From Trading Houses to Tokio Marine: Buffett’s Expanding Bet on Japan

Published April 10, 2026

Global Head of Research

Key Takeaways

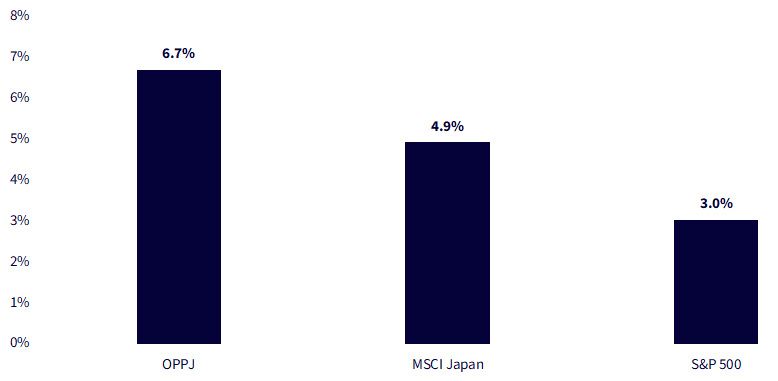

- Japan’s broad market equities are trading at a strong equity risk premium of 4.9%, significantly higher than the S&P 500 Index at 3.0%, while delivering superior earnings per share growth, positioning investors to capture both valuation upside and earnings momentum through strategies like the WisdomTree Japan Opportunities Fund (OPPJ), which had an even higher figure at 6.7%.

- Despite macro risks such as energy shocks and global uncertainty, Japan’s surge in shareholder returns, ¥18–20 trillion in annual buybacks alongside rising dividends, signals a structural governance shift that OPPJ systematically targets through its shareholder yield and corporate reform exposures.

- Warren Buffett’s expansion from trading houses to Tokio Marine underscores Japan’s evolution into a globally integrated, capital efficient market, reinforcing the case for investors to consider this multi-faceted opportunity via OPPJ's blend of focusing on Berkshire’s Japan investments, value opportunities, corporate governance improvement and thematic growth allocations.

Japan is emerging as one of the most compelling opportunities in global equities today.

What makes this moment different is not a single catalyst, but a convergence of forces. Valuations remain meaningfully discounted relative to global peers. Earnings growth is broadening across sectors.1 And perhaps most importantly, corporate Japan is undergoing a structural shift toward higher shareholder returns, improved governance, and more disciplined capital allocation.

We believe this is not a cyclical rebound or a short-term trade, but instead it is a market that is evolving at its core.

Importantly, this opportunity has not gone unnoticed. Some of the world’s most disciplined long-term investors began positioning for it years ago.

Buffett’s Japan Playbook: From Valuation to Integration

Warren Buffett’s entry into Japan in 2019 was deceptively simple. Berkshire Hathaway began acquiring stakes in five large Japanese trading houses. These are companies with diversified global operations, strong cash flows, and shareholder-friendly policies.

What stood out to Buffett was not complexity, but arithmetic. As he noted, Berkshire “simply looked at their financial records and were amazed at the low prices of their stocks”.2

That initial insight has aged well. Since those investments became publicly known, they have outperformed the S&P 500 Index, reinforcing the idea that Japan’s discount, particularly of these companies, was not justified by fundamentals.3

But what is more interesting is how Berkshire’s approach has evolved.

Tokio Marine: A Signal, Not Just a Stock

At first glance, the Tokio Marine investment may appear modest in size. But structurally, it is far more significant.

The transaction includes both an equity stake and a reinsurance relationship, likely increasing the quota-share structure within Tokio Marine’s reinsurance mix. This creates a mutually beneficial arrangement: Tokio Marine gains capital flexibility and earnings stability, while Berkshire gains access to a stream of insurance liabilities, “float”, that it can invest against.

More broadly, Tokio Marine highlights a key characteristic of Japanese corporates that is often underappreciated: global reach. Many Japanese firms generate significant revenue outside Japan, effectively making them exporters of capital, technology, and expertise rather than purely domestic plays.

