EUDG

Europe Quality Dividend Growth Fund

Published July 16, 2026

Global Head of Research

Those not directly studying Europe may miss an array of dynamic stories:

The WisdomTree Europe Quality Dividend Growth Fund (EUDG) provides a lens through which these narratives become visible. None of them depend on the export story, and each stands on its own.

Rearmament: Europe's Once-in-a-Generation Defense Spending Cycle

Perhaps no theme in European equities is more consequential or more misunderstood by investors anchored to older mental models than the continent's rearmament cycle. For most of the post-Cold War era, European NATO1 members treated defense as a budget line to be managed downward. The 2014 Wales Summit commitment to spend 2% of gross domestic product (GDP) on defense was widely ignored, and in that year, only three of the alliance's members met the target.2

That era is over. At the 2025 NATO Summit in The Hague, 31 of 32 member states committed to raising defense and security-related expenditure to 5% of GDP by 2035, and The commitment includes a two-tiered structure requiring at least 3.5% for core military expenditures and up to 1.5% for adjacent security domains including cyber, critical infrastructure, and defense innovation.3 In 2025, for the first time in recorded NATO history, every single ally met or exceeded the 2% threshold. European allies and Canada collectively increased defense spending by 20% in real terms versus 2024, investing a combined $574 billion. Between 2014 and 2025, European NATO members more than doubled their annual defense expenditure in real terms, a 106% increase.4

The numbers at the country level are equally striking.5

This is not cyclical procurement; it is a structural, multi-decade spending commitment mandated by geopolitical necessity and formalized in treaty.

EUDG's holdings translate this macro commitment into identifiable corporate beneficiaries. Rheinmetall, the German defense and technology group, reported 2025 defense sales of €9.9 billion, up 29% year-on-year, with an operating profit of €1.84 billion, up 33%, and a record order backlog of €63.8 billion, itself up 36% from the prior year. The company is guiding for revenue of €14 billion to €14.5 billion in 2026, representing growth of up to 45%, and expects its backlog to more than double to €135 billion by year-end.6 BAE Systems, Rolls-Royce, Thales, Safran, Leonardo, Kongsberg, Dassault Aviation, Saab, and Hensoldt round out a cluster of EUDG holdings that collectively span land systems, aerospace propulsion, naval platforms, electronic warfare, and space, the full domain architecture that European governments are now committed to rebuilding.7

What makes this theme unusual, and unusually durable, is its source of funding. Government defense budgets, once committed at the political level, are among the most predictable revenue streams in industrial history. Order backlogs of the scale now accumulating at Rheinmetall and its peers do not evaporate with a change in consumer sentiment or a turn in the inventory cycle. They tend to convert into revenue over years and decades.

Healthcare: A Continent That Punches Above Its Weight in Drug Development

The global pharmaceutical industry's most discussed story of the past five years, specifically, the GLP-1 revolution in obesity and diabetes care, has a Danish postcode. Novo Nordisk, the Copenhagen-based manufacturer of Ozempic and Wegovy, reported 2025 sales of its obesity care products at DKK 82.3 billion (approximately $12.5 billion), while Ozempic, its semaglutide treatment for type 2 diabetes, generated a further DKK 127 billion (approximately $19.3 billion), reflecting the breadth of the franchise across two major indications. Novo held a 59.6% branded volume market share of the global GLP-1 obesity market in 2025, in a category that saw 104% volume growth year-on-year.8

Novo Nordisk does not stand alone in EUDG's healthcare cluster.9

Europe's healthcare sector, taken in aggregate, is not a follower of American pharmaceutical innovation. Rather, it is one of its primary sources.

Banking: A Sector Repriced for a World That No Longer Has Zero Interest Rates

For roughly a decade beginning in June 2014, the European Central Bank's negative interest rate policy compressed the net interest margins of European banks, particularly deposit-reliant retail banks, creating persistent headwinds for profitability across the sector.11 Many investors absorbed that experience as a permanent feature of European banking and wrote the sector off accordingly. The rate environment has fundamentally changed, and so has the earnings picture.

The European Central Bank's May 2026 Financial Stability Review reported that euro area banks delivered return on equity levels averaging close to 10% in 2025.12

EUDG's banking exposure is varied:

The latter two are not conventional additions to a European equity fund. They represent exposure to economies that have been growing at rates more commonly associated with emerging Asia, served by banks with dominant domestic market positions and returns on equity well above the European average.

Infrastructure and Industrials: Europe Rebuilding Its Own Productive Capacity

Two related themes in EUDG that often go unnoticed by investors scanning for the headline names deserve attention:

Energy

On the energy side, SSE and RWE are utilities anchored to Europe's renewable infrastructure buildout, which includes wind, solar, grid storage, and transmission.

Prysmian and Nexans manufacture the high-voltage cables through which renewable electricity travels from generation to consumption; both have multi-year order books tied to offshore wind interconnection and grid expansion programs across the continent.

Rexel distributes electrical equipment to the installers and contractors who physically build out that infrastructure at the last mile.

These are not glamorous businesses, but they are embedded in one of the most capital-intensive and government-supported long-cycle spending programs in Europe's post-war economic history.

Selection of Scandinavian and British Industrials

The Scandinavian and UK precision industrial cluster in EUDG is equally distinctive.

Atlas Copco, Sandvik, Epiroc, and Konecranes are Swedish and Finnish companies with global leadership positions in compressors, cutting tools, mining equipment, and industrial cranes respectively, categories where switching costs are high, aftermarket service revenues are durable, and margins reflect genuine technological differentiation.

Halma, Spirax-Sarco, IMI, and the Weir Group add UK engineering depth across safety systems, steam engineering, flow control, and mining services.

