OPPJ

Japan Opportunities Fund

Published May 27, 2026

Global Head of Research

The question is no longer whether Japan is interesting. It is whether investors are positioned to capture it in a way that reflects how the opportunity has actually evolved.

That is exactly what the WisdomTree Japan Opportunities Fund (OPPJ) was designed to do.

A New Japan: From Deflation to Structural Reflation

The most important single shift in Japan today is the apparent exit from a decades-long deflationary mindset. This is not simply about inflation readings moving above zero. It is about what sustained, stable inflation changes at the behavioral level, whether for companies, for households, or for the policy apparatus that surrounds them.

For companies, inflation removes the excuse for inaction. In a world of flat or falling prices, sitting on cash, leaving cross-shareholdings intact, and protecting low-returning business lines could all be rationalized. In a world of rising prices and rising input costs, that posture becomes costly. It invites shareholder pressure, regulatory attention, and competitive disadvantage. The result, and this is already showing up in the data, is a record pace of cross-shareholding sales, record levels of share buybacks, record shareholder proposals, and a record number of companies adopting stock compensation plans.1

The Tokyo Stock Exchange's 2022 restructuring accelerated this.2 By shining a direct spotlight on companies trading below book value and demanding they articulate a credible path to improvement, the TSE created accountability where there was previously only convention. The Prime market has seen its price-to-book ratio expand by roughly 35–40% since then. That is meaningful movement, and it is real, but the analysis suggests return on equity (ROE) improvement is still incomplete. In other words, the market has rerated somewhat, but the fundamental earnings and capital discipline story is still unfinished, which is precisely what makes it interesting.3

The expected summer 2026 Corporate Governance Code revision adds another layer.4 If it refocuses attention on cash-rich companies, cross-shareholding unwind candidates, and firms with excess real-estate or balance-sheet resources, it could shift the governance reform story from a broad 'improvement' phase into a more actionable 'capital release' phase. That is a meaningful distinction for equity investors.

Thematic Tailwinds: AI, Defense, and the Infrastructure Supercycle

The structural backdrop alone would be enough to make Japan interesting. What makes it compelling in 2026 is the overlay of powerful thematic tailwinds that run directly through Japan's industrial economy.

Artificial intelligence is not just a U.S. software story. The buildout of AI infrastructure, specifically data centers, power systems, thermal management, advanced components, and semiconductor capital equipment, runs through Japanese suppliers in ways that are often underappreciated by investors focused on the hyperscaler layer. Japan has upstream and downstream beneficiaries of the AI capex cycle that do not come with U.S. mega-cap multiples. For investors looking for AI exposure with different valuation characteristics, Japan's industrial business-to-business sector could be one of the more compelling answers.

Defense spending is the other major thematic thread. Europe has received most of the attention in this area, but Japan is increasing its defense budget meaningfully through the end of the decade. Much of the spending is focused on missile defense systems, cybersecurity capabilities, and broader national security infrastructure. These are not one-year budget line items, but rather they are multi-year capital commitments, and Japanese industrial companies with the relevant capabilities are direct beneficiaries.

Underneath both of these sits a broader infrastructure renewal cycle. The Takaichi administration's 17 strategic investment areas5 include energy security, decarbonization, domestic supply chain resilience, and national resilience infrastructure. The implication for equity investors is that upstream business-to-business sectors, including machinery, electric appliances, construction and materials, precision instruments, steel and nonferrous metals, may have better earnings visibility than more consumer-facing or globally exposed parts of the market.

None of this depends on a weak yen. One of the important shifts in the Japan story is that the old reflexive link between yen weakness and equity outperformance has become less mechanical. Companies have improved margins, diversified revenue geographically, and reduced their sensitivity to currency moves. Japan can be attractive without a dramatictailwind from a depreciating yen.

Households Are Coming: Nippon Individual Savings Account (NISA) and the Savings Rotation

One structural argument for Japanese equities that deserves more attention is the domestic savings rotation. For decades, Japanese households kept an extraordinary share of their financial assets in cash and deposits, a legacy of the deflationary era, when real returns on cash were not meaningfully negative and equity markets had a long track record of disappointing.

The NISA program is beginning to change that. NISA purchases have already exceeded the government's cumulative target ahead of schedule. With inflation now eroding the real value of cash, and with corporate governance reform making Japanese equities structurally more attractive, the incentives for households to reallocate toward equities are stronger than they have been in a generation. The scale of the potential shift is significant:

If Japanese household equity allocations moved meaningfully toward European norms, the resulting inflows could represent a substantial fraction of the TOPIX Prime market cap.

Even partial realization of that shift is a powerful technical support for Japanese equities over time.6

How OPPJ Captures the Opportunity

The WisdomTree Japan Opportunities Fund (OPPJ) tracks the WisdomTree Japan Opportunities Index.

The strategy is built around four distinct sleeves. The first targets the five trading firms in which Berkshire Hathaway holds strategic stakes, companies like Mitsubishi Corporation, Mitsui & Co., and Marubeni Corporation. These sogo shosha are themselves broadly diversified across the Japanese industrial economy, and they have delivered shareholder yields that compare favorably to both the MSCI Japan Index and the S&P 500 Index.7 Mitsubishi Corporation, for example, currently carries a total shareholder yield meaningfully above both benchmarks. Buffett's entry into these names in 20198 reinvigorated foreign investor attention to Japan, and the positions have compounded well since.

