Time to Look Outward: The Case for Global Leadership beyond the U.S.

Published November 17, 2025

Christopher Gannatti, CFA

Global Head of Research

Key Takeaways

- Developed international markets are trading at steep discounts to the U.S. while delivering growth driven by real earnings, not inflated valuations.

- Structural reforms in Europe and Japan are fueling a new era of innovation, productivity and competitiveness.

- With supportive monetary policies and improving fundamentals abroad, global equities are poised to take the lead from the U.S.

U.S. equities remain expensive,1 yet investors cling to them. That home bias has paid off, but valuations now argue for looking abroad. Developed markets offer broader diversification, stronger reform-driven earnings and less expensive multiples. Ignoring them risks missing value and balance—since leadership often shifts to where expectations are lowest and fundamentals are improving.

- Valuations and Quality of Growth

Developed international markets are trading at meaningful valuation discounts—roughly 8 price-to-earnings points below the U.S.2—yet are delivering performance driven by earnings growth, not multiple expansion. Corporate reforms, stronger balance sheets and rising dividends make this growth potentially more sustainable and shareholder-friendly.

- Structural Economic Shift

A fundamental transformation is underway across developed economies. Japan and Europe are redirecting spending toward defense, innovation and productivity—long-term growth levers absent for decades.3 These shifts represent durable policy changes, not short-term cycles, and are reshaping the earnings base and competitiveness of international markets for the next decade.

- Monetary Tailwinds and Normalization

Unlike the U.S., most developed markets now enjoy positively sloped yield curves and more accommodative central banks. Aggressive rate cuts and normalized term structures favor credit growth and financials, creating monetary conditions that support continued earnings expansion without the valuation stress present in U.S. equities.4

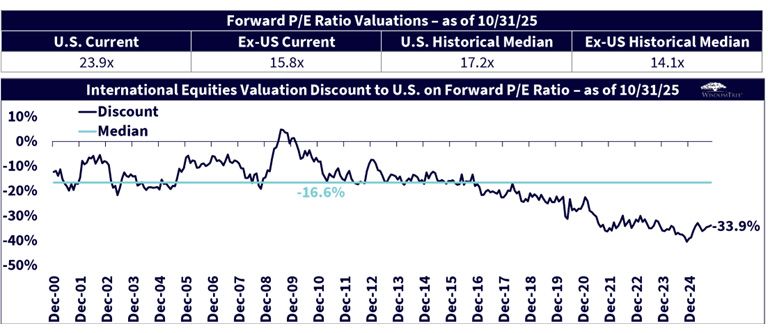

We see in figure 1, despite strong performance abroad, international equities remain deeply discounted compared to the U.S.—trading at a 34% forward price-to-earnings discount, twice their long-term median. The U.S. commands a 24-times multiple on stretched earnings, while ex-U.S. markets sit near 16 times with improving fundamentals. The valuation gap underscores overlooked opportunity, not underlying weakness.

Figure 1: Overlooked Opportunity vs. Underlying Weakness?

Sources: WisdomTree, MSCI, S&P. Data begins 12/29/2000 to coincide with inception of MSCI AC World ex-US Index. U.S. measured by S&P 500 Index. Ex-U.S. measured by MSCI AC World ex-US Index. You cannot invest directly in an index.

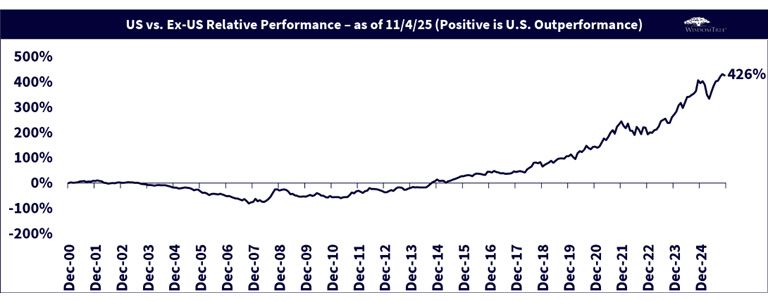

In figure 2, we show that U.S. equities have outperformed international markets by over 400% since 2009—a dominance driven largely by multiple expansion and mega-cap concentration. That extraordinary run has stretched relative valuations to extremes. History suggests such gaps eventually revert, setting the stage for international markets to reclaim leadership as fundamentals, policy and valuations realign.

Figure 2: History Suggests that Such Gaps Eventually Revert

Sources: WisdomTree, MSCI, S&P. Data begins 12/29/2000 to coincide with inception of MSCI AC World ex-US Index. U.S. measured by S&P 500 Index. Ex-U.S. measured by MSCI AC World ex-US Index. You cannot invest directly in an index.

Conclusion: We Believe U.S. Equity Investors Need to Look Abroad

Developed international is set up for a hand-off: wide valuation discounts, real earnings drivers (reform, capex, dividends) and policy normalization versus a richly priced U.S. After an historic run of U.S. outperformance, the asymmetry now favors looking outward—where expectations are lower and cash returns matter more.

To express that view with discipline, consider:

1 Expensive refers to valuation, specifically metrics like the price-to-earnings (P/E) ratio where the valuation of the U.S. equity market remains high relative to the developed international equity market, with data sourced from Bloomberg as of 11/5/25. U.S. equities represented by S&P 500 Index; ex-U.S. equities represented by MSCI AC World ex-US Index.

2 Sources: WisdomTree, MSCI, S&P. Data as of 10/31/25, comparing the forward P/E ratio of the S&P 500 Index and the MSCI AC World ex-US Index.

3 Sources: Directorate-General for Economic and Financial Affairs, "The Economic Impact of Higher Defence Spending (Box 1)," Spring 2025 Economic Forecast: Moderate Growth amid Global Economic Uncertainty, European Commission, 5/19/25; "Defense of Japan 2025: Digest (Overview of FY2025 Budget & Fundamental Reinforcement of Defense Capabilities)," Japan Ministry of Defense, 2025.

4 Source: "Deposit Rate Reduced to 2 % as Euro-Area Financing Conditions Ease," European Central Bank, 6/5/25.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund invests in derivatives in seeking to obtain a dynamic currency hedge exposure. Derivative investments can be volatile, and these investments may be less liquid than other securities, and more sensitive to the effects of varied economic conditions. Derivatives used by the Fund may not perform as intended. A Fund that has exposure to one or more sectors may be more vulnerable to any single economic or regulatory development. This may result in greater share price volatility. The composition of the Index underlying the Fund is heavily dependent on quantitative models and data from one or more third parties, and the Index may not perform as intended. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

About the contributor

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.