DNL

Global ex-US Quality Growth Fund

Published October 23, 2025

Director, Research

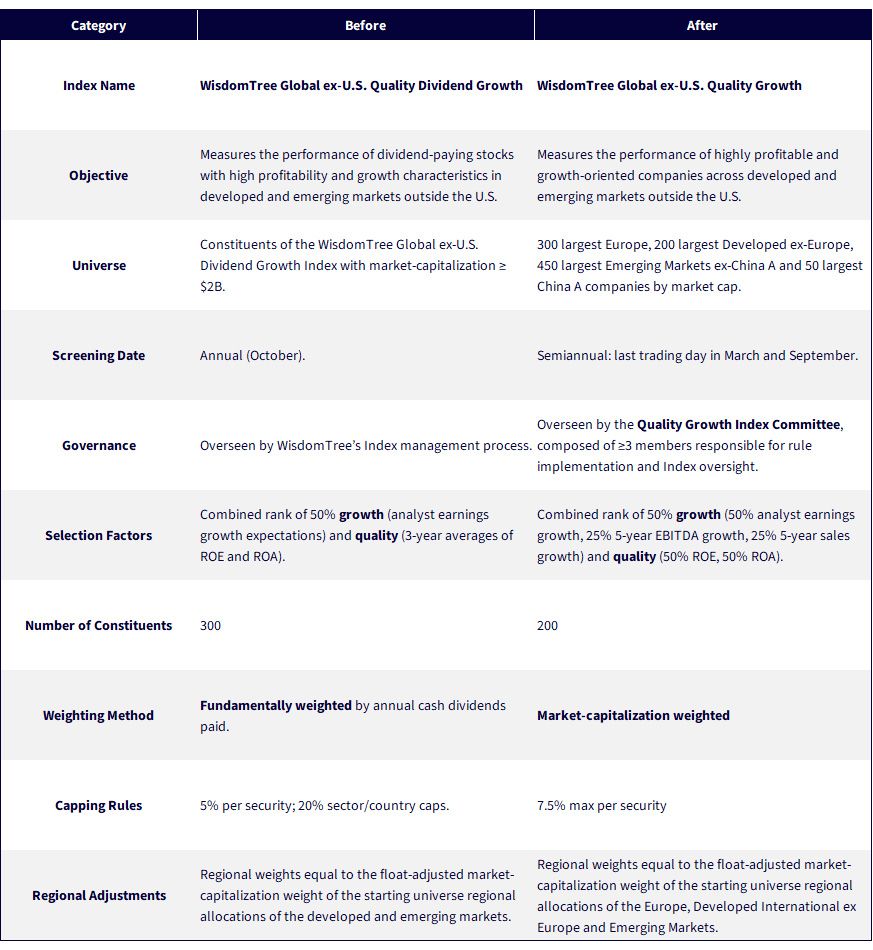

The WisdomTree Global ex-U.S. Quality Growth Fund (DNL) is evolving.

Reflecting its broadened universe, the Fund is dropping "Dividend" from its name and introducing enhancements to its methodology designed to better capture global quality growth opportunities.

Effective October 23, the WisdomTree Global ex-U.S. Quality Growth Fund—which tracks the similarly renamed WisdomTree Global ex-U.S. Quality Growth Index—will broaden its scope to include non-dividend-paying companies and shift its weighting approach from dividend-based to market-capitalization.

DNL has long been the global ex-U.S. counterpart to the WisdomTree U.S. Quality Dividend Growth Fund (DGRW).

Historically, the dividend requirement has shifted DGRW toward value.

Internationally, the dividend requirement is a less restrictive filter on a starting investment universe, as there are fewer mega-cap non-dividend payers like Amazon, Tesla or Netflix. Consequently, DNL's profitability and growth screens naturally tilted it toward growth characteristics, creating a mismatch with the more value-oriented U.S. approach.

To better capture the growth segment DNL was already aligned with, and create an international complement to the WisdomTree U.S. Quality Growth Fund (QGRW), the updated Index now:

