DGRW

U.S. Quality Dividend Growth Fund

Published November 18, 2025

Global Head of Research

Equity Strategist

By late 2025, the story of U.S. equities is one of extraordinary strength layered atop growing unease. The S&P 500 Index has climbed to record highs, powered by an artificial intelligence (AI)-led rotation that continues to defy gravity. Even as breadth has narrowed, dominated by the Magnificent 71 and their ecosystem of semiconductor, cloud and infrastructure plays, the market's resilience has repeatedly confounded skeptics.

The U.S. economy has remained surprisingly robust, with gross domestic product (GDP) growth outpacing expectations, strong balance sheets and productivity narratives reinvigorated by generative AI. Yet, beneath the surface, cracks of valuation tension have widened. The largest companies now account for nearly a quarter of global equity market capitalization, trading at roughly 30 times earnings. This is expensive but still below the extremes of 1999. Investors face a strange duality: fundamentals that justify optimism, and valuations that whisper caution.2

The mood evokes the late-1990s, but with new specifics. Silicon Valley once again feels detached from economic gravity. AI has replaced the web browser as the object of collective belief and the capital intensity is staggering. Unlike the dot-com era's debt-fueled exuberance, today's build-out is equity-funded, led by profitable giants pouring hundreds of billions into data centers, chips and energy infrastructure.3 It is estimated that cumulative AI capex will get into the multi-trillions of dollars by decade's end, with hyperscalers' cash-to-asset ratios falling and corporate bond issuance surging.4 There are clear signs of circularity—Nvidia investing in OpenAI, which in turn spends on Nvidia chips via Oracle—but also tangible productivity gains and record free cash flow generation. It is, at least so far, a "rational bubble": participants know prices are high, yet remain willing buyers, believing the payoff of AI's transformation will arrive before the reckoning.5

The Market's Tension between Narrative and Math

What makes 2025 distinct is the uneasy coexistence of rational exuberance and cyclical memory. Advisors are actively rebalancing, trimming profits in tech, rotating into value and international equities, while private investors hesitate to step aside for fear of missing further upside.6 The macroeconomic data does not yet spell danger. Long-term earnings expectations hover near their historical averages, and initial public offering (IPO) activity remains muted. Yet, the psychology is textbook: professional managers afraid to underperform, private valuations untethered from profits and an ecosystem funding itself on belief. Whether this ends in catharsis or consolidation depends less on valuation ratios than on realized AI utility and sustained productivity spillovers. Until then, we inhabit the uncomfortable middle ground of an equity market that may not be in a bubble but certainly feels as though it's breathing its air.7

In a market defined by stretched multiples and optimism priced to perfection, investors need a framework that marries quality with valuation discipline. The WisdomTree U.S. Quality Dividend Growth Fund (DGRW) embodies that intersection. Built to track the WisdomTree U.S. Quality Dividend Growth Index, it selects companies through a rules-based lens emphasizing return on equity (ROE), return on assets and forward-looking earnings growth, metrics that speak directly to operational strength rather than hype. The Fund systematically filters out firms with unsustainable payout ratios and low-quality balance sheets, targeting the 300 U.S. companies best positioned for durable profitability and dividend expansion.

Crucially, DGRW introduces valuation sensibility through its dividend-weighted construction. Unlike market cap-weighted indexes that inflate exposure to the most expensive names, DGRW weights constituents by their indicated cash dividends, automatically tilting the portfolio toward companies that are returning capital to shareholders. In an environment where investors debate whether AI enthusiasm has crossed into bubble territory, DGRW offers an elegant middle ground: exposure to innovation through quality franchises, but with the humility of valuation discipline built in.

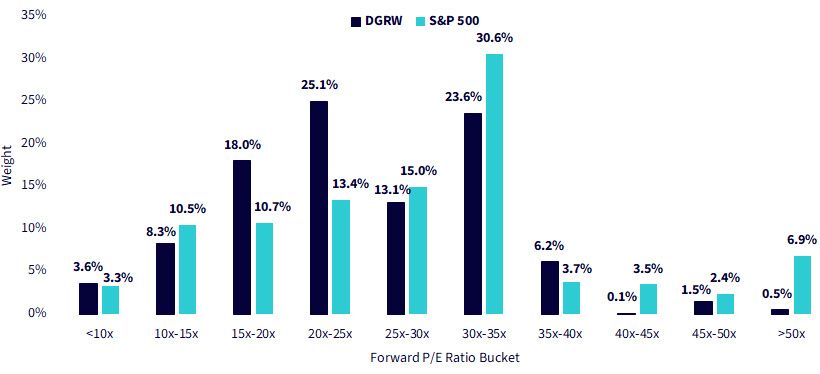

In figure 1, the valuation distribution underscores how DGRW's systematic process inherently reins in exposure to the most expensive corners of the U.S. equity market. By weighting stocks by their indicated dividend streams rather than market capitalization, DGRW naturally prioritizes companies where earnings power and shareholder return are in balance. In the chart, roughly 43% of DGRW's holdings trade between 15 and 25 times forward earnings, compared to just 24% for the S&P 500 Index, while about 2% of DGRW's weight resides in companies trading above 45 times earnings versus more than 9% for the S&P 500. That shift away from the upper valuation tail reflects more than index design, it's a structural bias toward durability over momentum, ensuring that capital isn't overconcentrated in the narrow band of ultra-high-multiple growth names currently dominating benchmarks.

