GCC

Enhanced Commodity Strategy Fund

Published July 21, 2025

Global Head of Research

There are moments in markets where the machinery of global trade, politics, and speculation collide to produce outcomes that feel more like financial theater than textbook economics. What we are witnessing in copper is precisely that. Following a surprise 50% U.S. tariff announcement on imported copper, prices on the COMEX exploded upward—creating a historic arbitrage between U.S. and international benchmarks. Commodity traders like Trafigura, Glencore, and Mercuria executed one of the most profitable basis trades in recent history, shipping hundreds of thousands of tonnes into the U.S. and reaping an estimated $300 million windfall3. This isn't just about a metal—it's about how fast capital moves to exploit inefficiencies when policy reshapes the rules overnight.

But here's the bigger picture: copper isn't just the story of a tariff or a trade. It's the story of industrial power in the age of electrification. From EVs to semiconductors to data center infrastructure, copper is foundational—and the world may not have enough of it. Glencore estimates the supply shortfall could grow by a million metric tons a year through 2050, essentially requiring a new Escondida-sized mine annually just to keep up4. Add geopolitics, tariffs, and recycling constraints, and copper starts to behave not like a boring industrial metal, but like a strategic asset. What we're seeing right now might be just a preview of how commodities will behave in an age where materials security starts to rival energy security.

Precious MetalsLeadership IsSignaling a Regime Shift

Gold and the U.S. Dollar Index (DXY) have shown an extraordinary −96 % inverse correlation this year—a relationship that has appeared only seven times since 1990 and historically preceded above-average gold returns.5 What is different in 2025 is that central banks are doing the heavy lifting: 95% of 71 banks surveyed expect to raise their gold reserves over the next 12 months, with none planning a cut—the highest net-positive reading since the survey began.6 That institutional bid underpins bullion's role as a possible portfolio stabilizer in an era of real rate uncertainty.

Base Metal Tightness Adds a Growth-Beta Kicker

Copper is flowing into the U.S. at a breakneck pace as traders front-run aggressive new tariffs, leaving LME inventories depleted and global supply increasingly bifurcated. At the same time, Chinese smelters—facing evaporating domestic premiums—are eyeing export markets to offload excess metal, underscoring just how disjointed and reactive the global copper ecosystem has become. But this isn't just short-term dislocation. Beneath the surface, copper is being pulled into the gravitational fields of three megatrends: the exponential rise of AI-fueled data centers, accelerated defense rearmament, and a global electrification push. It's no longer just a cyclical commodity—it's morphing into a strategic asset with both scarcity dynamics and long-duration demand tailwinds.

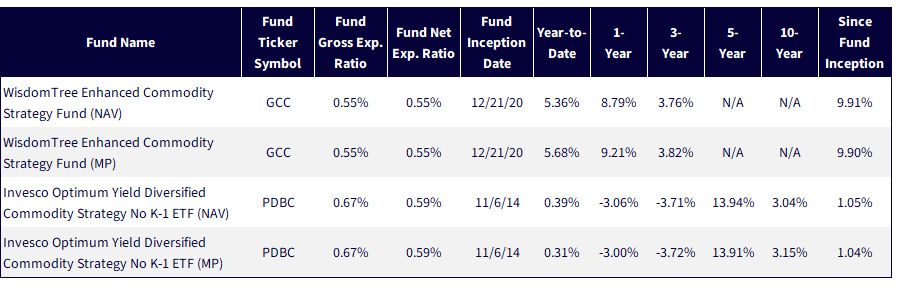

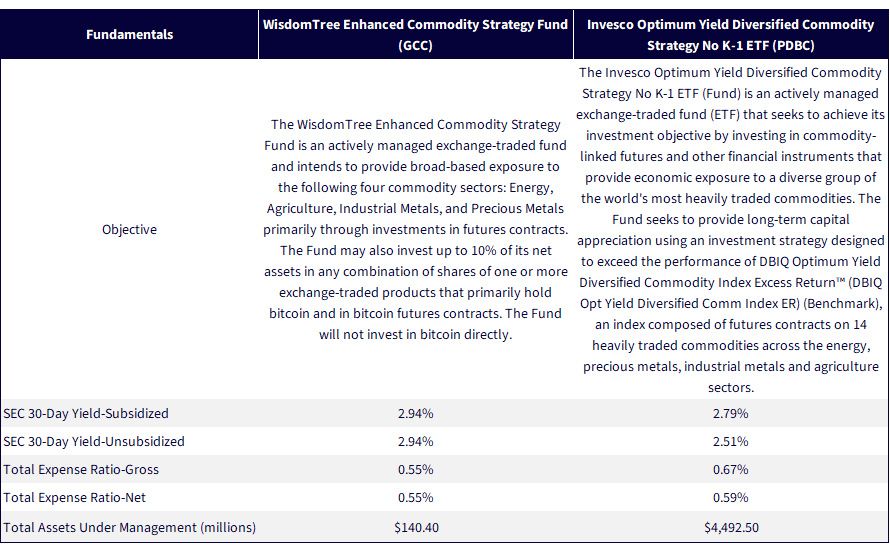

In the world of commodity investing, category names can obscure critical strategy differences. Both the WisdomTree Enhanced Commodity Strategy Fund (GCC) and the Invesco Optimum Yield Diversified Commodity Strategy ETF (PDBC) sit within the Morningstar "Commodity Broad Basket" category7 and share a futures-based, K-1-free structure.

