DGRW

U.S. Quality Dividend Growth Fund

Published November 6, 2025

Global Head of Research

Macro Strategist, Model Portfolios

There is certainly not a shortage of risks for the equity markets. There are the seemingly constantly shifting tariff regimes, the security-driven industrial policy and a rapid retreat from globalization that could be more accurately described as supply-chain triage. In that mix, businesses that can protect margins, fund investments from cash flow and keep raising dividends despite the rapid shifts in policy could emerge as long-term winners. That's the core of dividend growth, and it's exactly what the WisdomTree U.S. Quality Dividend Growth Fund (DGRW) seeks to package by screening for quality and forward-looking earnings growth among U.S. dividend payers.1

Sometimes the geopolitically resilient companies are sitting in plain sight.

Home Depot might not seem like an example of resilience. Why? Because tariffs and trade frictions flow straight into the cost of fixtures, appliances, tools and flooring—exactly the categories HD and its pro customers live in. The latest tariff chatter out of Washington and Beijing has real pass-through and timing effects into inventory and price tags, and retailers have been bracing for that reality.2 HD's counter is a decade of supply-chain diversification and a heavy North American sourcing base, which management has highlighted as a buffer to tariff volatility.3 That's the playbook—de-risk concentration, keep shelves stocked and hold the line on price where you can.

There's another angle. HD's mix skews toward projects and professional spend that are less elastic than pure discretionary impulse purchases. If tariffs raise input costs, the company can work SKU-by-SKU4 with vendors, adjust specs and lean on its scale to avoid blunt-force price hikes. That's exactly how a quality operator preserves gross margin through policy shocks—by making a thousand small, operational decisions before customers feel a thing. For an investor, it's the repeatability that matters more than a single-quarter same-store sales comp. DGRW holds HD among its larger positions, which gives the Fund exposure to a tariff-sensitive name with the levers to manage it.5

Consumer staples are supposed to be boring. But the current policy tape makes them anything but dull. P&G6 is facing higher costs tied to tariff actions, and it has outlined selective mid-single-digit U.S. price increases to offset an expected ~$1 billion pre-tax tariff headwind in fiscal 2026.7 That's not great. But it is a reminder of why brand equity matters. When the policy environment raises your cost base, the ability to price, mix up and still hold market share is critical. P&G's update lands squarely in that "pricing power" capability bucket.

The policy landscape is not simply tariffs either. There is also the ever-evolving regulatory environment. The European Union's (EU's) new Packaging and Packaging Waste Regulation sets tougher rules on recyclability and reuse that will nudge packaging costs and design costs higher.8 Companies with scale, sophisticated procurement and agile research & development (R&D) are oddly advantaged. Policy risk is now a constant in global staples. PG is not immune, but the company has navigated these realities for decades and maintained a culture of payout growth.

Payments are "tech-adjacent," and that is an advantage for Visa. Similar to PG, though, it is not all about tariffs. For Visa, the harbinger of geopolitical risk was (and is) sanctions. Visa suspended operations in Russia in 2022—revenue you can't replace one-for-one, but a strategic (and legal) necessity when geopolitics redraws operating maps.9 On another front, European regulators continue to scrutinize scheme fees and interchange for competition and consumer impact, extending non-EU tourist fee caps and widening probes10—conditions that shape Visa's economics and product design across borders. It is exactly this dance—between policy and payments—that makes the payment rails resilient. Sometimes being highly regulated is an incumbent advantage.

There's also a competitive-policy layer playing out in Asia. India's UPI11 is expanding acceptance abroad and tightening local rules at home—innovation that lifts digital payments overall but can compress economics for global card networks at the margin. For a dividend-growth investor, the key is that Visa's cross-border volumes, travel recovery tailwinds and operating discipline have historically offset regional policy drags. DGRW's stake in Visa12 gives exposure to that global, policy-aware earnings engine—without buying a pure-play "tech" name.

One point often missed: "dividend growth" is not the same as "high dividend." The former is a quality-and-cash-flow story; the latter can be a leverage-and-cyclicality story. The underlying index methodology behind DGRW leans into profitability (think return on equity/return on assets) and estimated long-term earnings growth, which historically helps avoid value traps. As of mid-October, the portfolio's estimated P/E ratio (~21.5) sits a touch below the S&P 500 Index's forward P/E multiple,13 while still owning durable potential dividend growers—an attractive combination when multiples are stretched and policy is noisy. You're not trading out of growth; you're upgrading the balance between growth, quality and payout.

There's a portfolio-construction angle too. Today's mega-cap concentration means investors carry implicit factor and policy bets they may not realize. Rotating a sleeve from the highest-valuation cohort into dividend growers can reduce sensitivity to possible multiple compression while keeping exposure to firms with secular tailwinds—and with the cultural habit of returning more cash over time. It's a way to make room for uncertainty without abandoning equities.

