CXSE

China ex-State-Owned Enterprises Fund

Published July 22, 2025

Director of Modern Alpha

China's economic trajectory continues to be a subject of global scrutiny, especially as its internal policies and external negotiations evolve rapidly. In two recent episodes of the China of Tomorrow podcast, Liqian Ren shares insights on China's domestic economic strategies, the dynamics of U.S.-China trade talks and China's positioning in global geopolitics, particularly in the Middle East. Below is a summary and analysis of these discussions.

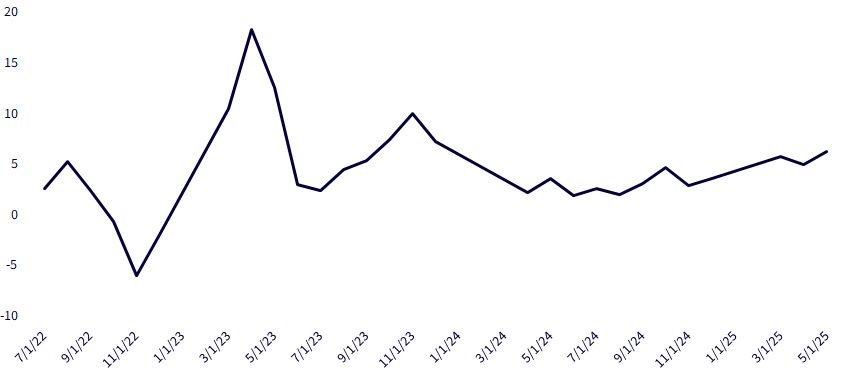

Throughout 2025, China's leadership has cautiously deployed fiscal stimulus in a bid to invigorate domestic demand. A standout move involved targeted subsidies via consumption coupons—particularly for durable goods such as automobiles.

Instead of handing out checks as seen in the U.S., the Chinese government chose a more indirect approach: providing subsidies to manufacturers that translate into consumer discounts. This policy led to a notable spike in total retail sales, reaching an upbeat May year-over-year increase of 6.4%.

Figure 1: China's Total Retail Sales % (Year-over-Year)

Sources: China Stats Bureau, Fred Data, for the period 7/1/22–5/1/25.

Skepticism persists regarding official data, but indicators like retail sales, inflation and PMI are still viewed as relatively reliable due to verifiability through secondary sources.

Interestingly, while core CPI shows mild growth, headline inflation remains near or below zero. This duality reflects a fragile yet not entirely deteriorating economic environment. In China's 40-year growth history, this is an unprecedented challenge and both the government and the Chinese public are yet fully convinced on what kinds of policies will work. Though the government has found some success in consumption coupons, we believe it will continue the program and expand it to stimulate beyond goods and into services like travel.

Figure 2: China Inflation Rate (Year-over-Year)

Sources: China Stats Bureau, Fred Data, as of 1/1/87–5/1/25.

China's export figures to the U.S. in May 2025 declined sharply—by 30% compared to the previous year—compounding April's 20% drop. High tariffs and logistical bottlenecks have contributed to the plunge, despite ongoing demand from U.S. firms. In response, China continues leveraging trans-shipping routes through Southeast Asia, with firms shifting production to countries like Vietnam and Cambodia to sidestep tariff constraints.

This reshuffling of the global supply chain underscores a broader trend: while the U.S. may seek to decouple from China, Southeast Asia is becoming a proxy battlefield for economic influence.

While China dominates rare earth processing, the U.S. will start investing in this area due to its strategic importance. The dialogue also highlighted key personnel involved in negotiations, including seasoned Chinese bureaucrats and influential U.S. representatives.

Both sides appear to be maneuvering with deliberate intent, using economic levers to shape a prospective deal. Expectations are building for a diplomatic exchange—Trump visiting China, followed by Xi's reciprocal state visit to the U.S.—which makes a tangible agreement more likely despite ongoing volatility.

In the wake of U.S. strikes on Iranian nuclear facilities, China's responses have been measured. Notably, Beijing first released its four-point statement via Twitter, bypassing traditional Chinese media. China's response to the U.S. bombing was subdued, reflecting its historically limited engagement in the Middle East despite growing economic ties, though its direct economic ties with Iran are minimal.

While not deeply entrenched in the region geopolitically, China's economic interests continue to expand. Observers should watch for more assertive soft-power strategies, especially as China balances relations with both the West and Middle Eastern states.

China is making progress in several industries, not just AI. As we've mentioned several times, it is becoming clear that the DeepSeek moment is not just for AI, but broader. However, Chinese firms have difficulty maintaining high profit margins, as China is still not yet at the technology frontier and competition is fierce.

Chinese equity could outperform, as fiscal stimulus is now in place and investors are now more convinced that the Party actually also tends to walk back to spur short-term economic growth.