Seen through this lens, Japan is less a local economy and more a collection of globally integrated businesses, often trading at a discount to their international peers.4

Valuations and Earnings: A Rare Combination

The opportunity in Japan becomes clearer when you step back and look at the combination of valuation and earnings.

Valuation through the Equity Risk Premium

One way to look at the valuation of a market regards a review of the earnings yield versus a measure of the government bond yield.

- A higher value tells us that the earnings yield for equities is high relative to what’s otherwise available in government fixed income.

- A lower value tells us that the earnings yield for equities is low relative to what is otherwise available in fixed income, and since fixed income tends to be lower volatility, the ‘extra risk’ of equities could look less compelling.

In Figure 1, we see the equity risk premium of the S&P 500 and MSCI Japan Indexes and then the WisdomTree Japan Opportunities Fund (OPPJ). Investors understand that the S&P 500 Index has delivered strong performance over the years and become more expensive relative to U.S. government bonds. Japan as a broad market, seen through the MSCI Japan Index, is significantly less expensive than the S&P 500 Index on this basis.

OPPJ is focused on valuation opportunities within Japan as one of its core methodology tenets, which we will explain further in the text that follows. However, in Figure 1, we do see how this specific focus has led to a more than 2x equity risk premium relative to that of the S&P 500 Index.

Figure 1: A Comparison of Equity Risk Premia, Japanese vs. U.S. Equities

Sources: WisdomTree, MSCI, Bloomberg, 10/31/2013-3/31/2026. OPPJ = WisdomTree Japan Opportunities Fund. Japanese Equity Risk Premium (MSCI Japan, OPPJ) measured by the forward earnings yields of the respective fund/index less the 10 Year Japanese Inflation Adjusted Government Bond Yield. S&P 500 Equity Risk Premium measured by the forward earnings yield of the index less the 10 Year US Treasury Inflation Adjusted Bond Yield. You cannot invest directly in an index. Past performance is not indicative of future returns.

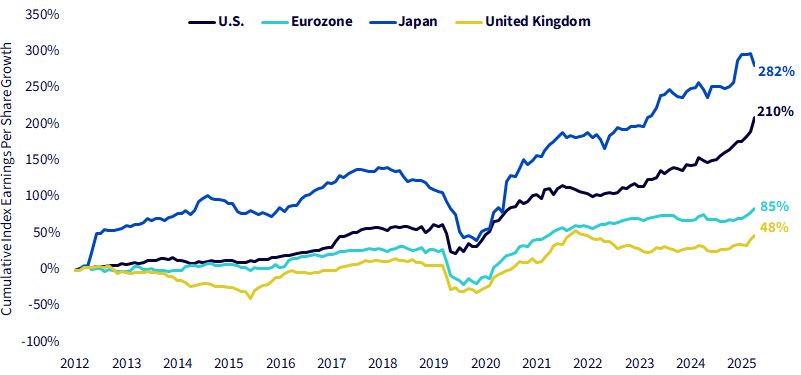

At the same time, earnings growth has been strong. In Figure 2, we see how the MSCI Japan Index, shown as Japan, has delivered cumulative earnings-per-share growth well ahead of that of the other MSCI country and regional benchmark indices shown. We do notice the near-term blip downwards and recognize that the conflict in Iran and the energy situation following on from that may not be ideal, but we believe the overall trend remains intact.

Figure 2: Japan’s Earnings Per Share Growth has been Impressive

Sources: WisdomTree, MSCI, with data from 12/31/2012 to 3/31/2026. U.S., Eurozone, Japan and UK measured by respective MSCI Index universes. Earnings-per-share growth measured in local currency. You cannot invest directly in an index.

This combination, lower valuations and growing earnings, is rare. It creates a setup where investors are not paying for perfection, but still participating in meaningful growth.

The Structural Shift: Shareholder Returns and Governance

Perhaps the most important change in Japan is not valuation or earnings, it is behavior.

