DGRW

U.S. Quality Dividend Growth Fund

Published December 11, 2025

Director, Research

The rebalance of the WisdomTree U.S. Quality Dividend Growth Index ("the Index") went effective at the close of trading on Wednesday, December 10. This post highlights recent methodology enhancements, the main before-and-after changes to the Index and how the strategy is positioned heading into 2026.

The Investment Process

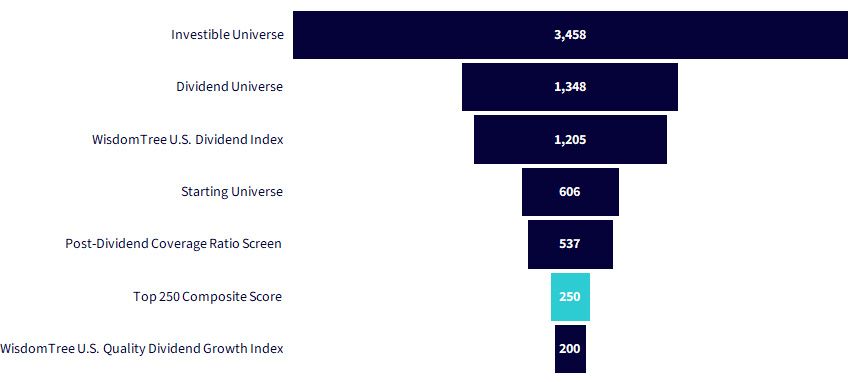

The Index follows a straightforward, rules-based process. The funnel chart below illustrates how the starting universe of more than 3,000 securities narrows to 200 final constituents.

Source: WisdomTree, as of 11/28/25. You cannot invest directly in an index.

WisdomTree builds its Indexes from the bottom up rather than starting from a benchmark like the S&P 500 or Russell 1000.

The investible universe is defined using information that includes country of exchange listing, market capitalization and liquidity requirements.

This year's universe included 3,458 securities, slightly broader than the Russell 3000.

Of the 3,458 securities, roughly 40% pay regular cash dividends.

A key differentiator for WisdomTree is that eligibility requires current dividend payments—not a long-term history of paying or growing dividends, as is common with other dividend growth methodologies.

The five biggest companies by market cap excluded on this screen: Amazon, Tesla, Berkshire Hathaway, Netflix, Palantir.

Five of the biggest companies to initiate a dividend in the last 24 months: Alphabet, Meta, Salesforce, Booking Holdings, GE Vernova.

The WisdomTree U.S. Dividend Index serves as the parent index for our domestic dividend strategies.

Of the 1,348 dividend-paying companies, 1,205 were included after applying the Composite Risk Screen (CRS), which removed 143 names.

The CRS helps mitigate exposure to value traps in dividend-weighted indexes by screening on profitability (within industry groups), risk-adjusted momentum and dividend yield (removing the riskiest, highest-yielding names).

Starting Universe for Quality Dividend Growth

The Quality Dividend Growth Index targets mid- and large-cap exposure.

Securities with less than $2 billion market capitalization and those included in the WisdomTree U.S. SmallCap Dividend Index are excluded.

This cutoff removes 599 companies, reducing the universe by about half.

The Index applies an additional filter to avoid companies with unsustainable dividends.

Firms with negative dividend coverage ratios (EPS < DPS) are excluded.

At this year's rebalance, this removed 69 companies.

Two methodology updates on the composite score were implemented at this year's rebalance:

From 537 eligible companies, the Index selects the 250 highest-scoring companies based on a 50% profitability score (three-year ROE and ROA) and a 50% growth score.

Another new methodology enhancement excludes the 50 smallest companies by weight after the top 250 are selected. The remaining constituents are then scaled to 100%.

Historically, this "bottom 100" tail represented only ~3% of total Index weight (about 3 bps per security). Removing these positions improves liquidity for investors and enhances investability without materially altering Index composition.

This rebalance also included the introduction of a new U.S. Dividend Index Committee, which serves as a sense check on the output of the rules-based process. The primary function of the Committee is to make sure the Index rules are implemented correctly and comprehensively, provided that the published Index composition shall be as determined by the Committee.

