If Europe's rearmament has a neural network, Hensoldt is the signal processor behind it. Spun off from Airbus in 2017, Hensoldt has become Germany's national champion in radar, electromagnetic warfare and battle-proven sensor integration. It's a company that operates in the shadows—developing the critical sensing, jamming and decision-support layers that make 21st-century defense systems intelligent, interoperable and resilient. With over €6.929 billion in backlog, Hensoldt has hit structural growth velocity, driven by radar production, integrated optronics and secure electronic intelligence systems that underpin Europe's multi-domain operations.18 It's also one of the few defense tech companies explicitly architecting its strategy around "software-defined defence"—a term that, in Hensoldt's case, isn't marketing speak, but a business model centered on data, modularity and sensor fusion.

The company's role isn't about volume—it's about informational dominance. Whether through advanced radar for Eurofighters and future combat air systems, secure communication layers for tactical edge units or cyber defense infrastructure to shield critical sensor data, Hensoldt is playing the long game in defense autonomy and information superiority. Its growth is methodical and margin-rich: Hensoldt delivered nearly €405 million in adjusted EBITDA in 2024, with over 18% margins and cash conversion in the 50%–60% range. With demand accelerating across NATO for modular, cyber-hardened ISR and C4ISR components, Hensoldt's path toward €5 billion in revenue by 2030—up from €2.2 billion in 2024—isn't speculative, it's strategic.19 In short: this is one of the most critical and underrecognized players in the race for digital sovereignty in European defense.

Europe is not just catching up in defense—it's leapfrogging into domains that will define the next era of deterrence. Investors conditioned to focus on U.S. primes and traditional platforms may be missing a far more dynamic story: a continent forced by geopolitical urgency to rethink sovereignty, resilience and how software integrates with steel. What's emerging is a new industrial layer—one powered by secure sensors, cyber-immune networks, AI-augmented decision cycles and high-value integration across land, air, sea, space and data. These aren't just defense companies anymore—they're critical infrastructure builders for a new era of multipolar conflict and digital warfare.

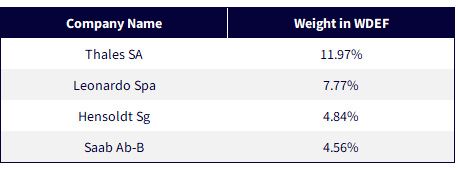

Thales, Leonardo, Saab and Hensoldt are building the digital backbone of NATO's evolving posture. The WisdomTree Europe Defense Fund (WDEF), which is tracking the total return performance of the WisdomTree Europe Defense Index, has exposure to all four of these firms and provides an option for U.S. investors seeking to gain exposure to what we believe is a defining global feature of the coming decade, and perhaps even longer.

Figure 3: Exposure in WDEF to the Companies Discussed in This Piece

Source: WisdomTree, with data as of the market's open on 7/17/25, the first day of trading for WDEF. Subject to change.

1 Source: "The Costly End of Europe's ‘Peace Dividend,'" Financial Times, 3/17/25.

2 Source: R. Throsby, "France's Thales Sees Revenue and Profit Growth after Cyber Expansion," Reuters, 11/14/24.

3 Zero trust architecture in cybersecurity is a security model based on the principle, "Never trust, always verify."

4 EBIT refers to earnings before interest and taxes.

5 Source: Thales Group, "Thales Reports its 2024 Full-Year Results," thalesgroup.com, 3/4/25.

6 Sources: Thales Group, "Thales Builds on Four Key Strengths: €4.2 Billion in R&D, Around 800 AI Experts, Over 20,000 Patents," PublicNow, June 2024; Thales Group, "Thales Speeds Up R&D on AI for Defence: Launch of cortAIx AI Accelerator," Aviation Defence Universe, 3/29/24; Thales Group, "cortAIx SG: Thales Accelerates Trusted AI Innovation in Singapore," thalesgroup.com, 6/2/25.

7 Source: R. Throsby, "France's Thales Sees Revenue and Profit Growth after Cyber Expansion," Reuters, 11/14/24.

8 Source: Leonardo S.p.A., "Board of Directors Approves FY 2024 Results and 2025 Guidance," leonardo.com, 3/11/25.

9 Source: "Italy's Leonardo Becomes Biggest Shareholder of Finland's SSH with Stake Purchase," Reuters, 7/1/25.

10 EBITA refers to earnings before interest, taxes and amortization.

11 Source: "Leonardo: Industrial Plan Update – Cyber Division Growth Guidance," EDR Magazine, 3/11/25.

12 Source: Saab AB, "Q2 2025 Interim Report: Accelerating Growth and Strengthening our Market Position," saab.com, 7/18/25.

13 Source: North Atlantic Treaty Organization, "NATO Concludes Historic Summit in The Hague," nato.int, 6/25/25.

14 Source: Government of Sweden, "CrossParty Agreement on Historic Rearmament," government.se, 6/19/25.

15 Source: Saab AB, "Q2 2025 Interim Report: Accelerating Growth and Strengthening our Market Position," saab.com, 7/18/25.

16 Source: Saab AB, "Q2 2025 Interim Report: Accelerating Growth and Strengthening our Market Position," saab.com, 7/18/25.

17 Source: Saab AB, "Q2 2025 Interim Report: Accelerating Growth and Strengthening our Market Position," saab.com, 7/18/25.

18 Source: HENSOLDT AG, "HENSOLDT Reports Strong First Quarter 2025 with Growth in Order Intake and Revenue," hensoldt.net, 5/7/25.

19 Source: HENSOLDT AG, "HENSOLDT Achieves Record Order Backlog in Financial Year 2024 – Guidance for All Key Figures Met, Partly Exceeded," hensoldt.net, 2/27/25.

For current holdings of WDEF, please click here. Holdings are subject to risk and change.

There are risks associated with investing, including the potential loss of principal. Foreign investing involves specific risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. This Fund focuses its investments in Europe, thereby increasing the impact of events and developments in Europe that can adversely affect performance. Europe has and may continue to experience security concerns, war, threats of war, aggression and/or conflict, terrorism, economic uncertainty, sanctions or the threat of sanctions, natural and environmental disasters, the spread of infectious illness, widespread disease or other public health issues and/or systemic market dislocations that lead to increased short-term market volatility and have adverse long-term effects on European and world economies and disrupt the orderly functioning of securities markets generally, which may negatively impact the Fund’s investments. Many countries within Europe are closely connected and their economies and markets are largely interdependent. As such, economic and political events in one European country, including monetary exchange rates between European countries and armed conflicts among two or more European countries, may have adverse effects across Europe. European countries that are members of the European Union (“EU”) and the European Economic and Monetary Union (“EMU”) are subject to certain economic and monetary policies and controls and the risks associated with such coordinated economic and fiscal policies. Because the Fund invests primarily in the securities of companies in Europe, the Fund’s performance is expected to be closely tied to social, political and economic conditions within Europe and to be more volatile than the performance of more geographically diversified funds. Investments in non-U.S. securities involve political, regulatory and economic risks that may not be present in investments in U.S. securities. The securities of small-capitalization companies generally trade in lower volumes and are subject to greater and more unpredictable price changes than larger-capitalization stocks or the stock market as a whole. The Fund invests in the securities included in, or representative of, its Index. The Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Europe Defense Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.