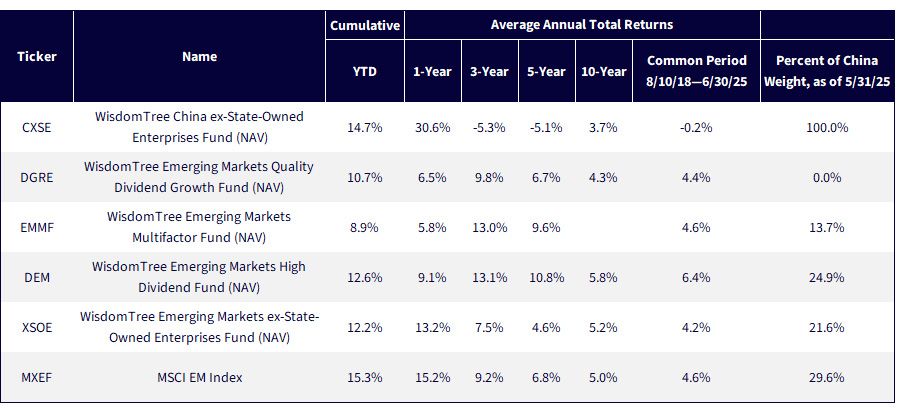

We offer a range of products, from pure China plays in the WisdomTree China ex-State-Owned Enterprises Fund (CXSE), to no China, to having some China, in WisdomTree Emerging Markets Multifactor Fund (EMMF), and full China weight as driven by WisdomTree Emerging Markets ex-State-Owned Enterprises Fund (XSOE) and WisdomTree Emerging Markets High Dividend Fund (DEM).

Figure3: Performance

Sources: WisdomTree, FactSet, as of 6/30/25. The performance data quoted represents past performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click the respective ticker: CXSE, DGRE, EMMF, DEM, XSOE.

China's internal and external policies are clearly in flux. Through calibrated stimulus, shifting trade strategies and sophisticated geopolitical messaging, Beijing is navigating a complex and often contradictory global landscape, with some success.

To dive deeper into the economic forces shaping China's future, listen to the latest episodes of the China of Tomorrow podcast.

There are risks associated with investing, including the possible loss of principal. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

CXSE: Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in China, including A-shares, which include the risk of the Stock Connect program, thereby increasing the impact of events and developments associated with the region which can adversely affect performance. Investments in emerging or offshore markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. The Fund’s exposure to certain sectors may increase its vulnerability to any single economic or regulatory development related to such sector. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers.

DGRE: Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Funds focusing on a single sector generally experience greater price volatility. Investments in emerging, offshore or frontier markets are generally less liquid and less efficient than developed markets and are subject to additional risks, such as of adverse governmental regulation, intervention and political developments. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs.

EMMF: Investments in non-U.S. securities involve political, regulatory and economic risks that may not be present in U.S. securities. For example, foreign securities may be subject to risk of loss due to foreign currency fluctuations, political or economic instability, or geographic events that adversely impact issuers of foreign securities. Derivatives used by the Fund to offset exposure to foreign currencies may not perform as intended. There can be no assurance that the Fund’s hedging transactions will be effective. The value of an investment in the Fund could be significantly and negatively impacted if foreign currencies appreciate at the same time that the value of the Fund’s equity holdings falls. While the Fund is actively managed, the Fund’s investment process is expected to be heavily dependent on quantitative models and the models may not perform as intended.

Additional risks specific to EMMF include but are not limited to emerging markets risk. Investments in securities and instruments traded in developing or emerging markets, or that provide exposure to such securities or markets, can involve additional risks relating to political, economic or regulatory conditions not associated with investments in U.S. securities and instruments or investments in more developed international markets.

DEM: Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Funds focusing on a single sector generally experience greater price volatility. Investments in emerging, offshore or frontier markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation, intervention and political developments. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time.

XSOE: Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Investments in emerging or offshore markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. Funds focusing their investments on certain sectors and/or regions increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index or take defensive positions in declining markets.

Director of Modern Alpha

Liqian Ren, Ph.D., joined WisdomTree as Director of Modern Alpha in 2018. She leads WisdomTree’s quantitative investment capabilities and serves as a thought leader for WisdomTree’s Modern Alpha® approach. Liqian was previously at Vanguard, where she worked for 12 years, most recently as a portfolio manager in the Quantitative Equity Group managing Vanguard’s active funds and conducting research on factor strategies. Prior to joining Vanguard, she was an associate economist at the Federal Reserve Bank of Chicago. Liqian received her bachelor’s degree in Computer Science from Peking University in Beijing, her master’s in Economics from Indiana University—Purdue University Indianapolis, and her MBA and Ph.D. in Economics from the University of Chicago Booth School of Business. Liqian co-hosts a podcast on China and Asian markets with Jeremy Schwartz, WisdomTree’s Global Head of Research, and she is a co-host on the Wharton Business Radio program Behind the Markets on SiriusXM 132.