Corporate Japan has undergone a quiet transformation in how it treats shareholders. Dividends have increased, buybacks have accelerated, and shareholder yield has become a defining feature of the market.5

Over the past decade, shareholder returns in Japan have undergone a structural shift. Share buybacks have surged to record levels, reaching roughly ¥18–20 trillion annually in recent years and remaining on track for new highs in 2025, while dividends have also continued to rise steadily as companies allocate a greater share of earnings to shareholders.6

This shift is not cosmetic. It reflects deeper changes in corporate governance, capital allocation discipline, and alignment with global investors.

Translating the Opportunity: The OPPJ Framework

Capturing this opportunity requires more than a broad allocation to Japan. It requires a framework that reflects the multiple dimensions of the story.

Here is where, as mentioned previously, we go more deeply into the core tenets underlying the OPPJ methodology, specifically that of the WisdomTree Japan Opportunities Index.

At its core, the strategy allocates across four distinct but complementary sleeves:

- Strategic Berkshire Holdings : Companies where Berkshire has demonstrated long-term conviction, reflecting proven capital allocation and global exposure.

- Shareholder Yield Leaders : Firms returning capital through dividends and buybacks, capturing Japan’s structural shift toward shareholder alignment.

- Corporate Governance Improvers : Companies with attractive valuations and improving fundamentals, often reflecting underappreciated turnaround potential.

- Thematic Beneficiaries : Businesses positioned to benefit from global trends such as geopolitical realignment, technological innovation (such as those exhibiting connections to artificial intelligence), and policy shifts.

The index is rules-based and systematically constructed, with allocations across these sleeves and a dynamic currency hedging overlay that adjusts yen exposure based on market conditions.

This structure matters because it avoids seeking to oversimplify Japan’s equity market into a single narrative. Japan is not just a value story. It is not just a governance story. It is not just a macro story.

We think it can be all of them, simultaneously.

The Bigger Picture

Warren Buffett recognized the opportunity early, in 2019, through the lens of valuation. His and Berkshire Hathaway’s more recent moves, Tokio Marine being an example, suggest something deeper: a willingness to integrate into the Japanese financial and corporate ecosystem.

For investors, the implication is clear. Japan is no longer simply an “international allocation.” It is a differentiated opportunity set, one that combines elements of value, quality, income, and thematic exposure in a way that is increasingly difficult to find elsewhere.

And importantly, it is an opportunity that we believe is still not fully appreciated.

- Source: Bloomberg, with data as of 3/31/2026 and Japanese equity universe referenced: MSCI Japan Index.

- Source: Buffett, W. E. (2025). Berkshire Hathaway Inc. 2024 annual report: Letter to shareholders. Berkshire Hathaway Inc.

- Source: Bloomberg, with data reference over the period since July 2019, the date cited in Warren Buffett’s initial investment in five large Japanese trading houses.

- Source: Takemura, A., & Nagasaka, M. (2026, March 26). Tokio Marine Holdings (8766): Key discussion points following announcement of strategic partnership with Berkshire Hathaway Group. Morgan Stanley MUFG Securities Co., Ltd.

- Source: Financial Times. (2025, May 1). Japan’s share buybacks nearly triple as governance push gains pace.

- Source: Nippon.com. (2026, February 12). Japan’s share buybacks on track for record high in fiscal 2025.

Source: Bloomberg, with data as of 3/31/2026 and Japanese equity universe referenced: MSCI Japan Index.

Source: Buffett, W. E. (2025). Berkshire Hathaway Inc. 2024 annual report: Letter to shareholders. Berkshire Hathaway Inc.

Source: Bloomberg, with data reference over the period since July 2019, the date cited in Warren Buffett’s initial investment in five large Japanese trading houses.

Source: Takemura, A., & Nagasaka, M. (2026, March 26). Tokio Marine Holdings (8766): Key discussion points following announcement of strategic partnership with Berkshire Hathaway Group. Morgan Stanley MUFG Securities Co., Ltd.

Source: Financial Times. (2025, May 1). Japan’s share buybacks nearly triple as governance push gains pace.

Source: Nippon.com. (2026, February 12). Japan’s share buybacks on track for record high in fiscal 2025.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

About the contributor

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.