DDWM

Dynamic International Equity Fund

Published December 12, 2025

Global Head of Research

Through the first nine months of 2025, developed-market ex-U.S. equity ETFs have attracted $76.3 billion in net inflows, a number that commands attention not just for its size, but for its trajectory. Roughly $31 billion of that arrived in the last three months alone, meaning more than 40% of the year's total came during Q3. Momentum has clearly shifted from episodic curiosity to sustained reallocation. September alone added another $9 billion, underscoring how global allocators are now leaning into regions that once sat dormant in portfolios.1

The pace and sequencing matter. In a world still digesting a higher-for-longer rate regime, this concentration of inflows signals a structural re-rating of opportunity outside the U.S. Investors are responding not to headline gross domestic product (GDP) surprises but to earnings resilience, fiscal pragmatism and corporate reform taking root across Europe and Japan.2 The flows suggest allocators are no longer viewing international diversification as a hedge. Instead, it's starting to look like a core engine of returns.

Re-Engaging with Global Equities through a Disciplined Lens

For investors looking to reweight toward developed markets outside the U.S., the WisdomTree Dynamic International Equity Fund (DDWM)3 offers an efficient bridge between macroeconomic awareness and portfolio practicality. It provides diversified exposure to dividend-paying companies across the industrialized world. It covers Europe, Japan and other developed economies, excluding the U.S. and Canada, while dynamically managing currency risk, a factor that has historically amplified volatility for U.S. dollar-based investors.

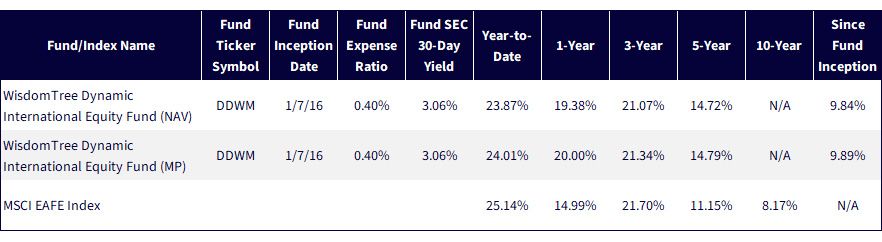

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 10/21/25 with returns as of 9/30/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

Performance: Consistency across Cycles, Not Just a Single Year

When evaluating any broad-based international equity strategy, the natural benchmark is the MSCI EAFE Index, the default measure of developed markets outside the U.S. and Canada. Against that backdrop, DDWM's track record speaks to consistency rather than coincidence.

Through late 2025, DDWM has delivered competitive year-to-date results, roughly in line with the MSCI EAFE. The more telling story emerges over longer horizons. Over one-, three-, five-year and longest common period comparisons, DDWM's rules-based framework has translated into higher compounded returns.

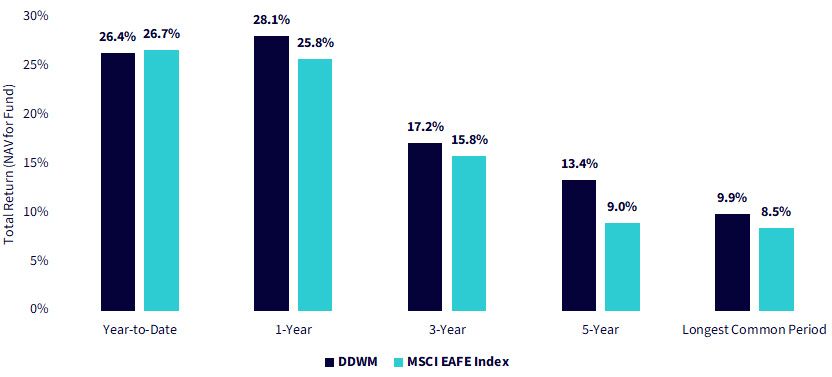

Figure 2: Consistent Performance across Cycles

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 11/28/25 with returns as of 11/26/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

Over the past five years, the DDWM has delivered something investors chronically underestimate: consistency through turbulence. The chart tells a clear story. While global markets oscillated through inflation spikes, tightening cycles and currency shocks, DDWM's performance line rarely lost its composure.

The outcome is notable. By November 2025, DDWM's five-year annualized return sits meaningfully above MSCI EAFE's. But more importantly, the path to those returns has been smoother. The strategy didn't depend on one heroic rally, it benefited from a disciplined process that adapts when currencies swing, rewards cash-flow resilience and maintains exposure where the earnings power is most durable. In an environment where global leadership is rotating and volatility remains part of the landscape, consistency is not defensive, it's a competitive advantage.