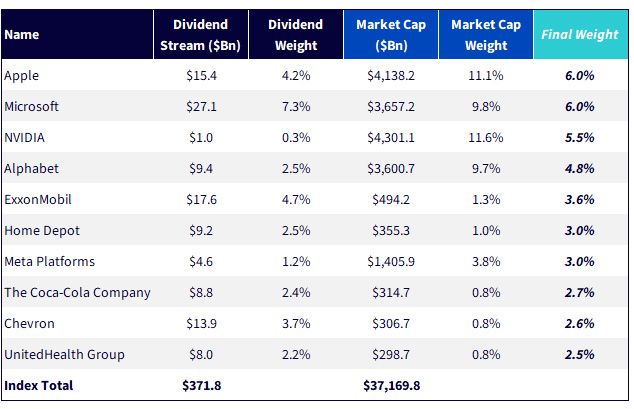

After selecting 200 companies, the Index weights constituents by Dividend Stream—the total cash dividends they pay.

Microsoft pays the largest dividend in the U.S., at $27 billion.

Of the $371.8 billion in total dividends across the 200 companies, Microsoft's dividend translates to a 7.3% weight.

To manage single-stock concentration, the Index Committee capped the top holdings at 6% this year. Additional adjustments were made to manage tracking error relative to core, value and dividend growth benchmarks, while maintaining valuation and dividend growth discipline.

2025 Rebalance: Top 10 Holdings

Source: WisdomTree, as of 11/28/25. You cannot invest directly in an index.

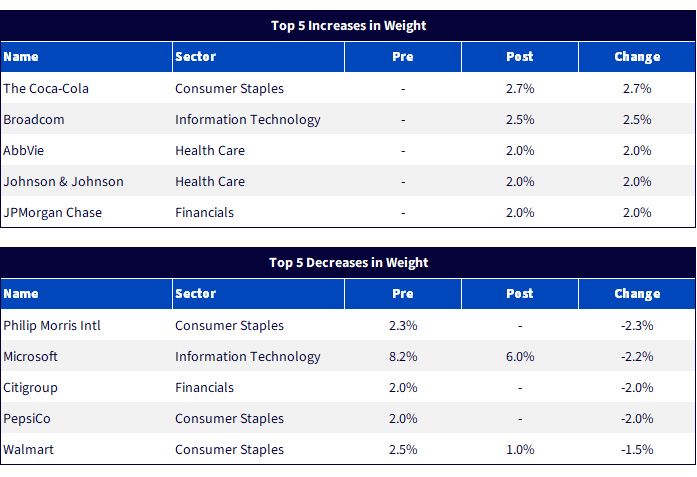

Single Stock Changes

The tables below highlight the largest weight changes at the rebalance.

Source: WisdomTree, as of 11/28/25. You cannot invest directly in an index.

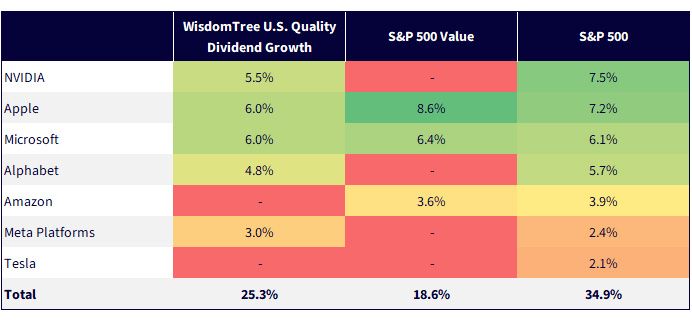

Given the strong performance of the "Mag 7" and their larger representation in the S&P 500, their weight within this Index is increasingly important. After the rebalance, the Index held 25% in the group—about 10% under-weight versus the S&P 500.

Mag 7 Exposure across Indexes

Source: WisdomTree, as of 11/28/25. WisdomTree U.S. Quality Dividend Growth Index represents the post-rebalance holdings. The rebalance was effective at the close of 12/10/25. You cannot invest directly in an index.