The second sleeve focuses on high shareholder yield, specifically companies that return capital to shareholders through dividends and net buybacks at above-average rates. This is more than an income play. Two-plus decades of data show that the highest shareholder yield quintile within Japan has outperformed the lowest by a wide margin, with lower volatility along the way. As Japanese companies increasingly use buybacks alongside dividends to return capital, as over 84% of MSCI Japan constituents now carry a positive net buyback yield, up from nearly zero in the mid-1990s, the shareholder yield signal becomes more powerful and more broadly applicable.9

The third sleeve targets corporate governance improvers: companies with low valuations, such as low price-to-book ratios, that are also demonstrating earnings and dividend growth. This is essentially a systematic way to capture companies in the process of reform, before their valuation improvement is fully reflected in prices.

The fourth sleeve—the so-called Geopolitical-Alpha (GeoAlpha) component—is where OPPJ distinguishes itself most clearly from other Japan strategies. It provides exposure to companies positioned to benefit from geopolitical events, fiscal and monetary policy shifts, technological innovation, and shifting consumer preferences. This is where AI infrastructure, defense, and domestic capex themes enter the portfolio in a systematic, rules-based way. Holdings like Mitsubishi Heavy Industries, with its combined energy systems and defense capabilities, illustrate how thematic selection works in practice: companies positioned at the intersection of multiple structural tailwinds, selected through a disciplined process rather than discretionary judgment.

The strategy also applies a dynamic currency hedging overlay. Yen exposure is managed monthly, ranging from 0% to 100% hedged.

Conclusion: The Strategy Is Working

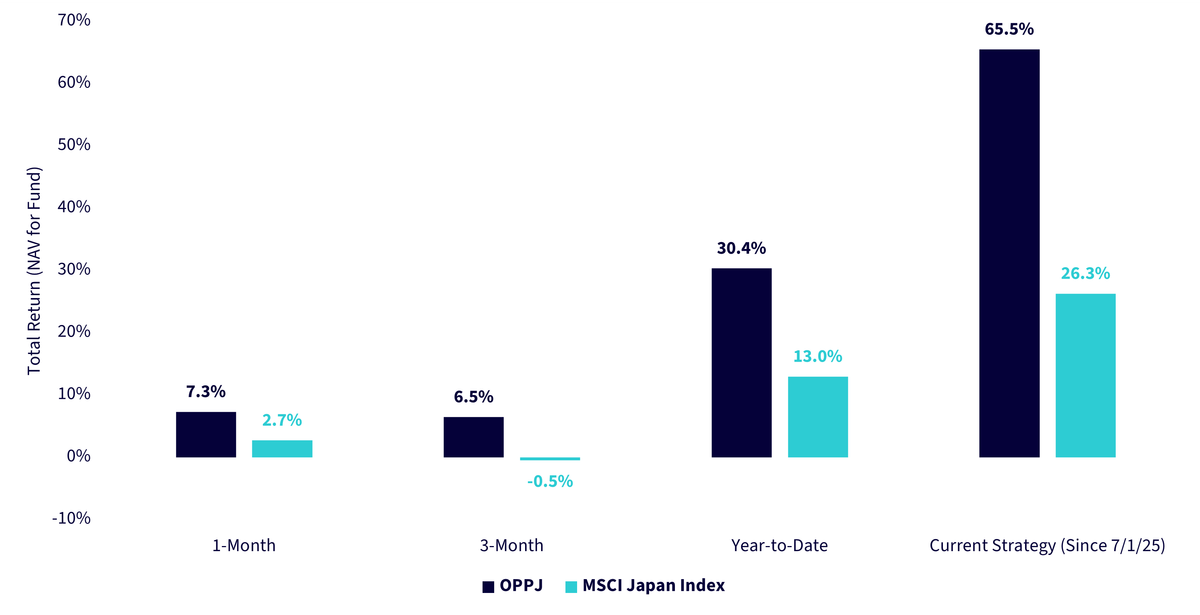

OPPJ started running its current strategy on July 1, 2025, so we are getting closer and closer to the first full year live track record. Figure 1a showcases some strong results relative to the MSCI Japan Index benchmark. While we don’t know whether this type of outperformance will continue, we really like the setup espoused in the first sections of this piece. Japan’s equity rally is occurring across many parts of its market for a diverse set of reasons, and OPPJ is designed with such a multi-dimensional focus in mind.

Figure 1a: A Differentiated Performance Trajectory for Japan’s Equities

Figure 1b: Standardized Returns

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of May 18, 2026, but showing returns for the period ended May 15, 2026 for Figure 1a and March 31, 2026 for 1b. Prior to July 01, 2025, the Fund was known as the WisdomTree Japan Hedged SmallCap Equity Fund (DXJS). On that date the Fund’s investment policy changed. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance and to download the respective Fund prospectuses, click here.

The investment story for Japan in 2026 is not that it is cheap. It is that multiple long-duration forces — reflation, governance reform, AI capex, defense spending, domestic savings rotation, and policy continuity — are converging at once, while valuations and positioning still leave room for upside. OPPJ is built to capture that convergence in a disciplined, rules-based way. That combination is worth paying attention to.

1 Source: Nakazawa, 2026.

2 Source: Japan Exchange Group. (2022). Overview of market restructuring. Tokyo Stock Exchange.

3 Source: Nakazawa, 2026.

4 Source: Financial Services Agency. (2026, April 10). Draft revisions to the Corporate Governance Code for public consultation.

5 Source: Prime Minister's Office of Japan. (2025, December 17). Press conference by Prime Minister Takaichi.

6 Source: Nakazawa, 2026.

7 Source: FactSet, with data as of April 30, 2026.

8 Source: Buffett, W. E. (2025, February 22). 2024 annual report: Letter to shareholders. Berkshire Hathaway Inc.

9 Source: FactSet, with data as of April 30, 2026.

For current holdings, please click here. Holdings are subject to risk and change.

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Japan Opportunities Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.