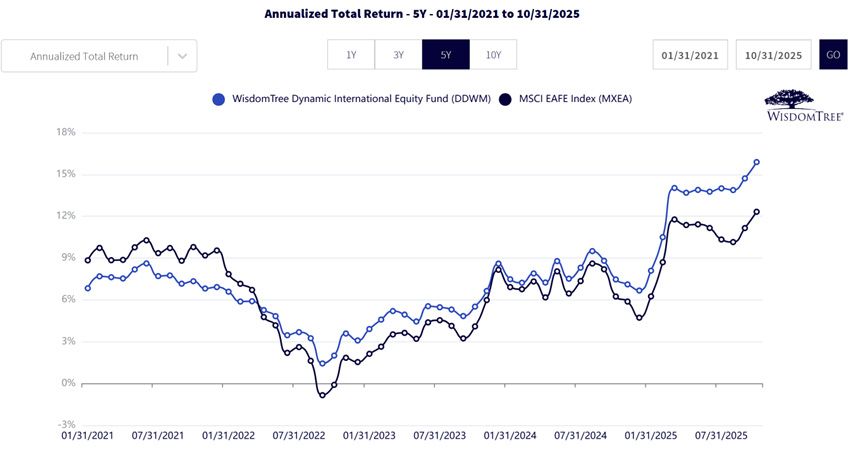

Figure 3: A Comparison of Rolling 5-Year Annualized Returns

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 11/28/25 with returns as of 10/31/25. 5-Year annualized returns are calculated monthly, starting from 1/31/16 to 1/31/21, which is the first full five-year period. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here. To download the Fund prospectus, click here.

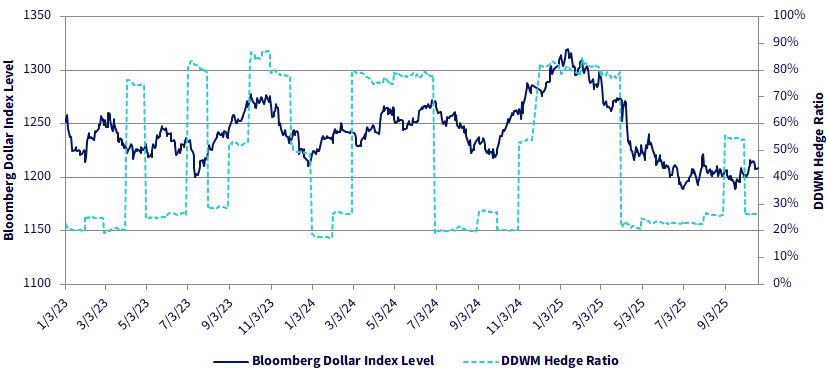

How Dynamic Currency Hedging Has Worked

For U.S.-based investors, foreign equity exposure carries a second layer of volatility through currency. When the U.S. dollar strengthens, returns on international equities often compress once translated back into dollars. When the dollar weakens, those same foreign returns can receive a tailwind. The challenge is that few investors can, or should, try to time those cycles.

That's where DDWM's dynamic currency hedging framework becomes an additional performance lever. The chart illustrates this: the solid line represents the Bloomberg Dollar Index, while the dashed line shows DDWM's hedge ratio, or the percentage of foreign currency exposure that's neutralized. When the dollar trend turns higher, signaling potential headwinds for unhedged international assets, the model has systematically increased the hedge ratio. Conversely, when the Bloomberg Dollar Index weakened, the model allowed more foreign-currency participation by lowering the dynamic hedge ratio.

For investors translating global opportunities back into U.S. dollars, this adaptive layer effectively reduced one of the least rewarded risks in international investing—currency swings—without requiring active intervention. Over time, it's a subtle but powerful mechanism that can have the potential to smooth the path of returns and improve consistency across market regimes.

Figure 4: How Dynamic Currency Hedging Adjusted with the Dollar Cycle

Sources: WisdomTree, Bloomberg, with the period calculated from 1/3/23–11/21/25. Past performance is not indicative of future results.