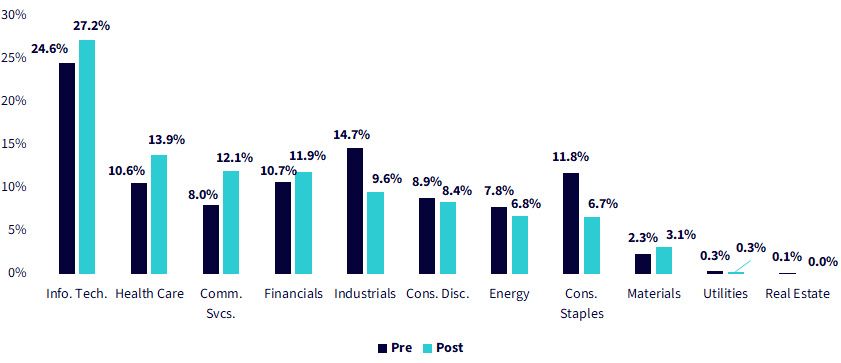

Four sectors saw notable shifts:

Source: WisdomTree, as of 11/28/25. Pre-/post-rebalance characteristics for the WisdomTree U.S. Quality Dividend Growth Index. The rebalance was effective at the close of 12/10/25. You cannot invest directly in an index.

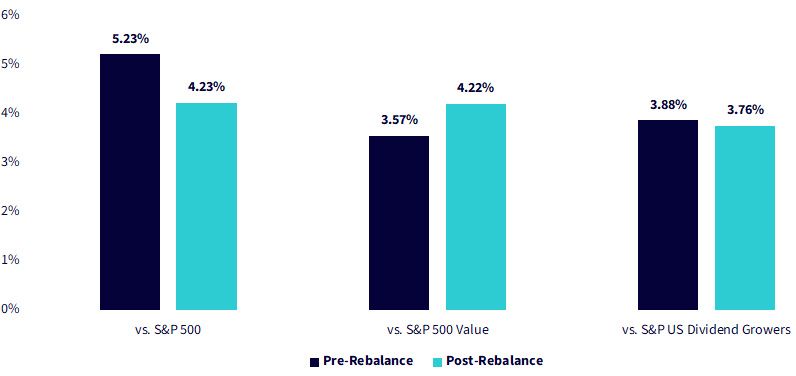

Rebalance changes contributed to:

In short, the Index reduced its tracking risk to the S&P 500 and modestly lowered tracking risk to a key dividend-growth benchmark, while continuing to exhibit the low-beta characteristics that have historically defined the strategy.

Sources: WisdomTree, FactSet, as of 11/28/25. Pre-/post-rebalance characteristics for the WisdomTree U.S. Quality Dividend Growth Index. The rebalance was effective at the close of 12/10/25. You cannot invest directly in an index.

Sources: WisdomTree, FactSet, as of 11/28/25. Pre-/post-rebalance characteristics for the WisdomTree U.S. Quality Dividend Growth Index. The rebalance was effective at the close of 12/10/25. You cannot invest directly in an index.

Heading into 2026: Lower Valuations, Higher Growth Potential

Post-rebalance characteristics highlight attractive fundamentals:

In today's environment—where investors are focused on valuations and the risks of a potential AI bubble—we see this fundamentals-driven approach as a compelling solution that maintains both profitability and growth while avoiding value traps.

This year's enhancements—including the refined growth composite, a more focused stock selection and the introduction of the Index Committee—underscore WisdomTree's commitment to improving index design and delivering a more consistent investor experience.

Source: WisdomTree, as of 11/28/25. WisdomTree U.S. Quality Dividend Growth Index represents the post-rebalance holdings. The rebalance was effective at the close of 12/10/25. You cannot invest directly in an index.

U.S. Quality Dividend Growth Fund

Director, Research

Matt Wagner joined WisdomTree in May 2017 as an Analyst on the Research team. He currently serves as a Director, where he supports the creation, maintenance, and reconstitution of WisdomTree’s indexes and actively managed ETFs. Matt began his career at Morgan Stanley, working as an analyst in Treasury Capital Markets from 2015 to 2017, focusing on unsecured funding planning, execution, and risk management. He graduated magna cum laude from Boston College in 2015 with a B.A. in International Studies, concentrating in Economics. In 2020, he earned a Certificate in Advanced Valuation from NYU Stern. He is also a Chartered Financial Analyst (CFA) charterholder.