WDEF

Europe Defense Fund

Published July 9, 2026

Global Head of Research

Secretary of Defense Pete Hegseth was in Singapore on May 30, 2026, visiting what has become one of the world's most consequential diplomatic venues. His message, specifically that the United States, Japan, and South Korea are "deepening our defense cooperation to ensure our combined forces remain lethal, ready, and capable of deterring aggression in the region," was brief even by the standards of an X post.1 But for anyone paying attention to the industrial base supporting these political declarations, but the implications were anything but brief.

Most American investors understand the geopolitical tension in the region in broad strokes.

What often gets lost is the connection between these abstract tensions and the companies actually building the hardware, the software, and the integrated systems that deterrence depends on. The gap between "understanding the headlines" and "understanding who benefits" is precisely where investment insight lives.

Intensifying Trilateral Coordination

The Hegseth meeting in Singapore was not a standalone moment. It capped months of intensifying trilateral coordination. In May 2026, the U.S. and South Korea held their Korea-U.S. Integrated Defense Dialogue, with Secretary Hegseth welcoming Seoul's commitment to raising defense spending, including a proposed 8.2% increase, and explicitly praising South Korea's shipbuilding capabilities as essential to keeping U.S. naval assets ready for any contingency.2

In January 2026, the U.S. and Japan were already advancing what has been branded "USFJ 2.0," a structural overhaul of U.S. Forces Japan into a joint operational headquarters capable of coordinating real warfighting, not just exercises.3 Extended deterrence dialogues, force posture reviews and technology transfer frameworks—in effect, the bureaucratic scaffolding of alliance deepening was being erected rapidly, with increasing urgency.

None of this happens without the companies that make it real. Defense spending translates into contracts. Contracts translate into revenue. And revenue, for the publicly traded firms embedded in Asia's defense ecosystem, translates into earnings growth over a duration that is measured in decades, not quarters. The WisdomTree Asia Defense Fund (WDAF) holds a carefully constructed portfolio of these firms. Five of them, drawn from across the fund's holdings, illustrate just how broad and structurally important this investment universe has become.4

Hindustan Aeronautics Limited — India's Air Power Engine (7.75% weight)

Hindustan Aeronautics Limited, better known as HAL, is the state-owned but publicly listed backbone of India's indigenous aerospace and defense manufacturing capability. HAL designs, develops, manufactures, and overhauls military aircraft, helicopters, aero-engines, avionics, and spacecraft. Its product lineage includes the Tejas light combat aircraft, which is India's answer to dependence on imported fighter aircraft, as well as the Dhruv advanced light helicopter and a growing partnership with foreign original equipment manufacturers transferring technology into India's industrial base.

India's defense modernization story is one of the defining investment narratives of this decade. The government's push for "Atmanirbhar Bharat", meaning ‘self-reliant India,’ has translated into explicit procurement policies favoring domestic manufacturers.5 HAL is the prime beneficiary. Orders for additional Tejas squadrons, helicopter procurement for the Navy and Army, and an ambitious pipeline of next-generation development programs give HAL a backlog that extends well into the 2030s. As India navigates its relationships with Western partners while managing tensions with China across a disputed Himalayan border, the political will sustaining HAL's order book is not a policy preference. It is a national security imperative.

Hyundai Rotem — The Land Warfare Specialist (7.03% weight)

While much of the attention in Asian defense focuses on naval and air assets, the ground warfare domain is experiencing its own quiet renaissance, and Hyundai Rotem is at the center of it. A subsidiary of the Hyundai Motor Group, Rotem is South Korea's preeminent manufacturer of main battle tanks, armored vehicles, and railway systems. Its K2 Black Panther main battle tank is widely regarded as one of the most capable platforms in the world, combining an advanced powerpack, an active protection system, and sophisticated fire control into a package that has drawn confirmed export orders from Poland, where a framework agreement envisions up to 1,000 tanks, and serious evaluation interest from across Europe. Poland signed its first executive contract for 180 K2 tanks in 2022, valued at $3.7 billion, and followed with a second deal in August 2025 worth approximately $6.5 billion, with full-scale domestic production of a Polish-configured variant scheduled to begin in 2026.6

The K2's export success is itself a signal. European nations, shaken by the war in Ukraine into reconsidering their land warfare capacity, have looked to South Korea's mature and cost-competitive defense industrial base as an alternative to domestic production timelines that stretch years longer. For Hyundai Rotem, this means the demand signal is no longer purely regional. And domestically, South Korea's stated ambition to assume wartime operational command, reducing the leading role of U.S. forces on the peninsula, means Seoul needs to fund and field the ground capabilities that would underpin that command. Hyundai Rotem is a direct expression of that budget.