These companies rarely appear in discussions of European equity opportunity, but their financial characteristics, which include consistent returns on capital, recurring revenue streams, and disciplined capital allocation, are exactly what quality-oriented investors tend to seek.

Two Lenses, One Continent

EUDG, based on its underlying exposure, connects investors to Europe's own internal inflection, a continent that is simultaneously rearming, repricing its financial sector, reinvesting in its energy grid, and home to some of the world's most durable pharmaceutical and industrial franchises.

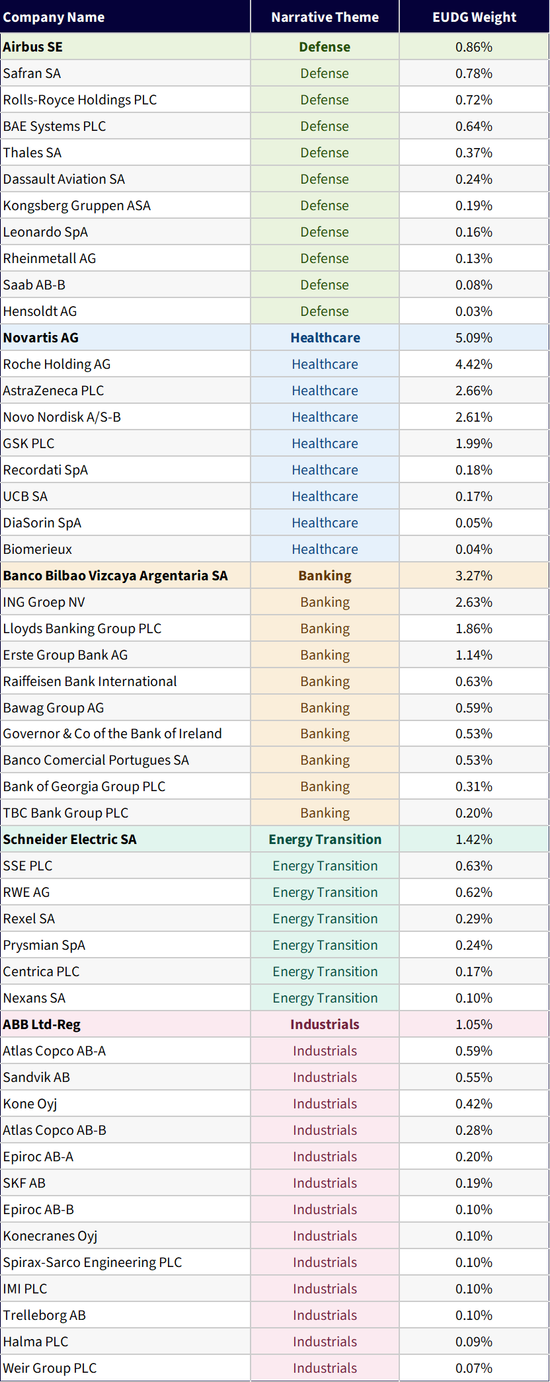

Figure 1: EUDG Weights of Companies Mentioned

Source: WisdomTree, specifically the EUDG fund page with holdings and weights as of June 26, 2026. For current holdings of EUDG, please click here. Holdings are subject to risk and change.

1 North Atlantic Treaty Organization.

2 Source: North Atlantic Treaty Organization. (2026, April 10). Defense expenditures and NATO's 5% commitment.

3 Source: North Atlantic Treaty Organization. (2026, April 10). Defense expenditures and NATO's 5% commitment.

4 Source: Rutte, M. (2026, March 26). NATO Secretary General's annual report 2025 [Press release]. North Atlantic Treaty Organization.

5 Source: Clapp, S. (2026, March 9). EU member states' defense budgets. European Parliamentary Research Service, European Parliament.

6 Sources: Rheinmetall AG. (2026, March 11). Financial report: Figures FY 2025 — Rheinmetall on course for success [Press release]; Rheinmetall AG. (2026, May 7). Financial report for Q1 2026 — profitable growth and full order books [Press release].

7 Source: WisdomTree, with specific company exposures in EUDG shown in Figure 1. Holdings subject to change.

8 Source: Novo Nordisk A/S. (2026). Financial performance: 2025 performance and 2026 outlook. Novo Nordisk Annual Report 2025.

9 Source: WisdomTree, with specific company exposures in EUDG shown in Figure 1. Holdings subject to change.

10 Sources: AstraZeneca PLC. (2026, February 10). AstraZeneca results: FY and Q4 2025 [Press release]; Drug Discovery & Development. (2025, June 10). Pharma 50: The top pharma companies in the world for 2025.

11 Source: Lane, P. R. (2020, August 26). Going negative: The ECB's experience [Speech]. European Central Bank.

12 Source: European Central Bank. (2026, May 27). Financial stability review, May 2026.

13 Source: Lloyds Banking Group PLC. (2026, January 29). 2025 results [News release].

14 Source: European Banking Authority. (2026). Q4 2025 risk dashboard [Press release].

15 Sources: TBC Bank Group PLC. (2026, February 20). 4Q 2025 results presentation [Investor presentation]; Bank of Georgia Group PLC. (2026, February 25). 4Q 2025 results [Earnings release].

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. This Fund focuses its investments in Europe, thereby increasing the impact of events and developments associated with the region which can adversely affect performance. Growth stocks, as a group, may be out of favor with the market and underperform value stocks or the overall equity market. Growth stocks are generally more sensitive to market movements than other types of stocks. Dividends are not guaranteed and a company currently paying dividends may cease paying dividends at any time. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.