DXJ

Japan Hedged Equity Fund

Published November 17, 2025

Global Head of Research

U.S. investors still can't ignore valuations—and Japan remains one of the most compelling global stories. After decades of caution, Japan's equity market combines reasonable valuations, reform-driven earnings and growing performance momentum. As U.S. equities remain richly priced, Japan stands out for its improving fundamentals, policy clarity and renewed corporate discipline.

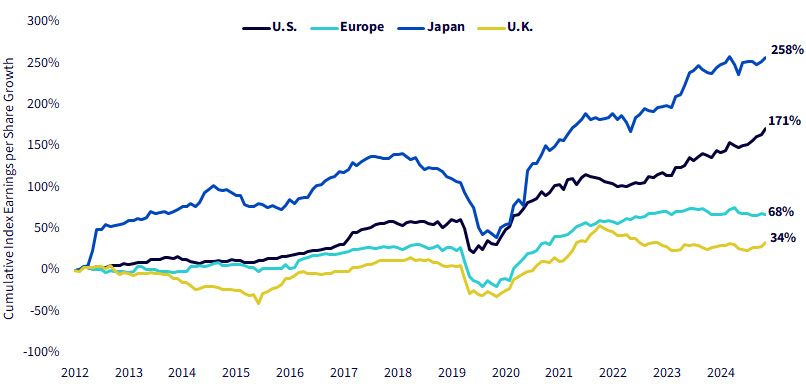

Few investors realize that Japan has been leading the developed world in corporate earnings growth. As we see in figure 1, over the past decade, Japanese companies have delivered 250% cumulative earnings-per-share (EPS) growth—outpacing the U.S., Europe and the U.K. This surge isn't driven by valuation multiples but by real profitability gains tied to governance reform, cost discipline and balance sheet efficiency.

Japan's corporate sector has quietly undergone a structural transformation—rewarding shareholders through buybacks, dividends and improved capital allocation. For investors still anchored to outdated views of Japan as stagnant, this chart tells a very different story: Japan Inc. has become a global earnings leader.

Figure 1: Surprise—Japan's Strong Earnings-per-Share Growth

Sources: WisdomTree, MSCI, 12/31/12–10/31/25. U.S., eurozone, Japan and U.K. measured by their respective country-specific MSCI indexes. Earnings per share growth measured in local currency terms. You cannot invest directly in an index.

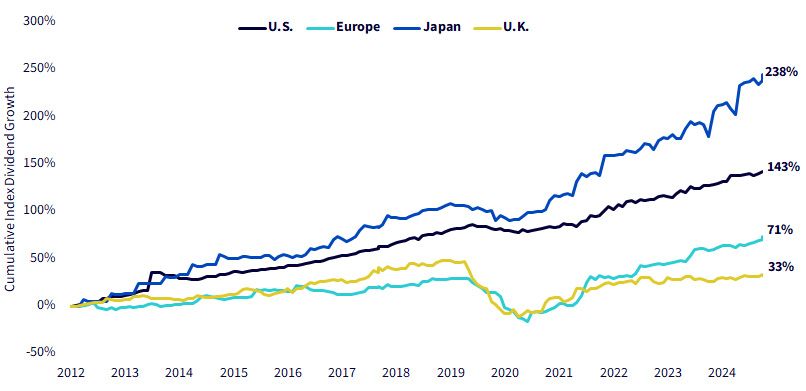

Japan's reputation as a low-dividend-yield, income-light market is becoming outdated. Over the past decade, Japanese companies have grown dividends by more than 200%, outpacing even the U.S. and far exceeding Europe and the U.K. This surge reflects corporate reforms—firms returning excess cash through buybacks and dividends as governance standards rise. What was once a market hoarding cash has become one actively rewarding shareholders. This represents disciplined capital deployment tied to profitability and efficiency. For investors seeking sustainable income growth, Japan has quietly transformed from dividend laggard to one of the most dynamic payout stories in the developed world.

Figure 2: Japan's Transformation for Dividend Growth Laggard to Leader

Sources: WisdomTree, MSCI, 12/31/2012–9/30/2025. U.S., eurozone, Japan and U.K. measured by their respective country-specific MSCI indexes. Earnings per share growth measured in local currency terms. You cannot invest directly in an index.

Japan is no longer the global laggard it once was. With attractive valuations, a reform-minded government and shareholder-friendly corporations, it offers both growth and resilience in a changing global cycle. For investors seeking disciplined exposure to this evolution, we believe Japan deserves a more strategic position at the heart of global equity portfolios.

For those looking to implement a Japan-focused equity strategy:

1 Source: Bloomberg. U.S. equities reference the S&P 500 Index, while Japanese equities reference the MSCI Japan Index. Data is as of 11/5/25.

2 Source: P. Chai, "Takaichi's Ambitious Economic and Security Agenda for Japan," The Diplomat, 10/29/25.

3 Source: T. Quinn, "Corporate Governance Reforms and Shareholder Value in Japan's Conglomerates: A New Era of Accountability," AInvest, 9/2/25.

4 Source: Markets Insider, "Japan's Stock Market Powers to a Fresh Record on a New Leader, but the Hype Could Fizzle Fast," Business Insider, 10/7/25.

DXJ/OPPJ: There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Investments in currency involve additional special risks, such as credit risk, interest rate fluctuations and derivative investments, which can be volatile and may be less liquid than other securities and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time.

Please read each Fund’s prospectus for specific details regarding the Fund’s risk profile.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.