Mitsubishi Heavy Industries — Japan's Industrial Rearmament (3.55% weight)

No single company embodies the transformation of Japan's defense posture more completely than Mitsubishi Heavy Industries. For decades, Japan's pacifist constitutional constraints kept its defense industrial base in a deliberate state of underutilization. That era is over. Japan has committed to doubling its defense budget to 2% of gross domestic product (GDP) by fiscal year 2027, the most significant reorientation of Japanese defense spending since World War II,7 and MHI is at the center of this tidal shift. Japan has already reached this target.

MHI builds submarines, destroyers, fighter aircraft, missiles, and space launch systems. It has been awarded contracts for hypersonic weapon development and is deeply embedded in the missile defense architecture protecting Japan's southwestern islands, the chain running toward Taiwan that has become some of the most strategically contested geography on Earth. The USFJ 2.0 initiative to upgrade allied command-and-control architectures creates operational demand for exactly the kind of integrated platforms and systems that MHI provides. When Hegseth and Japanese Defense Minister Koizumi agreed in Singapore to advance cooperation "with a sense of urgency and speed," those are words that eventually show up in MHI's order intake.8

DroneShield — The New Warfighting Domain (2.73% weight)

Not every critical defense capability comes wrapped in steel plating and measured in displacement tonnage. DroneShield, an Australian company listed on the ASX, is building what may be the defining defensive technology of this era, which develops systems that detect, track, and neutralize unmanned aerial systems. The proliferation of commercial drones as weapons, demonstrated dramatically in Ukraine but equally relevant across every potential theater of conflict in Asia, has created an urgent and rapidly expanding market for counter-UAS capabilities.

Singapore Technologies Engineering — The Integrator's Integrator (4.46% weight)

Singapore's strategic geography, sitting astride the Malacca Strait, the world's most critical maritime chokepoint, has always made defense a matter of existential seriousness for the city-state. ST Engineering is the institutional expression of that seriousness, a defense and engineering conglomerate with capabilities spanning aerospace MRO (maintenance, repair, and overhaul), naval systems, land systems, cybersecurity, smart city infrastructure, and satellite communications.