Geopolitical risk is here to stay for investors. That argues for businesses that can navigate tariffs, regulation and cross-border complexity—all while returning cash to shareholders. Home Depot (tariff-aware supply chains), Procter & Gamble (pricing power brands) and Visa (resilient payment rails) are three examples. At the same time, starting valuations make a case to trim exposure to the highest-priced equities and reintroduce "paid-to-wait" into portfolios. Dividend growers won't eliminate volatility—but they can help convert more of it into compounding. In a world where policy is a persistent headwind and a periodic tailwind, that's a trade-off portfolios should consider.

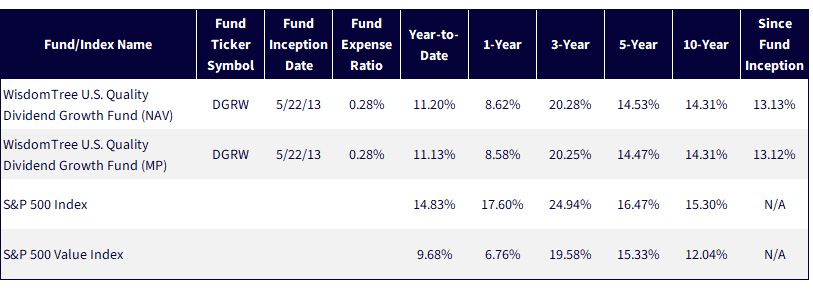

Sources: WisdomTree, FactSet; specifically, data from the Fund Comparison Tool in the PATH suite of tools, accessed 10/17/25, with returns as of 9/30/25. NAV denotes total return performance at net asset value. MP denotes market price performance. The performance data quoted represents past performance and is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click here.

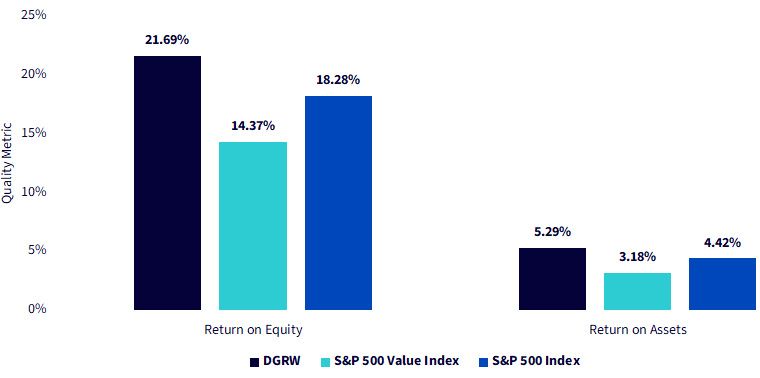

That quality bias shows up in the numbers. Dividend growers—represented here by DGRW—generate a return on equity north of 21% and a return on assets above 5%, outpacing both the S&P 500 and the S&P 500 Value Index. Those metrics speak to durable profitability and efficient capital allocation, the financial backbone that supports consistent dividend increases. In practical terms, these companies compound capital faster, cushion earnings shocks better and enter uncertain macro regimes with balance sheets built for optionality. It's a quiet but measurable edge in an environment where policy volatility and geopolitical noise can quickly turn "cheap" into "value traps."

Sources: WisdomTree, FactSet, with data as of 9/30/25.

1 DGRW is designed to track the total return performance, before fees and expenses, of the WisdomTree U.S. Quality Dividend Growth Index. The primary selection criteria for constituents in this Index include such attributes as strong return on equity, strong return on assets, lower leverage and strong earnings growth expectations.

2 Source: "U.S. retailers brace for impact as Trump's 100% China tariffs loom," Reuters, 10/13/25.

3 Source: "Q2 2025 The Home Depot Earnings Call Transcript," Home Depot Investor Relations, 8/19/25.

4 SKU is a "stock keeping unit," which is a unique alphanumeric identifier assigned to each distinct product and service that can be purchased. It's primarily used for inventory management, sales tracking and logistics.

5 As of 10/16/25, DGRW had a 2.57% weight in HD.

6 As of 10/16/25, DGRW had a 2.55% weight in P&G.

7 Source: "P&G Announces Fourth Quarter and Fiscal Year 2025 Results" [press release], The Procter & Gamble Company, 7/29/25.

8 Source: Packaging & Packaging Waste Regulation (PPWR), European Commission. (2025).

9 Source: "Visa suspends all Russia operations" [press release], Visa Investor Relations, 3/5/22.

10 Source: "EU widens probe into Visa and Mastercard fees," Reuters, 5/26/25.

11 Unified Payments Interface (UPI) is a real-time payment system developed by the National Payments Corporation of India (NPCI) and regulated by the Reserve Bank of India (RBI).

12 As of 10/16/25, DGRW had a 1.38% weight in Visa.

13 Source: Bloomberg, with data as of 10/16/25.

For current holdings of DGRW, please click here. Holdings are subject to risk and change.

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

U.S. Quality Dividend Growth Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.