Source: WisdomTree

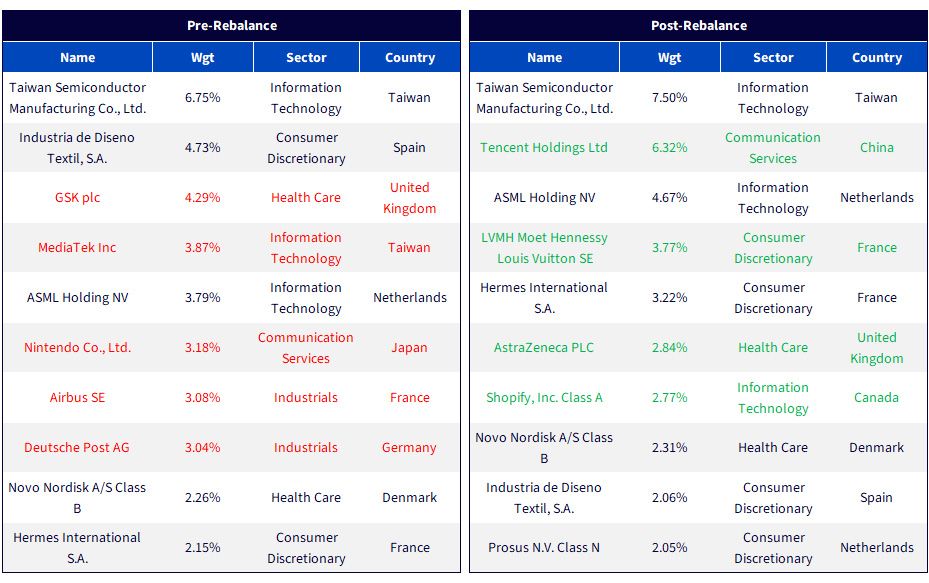

Five of the prior top 10 holdings were dropped, replaced by four new entrants. Notably, Shopify, the Canadian e-commerce leader, was added to the top 10 and is one of the few that does not pay a dividend.

Source: WisdomTree. Pre-Rebalance is the WisdomTree Global ex-U.S. Quality Dividend Growth Index as of 9/30/25. Post-Rebalance is the WisdomTree Global ex-U.S. Quality Growth Index as of the 9/30/25 screening date. You cannot invest directly in an index.

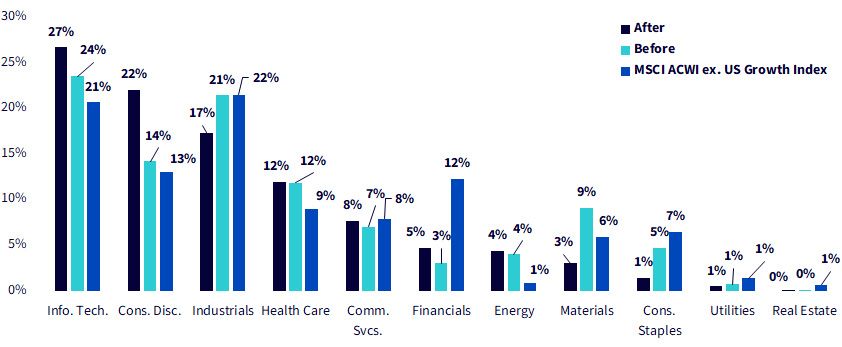

The higher beta observed (1.11) is reflected in over-weight allocations in the more volatile Consumer Discretionary (+10%) and Information Technology (+6%) sectors, and a 5% under-weight in the low-vol Consumer Staples sector.

Consistent with the previous methodology, the Index remains under-weight in Financials (~7%). The return-on-assets screen continues to penalize the highly levered banking sector that heavily populates ex-U.S. markets.

Sources: WisdomTree, MSCI, as of 9/30/25. Before is the WisdomTree Global ex-U.S. Quality Dividend Growth Index as of 9/30/25. After is the WisdomTree Global ex-U.S. Quality Growth Index as of the 9/30/25 screening date. You cannot invest directly in an index.

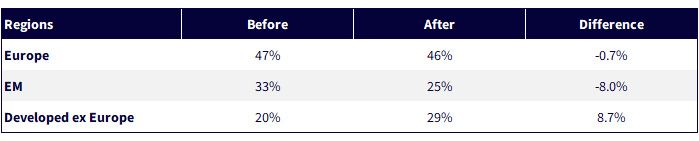

A unique enhancement of the new methodology is regional scoring and selection within defined geographic segments. This adjustment brings regional allocations closer to the underlying market-cap universe.

Regional exposures after the rebalance:

Sources: WisdomTree, FactSet. Before is the WisdomTree Global ex-U.S. Quality Dividend Growth Index as of 9/30/25. After is the WisdomTree Global ex-U.S. Quality Growth Index as of the 9/30/25 screening date. You cannot invest directly in an index.

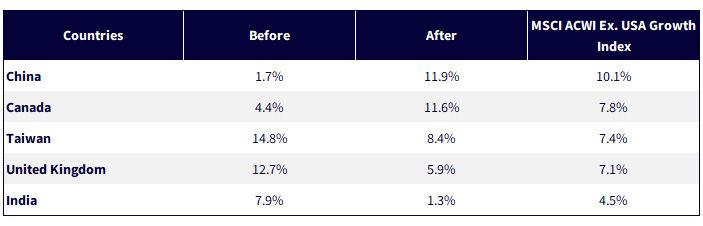

Top country exposure changes after the rebalance:

Sources: WisdomTree, FactSet, MSCI, as of 9/30/25. Before is the WisdomTree Global ex-U.S. Quality Dividend Growth Index as of 9/30/25. After is the WisdomTree Global ex-U.S. Quality Growth Index as of the 9/30/25 screening date. You cannot invest directly in an index.