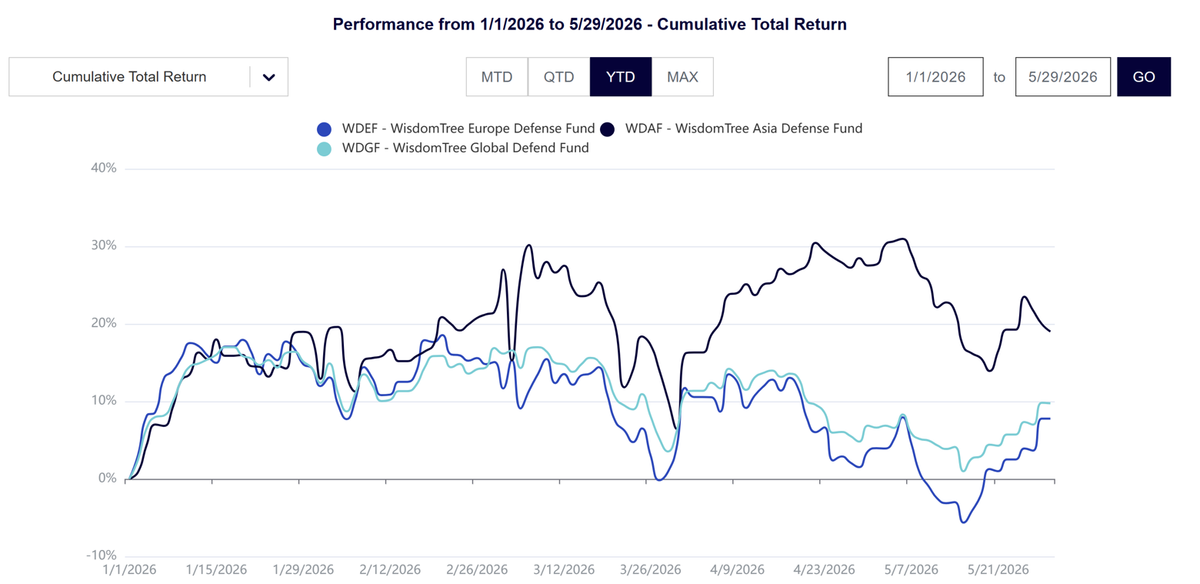

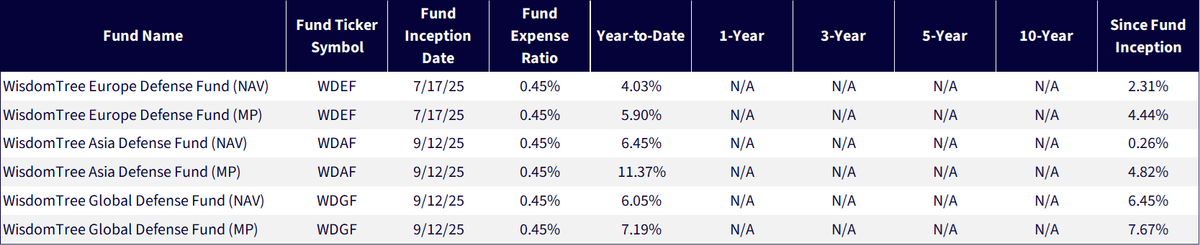

Conclusion: How Asia Defense is Stacking up in 2026 vs. Other Regionally-Focused Defense Strategies

In 2025, WisdomTree launched a suite of regionally-focused defense strategies:

Having these strategies allows us to gauge the response, by way of market performance, that is transmitting through global equities. Anyone doing research on different defense equities could learn from which regions are leading or lagging over different periods, and we look forward to having a longer live track record.

For the first five months of 2026, it’s clear that volatility was the rule overall, but also that WDAF was the leader. We would note that any time someone is thinking of the U.S. versus China geopolitical tension, they might also benefit from considering this specific angle where we see U.S. allies strengthening their defense capabilities, thereby engaging in business opportunities with specific companies.

Figure 1a: First Five Months of Performance in 2026

Figure 1b: Standardized Performance

Sources: Morningstar, FactSet and WisdomTree. Specifically, the data are from the PATH Fund Comparison Tool, accessed as of May 31, 2026, but showing returns for the period ended May 29, 2026 for Figure 1a and March 31, 2026 for Figure 1b. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: WDEF, WDAF, WDGF.

1 Source: Bloomberg News. (2026, May 30). Hegseth says US to deter regional aggression with Japan, Korea. Bloomberg.

2 Source: Vandiver, J. (2026, May 12). Pentagon talks include South Korea taking wartime command of allied forces. Stars and Stripes.

3 Source: Gordon, C. (2026, January 16). US-Japan defense chiefs vow to strengthen alliance. Air & Space Forces Magazine.

4 Source for weights and holdings is the WDAF fund page, as of May 29, 2026. Holdings subject to change.

5 Source: Invest India. (n.d.). Defence manufacturing. Government of India.

6 Sources: Defence Industry Europe. (2025, November 14). South Korea's Hyundai Rotem concludes deliveries of 180 K2 main battle tanks to Poland; Army Recognition. (2025, August 24). Exclusive: South Korea plans K2 tank production hub in Poland for European market.

7 Source: Nippon.com. (2026, January 17). Japan targets 2% defense spending.

8 Source: Ministry of Defense Japan. (2026, May 30). Japan-U.S. defense ministerial meeting (summary).

There are risks associated with investing, including potential loss of principal. Foreign investing involves specific risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Please read each Fund’s prospectus for specific details regarding the Fund’s risk profile.

WDAF: Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Because the Fund invests primarily in the securities of companies in Asia, the Fund’s performance is expected to be closely tied to social, political, and economic conditions within Asia and to be more volatile than the performance of more geographically diversified funds. Many countries in the region have historically faced political uncertainty, corruption, military intervention, and social unrest. To the extent that such events continue in the future, they can be expected to have an unpredictable effect on economic and securities market conditions in the region and may impact the ability of the Fund to buy, sell or otherwise transfer securities and cause the Fund to decline in value. Investments in non-U.S. securities involve political, regulatory, and economic risks that may not be present in investments in U.S. securities. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit. The Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended.

WDEF: This Fund focuses its investments in Europe, thereby increasing the impact of events and developments associated with the region which can adversely affect performance. A Fund focusing its investments on certain sectors and/or regions increases its vulnerability to any single economic or regulatory development. This may result in greater share price volatility. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended.

WDGF: To the extent the Fund invests a significant portion of its assets in securities of companies of a single country or region, it is more likely to be impacted by events or conditions affecting that country or region. Investments in non-U.S. securities involve political, regulatory, and economic risks that may not be present in investments in U.S. securities. Investments in non-U.S. securities may be subject to risk of loss due to foreign currency fluctuations, political or economic instability, or geographic events that adversely impact issuers of foreign securities. Investments in non-U.S. securities also may be subject to withholding or other taxes and may be subject to additional trading, settlement, custodial, and operational risks. These and other factors can make investments in the Fund more volatile and potentially less liquid than other types of investments. These risks may be heightened to the extent the Fund invests in companies domiciled in or otherwise tied to developing or emerging market countries. The Fund invests in the securities included in, or representative of, its Index regardless of its investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.