OPPE

European Opportunities Fund

Published November 17, 2025

Global Head of Research

After a decade of muted growth and policy hesitation, Europe has reemerged as a dynamic force in global equity markets. Fiscal expansion, defense spending acceleration and monetary easing are converging to create, potentially, one of the most constructive European equity market backdrops in recent memory.1 The market's breadth, dividend strength and valuation support make it an increasingly strategic complement to U.S. equity exposure.

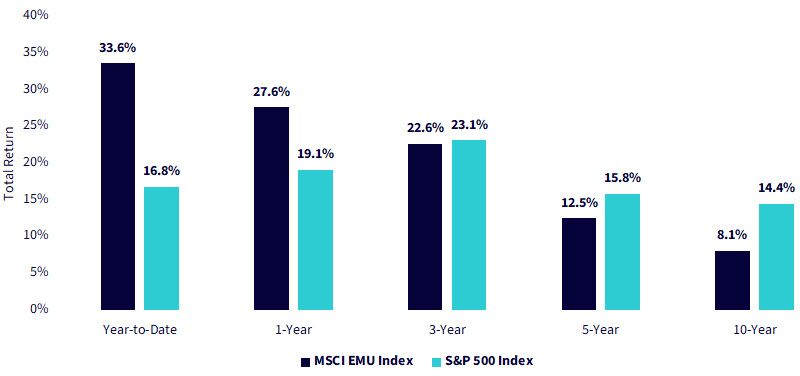

As we see in figure 1, European equities are showing clear momentum relative to U.S. markets. The MSCI EMU Index has delivered a 33.6% year-to-date gain, roughly double the S&P 500's 16.8%, marking a decisive shift in performance leadership. Over the past one and three years, Europe has also closed the return gap, supported by accelerating earnings revisions, monetary easing and fiscal tailwinds. This performance resurgence reflects more than short-term relief—it signals a durable recovery driven by industrial reinvestment, rising defense spending and strong dividend growth. After years of lagging the U.S., Europe's equity story is now one of cyclical strength reinforced by structural transformation.

Figure 1: European Equities Are Showing Clear Momentum Relative to U.S. Markets

Sources: WisdomTree, FactSet, Morningstar, with data as of 11/5/25. You cannot invest directly in an index.

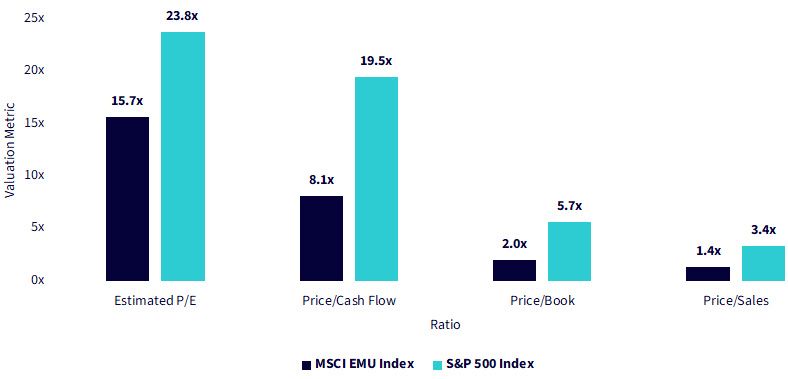

As seen in figure 2, European equities trade at a steep valuation discount to the U.S. The MSCI EMU Index commands just 15.7 times forward earnings versus 23.8 times for the S&P 500, with similarly lower ratios across cash flow, book value and sales. This wide gap highlights Europe's compelling relative value amid improving fundamentals and accelerating earnings momentum.

Sources: WisdomTree, FactSet, Morningstar, with data accessed as of 11/5/25, based on index constituents as of 9/30/25. For definitions of terms in the chart above, please visit the glossary. You cannot invest directly in an index.

Europe's story is no longer about survival—it's about competitive renewal. Fiscal stimulus, monetary normalization and industrial reinvestment have combined to reset the region's growth potential. For investors seeking cyclical leverage with structural support, Europe offers both value and velocity.

For those looking to express this view:

1 Sources: A. García-Serrador et al., "Europe | EU Priorities: Defence Spending & Multipliers," BBVA Research, 9/16/25; "Combined Monetary Policy Decisions and Statement," European Central Bank, 10/30/25.

2 Sources: "A Different Lens on Europe's Defence Budgets," McKinsey & Company, 2/12/25; "Time to Be Strategic: How Public Money Could Power Europe's Green, Digital and Defence Transitions," European Central Bank, 7/25/25.

3 Sources: R. Daugherty, "Why the Smart Money Is Moving to Europe – The Yield Curve Is Telling Us to Buy," Forbes, 6/11/25; S. Soubeyran, "Fixed Income Insights: Europe," London Stock Exchange Group, June 2025.

4 Source: Bloomberg, with data covering the 2025 year through 11/5/25.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty

HEDJ: Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time.

OPPE: There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. This Fund focuses its investments in Europe, thereby the impact of events and developments associated with the region can adversely affect performance. The securities of small-capitalization companies generally trade in lower volumes and are subject to greater and more unpredictable price changes than larger-capitalization stocks or the stock market as a whole. The Fund uses various strategies to attempt to minimize the impact of changes in the value of the euro against the U.S. dollar and these strategies may not be successful. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs.

Please read each Fund’s prospectus for specific details regarding the Fund’s risk profile.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.