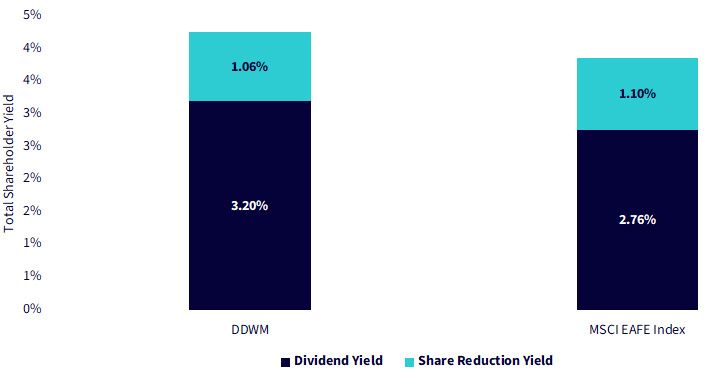

At the heart of DDWM's methodology is a deceptively simple idea: start with companies that pay dividends, then weight them by the size of those dividends rather than by market capitalization. That single design choice changes the character of the portfolio. It naturally tilts DDWM toward firms with durable cash flows, shareholder-friendly balance sheets and valuation awareness, attributes that often get diluted in cap-weighted benchmarks like MSCI EAFE.

The impact shows up in the numbers. As figure 5a illustrates, DDWM's total shareholder yield of roughly 4.3%, a blend of 3.2% dividend yield and 1.1% share-reduction yield, sits above MSCI EAFE's 3.9% total. That higher yield is more than just income; it's a signal of capital discipline and a margin of safety in a world where cash flow consistency is rare.

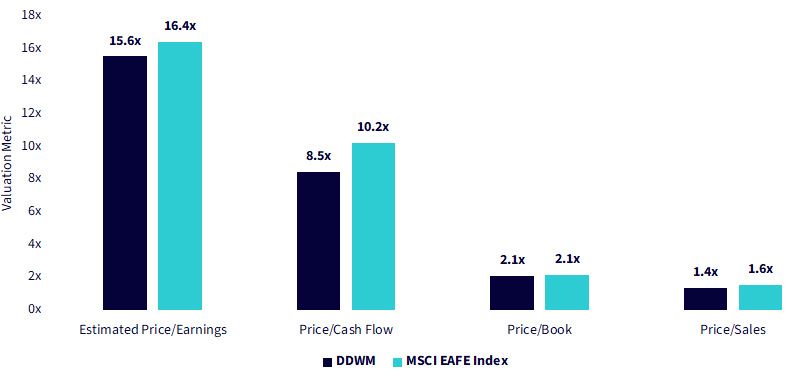

Those same structural choices also deliver valuation resilience. By emphasizing dividend weight rather than following market capitalization, DDWM maintained lower multiples across many major metrics shown in figure 5b: price-to-earnings, price-to-cash-flow, price-to-book and price-to-sales. In other words, the strategy doesn't just chase yield; it embeds valuation discipline directly into its DNA, offering investors a way to participate in global equity growth while managing one of the most persistent portfolio risks, overpaying for it.

Figure 5a: How Dividend Weighting Translated into Greater Total Shareholder Yield

Sources: WisdomTree, FactSet and Morningstar. Data as of 10/31/25. Subject to change.

Figure 5b: An Illustration of Valuation Discipline

Sources: WisdomTree, FactSet and Morningstar. Data as of 10/31/25. Subject to change.

The global market landscape of late 2025 looks fundamentally different from the one investors faced even a year ago. Capital is rotating toward developed markets beyond the U.S., and that rotation is increasingly being led by fundamentals rather than fear. In this environment, DDWM stands out as a purpose-built framework for capturing those evolving opportunities, not by prediction, but by process. Its combination of dividend-weighted stock selection, dynamic currency hedging and valuation discipline has proven capable of delivering consistent, risk-aware returns across multiple market regimes.

For investors seeking to modernize their global equity exposure, the message is clear: geographic diversification is no longer defensive; it's opportunistic. DDWM offers a structured way to participate in that shift, aligning with regions undergoing reform and reinvestment, while controlling for the volatility that often keeps U.S. investors on the sidelines. As the world continues to reprice, portfolios that can adapt systematically, the way DDWM does, may be positioned not just to keep pace, but to compound ahead.

1 Source: "SPDR ETFs Monthly Chart Pack," State Street Global Advisors, October 2025.

2 Source: State Street Global Advisors, 2025.

3 DDWM is designed to track the total return performance, before fees and expenses, of the WisdomTree Dynamic International Equity Index.

You cannot invest directly in an index.

Prior to April 30, 2025, the Fund was known as the WisdomTree Dynamic Currency Hedged International Equity Fund.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund invests in derivatives in seeking to obtain a dynamic currency hedge exposure. Derivative investments can be volatile, and these investments may be less liquid than other securities, and more sensitive to the effects of varied economic conditions. Derivatives used by the Fund may not perform as intended. A Fund that has exposure to one or more sectors may be more vulnerable to any single economic or regulatory development. This may result in greater share price volatility. The composition of the Index underlying the Fund is heavily dependent on quantitative models and data from one or more third parties, and the Index may not perform as intended. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Dynamic International Equity Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.