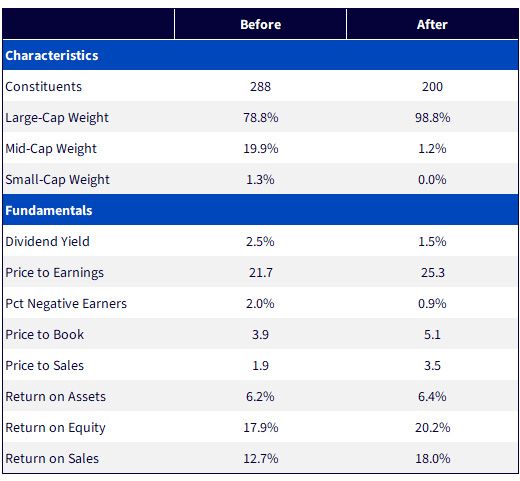

The updated methodology focuses on a narrower, higher-quality set of 200 large-cap growth companies drawn from a broader global universe, unconstrained by the dividend requirement.

Key Takeaways:

Sources: WisdomTree, FactSet. Before is the WisdomTree Global ex-U.S. Quality Dividend Growth Index as of 9/30/25. After is the WisdomTree Global ex-U.S. Quality Growth Index as of the 9/30/25 screening date. You cannot invest directly in an index.

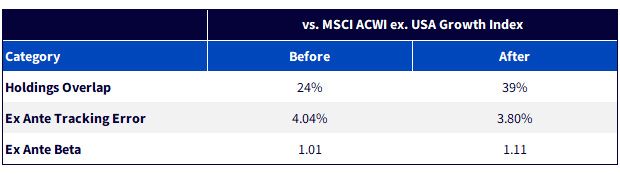

Following the rebalance, the WisdomTree Global ex-U.S. Quality Growth Index shows a 15% higher holdings overlap with the MSCI ACWI ex-USA Growth Index. This results in a lower ex ante tracking error and a beta of 1.11, aligning DNL more directly with global growth benchmarks.

Sources: WisdomTree, MSCI, as of 9/30/25. Before is the WisdomTree Global ex-U.S. Quality Dividend Growth Index as of 9/30/25. After is the WisdomTree Global ex-U.S. Quality Growth Index as of the 9/30/25 screening date. You cannot invest directly in an index.

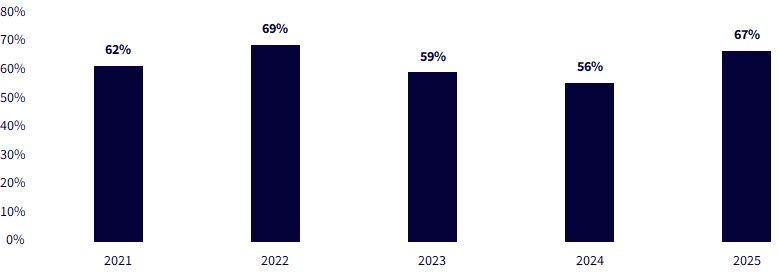

Turnover for this year's rebalance was 67% (one-way)—up 11 percentage points from 2024, but in line with levels seen between 2021 and 2022.

Source: WisdomTree. Rebalance turnover of the WisdomTree U.S. Quality Dividend Growth Index

With this evolution, DNL transitions from a dividend-driven framework to a pure quality growth strategy.

By aligning with the U.S. Quality Growth framework, DNL will soon offer investors a cohesive global quality growth solution—balancing strong fundamentals, consistent profitability and exposure to the world's leading growth franchises outside the United States.

This repositioning strengthens DNL's relevance for investors seeking long-term capital appreciation through a disciplined, fundamentals-based approach to quality and growth.

There are risks associated with investing, including the possible loss of principal.

DNL: Growth stocks, as a group, may be out of favor with the market and underperform value stocks or the overall equity market. Growth stocks are generally more sensitive to market movements than other types of stocks. The Fund is non-diversified; as a result, changes in the market value of a single security could cause greater fluctuations in the value of Fund shares than would occur in a diversified fund. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. To the extent the Fund invests a significant portion of its assets in securities of companies of a single country or region, it is more likely to be impacted by events or conditions affecting that country or region. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit. The Fund does not attempt to outperform its Index or take defensive positions in declining markets, and the Index may not perform as intended.

QGRW: Growth stocks, as a group, may be out of favor with the market and underperform value stocks or the overall equity market. Growth stocks are generally more sensitive to market movements than other types of stocks. The Fund is non-diversified; as a result, changes in the market value of a single security could cause greater fluctuations in the value of Fund shares than would occur in a diversified fund. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit. The Fund does not attempt to outperform its Index or take defensive positions in declining markets, and the Index may not perform as intended.

DGRW: Funds focusing their investments in certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time.

Please read each Fund’s prospectus for specific details regarding the Fund’s risk profile.

Director, Research

Matt Wagner joined WisdomTree in May 2017 as an Analyst on the Research team. He currently serves as a Director, where he supports the creation, maintenance, and reconstitution of WisdomTree’s indexes and actively managed ETFs. Matt began his career at Morgan Stanley, working as an analyst in Treasury Capital Markets from 2015 to 2017, focusing on unsecured funding planning, execution, and risk management. He graduated magna cum laude from Boston College in 2015 with a B.A. in International Studies, concentrating in Economics. In 2020, he earned a Certificate in Advanced Valuation from NYU Stern. He is also a Chartered Financial Analyst (CFA) charterholder.