The real power of this construction shows up when sentiment reverses. In periods when markets question stretched valuations, something that may ultimately happen with the AI story, DGRW's orientation toward moderate-multiple, high-profitability firms may provide ballast. This combination of valuation restraint and operational strength gives DGRW what you might call "quality convexity": upside participation when fundamentals drive returns, and downside resilience when exuberance fades. In a market that increasingly rewards discipline as much as innovation, that balance might be the defining advantage for the next phase of the cycle.

Figure 1: Quality at Reasonable Valuations

Sources: WisdomTree, FactSet, S&P. Data is as of 10/24/25. Subject to change.

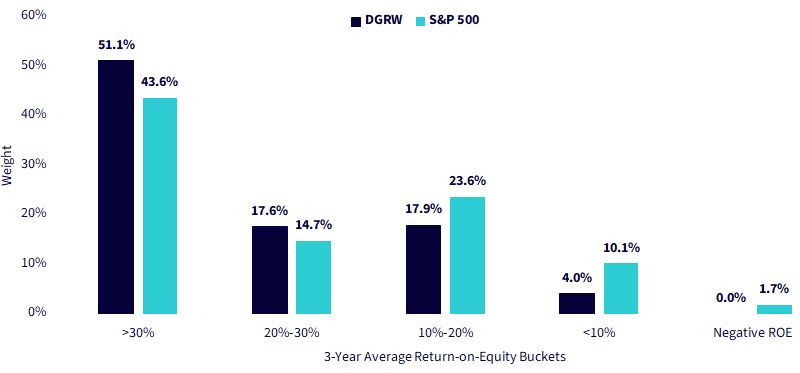

If valuation discipline defines how DGRW avoids overpaying, ROE defines why it still captures the right kind of growth. Figure 2 uses a three-year average ROE to illustrate how the Fund's methodology systematically channels capital toward companies that generate more profit per dollar of shareholder equity. Over 50% of DGRW's holdings exhibit ROEs above 30%, compared to about 44% in the S&P 500 Index. This distinction is crucial. It means the portfolio isn't simply chasing high dividend yields; it's allocating to businesses that consistently reinvest at superior rates of return, which is the hallmark of durable quality.

Figure 2: Proof of Quality: DGRW's Portfolio Skews toward Higher ROE Businesses

Sources: WisdomTree, FactSet, S&P. Data is as of 9/30/25. Subject to change.

Conclusion: Quality, Discipline and the Courage to Be Selective

In late 2025, investors face an environment defined by tension between belief in AI's transformative potential and the recognition that not every company can compound capital at the pace its stock price implies. The parallels to past bubbles are impossible to ignore. Yet, this time, the market also reflects a decade of balance-sheet repair and operational efficiency. The winners are real businesses with pricing power, free cash flow and durable profitability. That is precisely where DGRW plants its flag: in the intersection of innovation and prudence. Its systematic preference for high ROE and forward earnings growth ensures exposure to the companies driving technological progress, but with an embedded valuation anchor that tempers speculation.

Ultimately, DGRW represents more than a factor tilt. It's a philosophy of compounding under uncertainty. By emphasizing firms that generate superior profits on invested capital and reward shareholders through consistent dividends, DGRW channels market enthusiasm into disciplined ownership. When sentiment turns, it offers ballast by compounding when fundamentals drive returns. In a world where investors are once again asking whether we're in a bubble, DGRW provides a pragmatic answer: own quality, pay sensible prices, and let time, not speculation, do the heavy lifting.

1 Refers to Apple, Amazon.com, Alphabet, Meta Platforms, Microsoft, Nvidia and Tesla.

2 Source for paragraph: Goldman Sachs Global Investment Research, "Top of Mind: AI—In a Bubble?" Goldman Sachs Group, Inc., 10/22/25.

3 Source: R. Foroohar, "Silicon Valley Called—the 1990s Are Back: How Today's Artificial Intelligence Boom Is Both Different from, and Similar to, What Came Before," Financial Times, 10/26/25.

4 Source: Goldman Sachs Global Investment Research, 2025.

5 Source: J. Mackintosh, "Why Bubbles Can Keep Inflating in Plain Sight," The Wall Street Journal, 1024/25.

6 Source: N. Templin, "Worried about the AI Bubble? How to Stay Invested in Stocks without Getting Burned," Barron's, 10/25/25.

7 Source: Goldman Sachs Global Investment Research, 2025.

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

U.S. Quality Dividend Growth Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Equity Strategist

Brian Manby is an Equity Strategist at WisdomTree and part of the Investment Strategy team.

He is responsible for developing and communicating equity market insights, investment themes, and portfolio strategies that support the firm’s ETF and investment solutions platform. He evaluates sectors, valuations, fundamentals and equity styles to identify investment opportunities and provide actionable perspectives to clients and advisors. He also helps investors understand how WisdomTree’s equity strategies can be used to achieve long-term investment objectives in evolving market environments.

Brian joined WisdomTree in October 2018 as an Investment Strategy Analyst after a few years as a Consultant for FactSet Research Systems, Inc. He earned a B.A. in Economics and Political Science from the University of Connecticut in 2016 and has been a Chartered Financial Analyst since 2022.