Yet under the hood, they represent fundamentally distinct approaches. PDBC, the category leader by assets under management,8 tracks the DBIQ Optimum Yield Diversified Commodity Index and emphasizes maximizing roll yield by dynamically selecting futures contracts. GCC, while also using an enhanced roll methodology, incorporates a broader, research-driven strategic allocation—diversifying across 26 contracts, including up to 5% in regulated bitcoin futures.

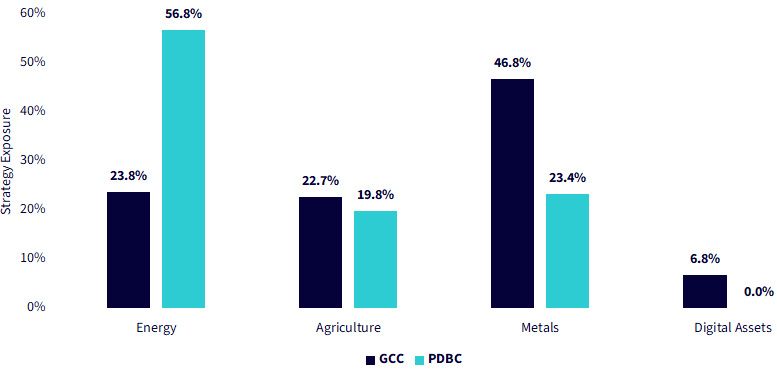

This divergence becomes critical in sector compositions. PDBC's underlying index assigns more than 50% weight to energy contracts (e.g., WTI crude, Brent crude, ultra-low sulfur diesel and gasoline), as of Q2 2025.9

GCC, in contrast, limits energy exposure to around 25%, deliberately under-weighting the most volatile sector in favor of more balanced allocations to precious metals, industrial metals and agriculture.

GCC gives roughly 25% weight to industrial metals like copper and aluminum—commodities increasingly tied to electrification, defense technology and infrastructure modernization—while also allocating significantly to gold and silver as monetary hedges.

The key takeaway is not that one strategy is superior to the other, but that they are purpose-built for different investor profiles. PDBC may appeal to those seeking a higher beta to energy-related commodities and tactical exposure to oil cycles, while GCC may be better aligned with investors emphasizing diversification, risk reduction and thematic alignment with long-term trends like decarbonization and inflation hedging.

With oil selling off following the Iran-Israel conflict, the more diversified exposures have been paying off for GCC recently.

Given that both funds appear under the same Morningstar category, investors often overlook how materially different the exposures—and potential outcomes—can be. This makes a closer look not just useful, but essential.

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 7/11/25, with returns as of 6/30/25. NAV denotes total return performance at net asset value. MP denotes market price performance. The performance data quoted represents past performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the respective ticker: GCC, PDBC.

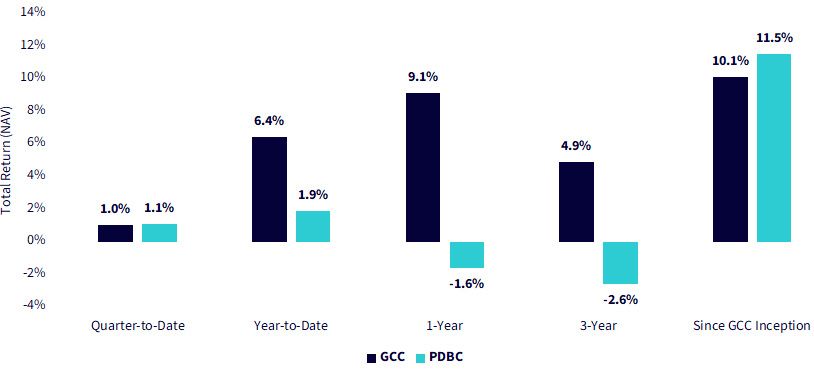

The Bottom-Line Drivers of Differentiated Returns

When oil is the market's engine, PDBC can outrun a diversified peer; when the leadership baton passes to gold or the green-metals complex, GCC's broader mix shows its stride.

Figure 2 displays exactly that hand off: across recent periods when metals outperformed, GCC's returns dominate, whereas PDBC's edge only re-emerges over the full cycle that includes 2021–22's energy market price spike.

Figure 2: When Methodology Matters: A Multi-Year Test of Commodity ETF Design

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 7/11/25, with returns as of 7/10/25. NAV denotes total return performance at net asset value. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the respective ticker: GCC, PDBC.

Figure 3 helps us to see a simplified mapping of exposures.

Figure 3: Portfolio DNA across Ags, Metals and Digital Assets

Sources: WisdomTree and Invesco product pages, with data as of 7/10/25. Subject to change.

Conclusion: Why Commodity Exposure Demands Clarity

For investors seeking to add real asset exposure, not all broad commodity strategies are created equal—and the differences aren't always intuitive. Many investors assume that a commodity allocation will offer general inflation protection or a hedge against macroeconomic uncertainty, but if over 50% of that allocation is implicitly a bet on energy, the allocation's actual behavior can deviate sharply from that expectation.

This is precisely why looking under the hood matters. Commodity investing is not a monolith; it's a mosaic of volatile, cyclical sub-sectors with vastly different drivers. A more diversified approach—like that of GCC—not only smooths sector-specific drawdowns but also increases the chance of capturing emerging themes, from industrial decarbonization to central bank gold accumulation or the institutionalization of bitcoin.

For allocators, the key insight is simple: choose the exposure that matches your conviction. Otherwise, your commodity sleeve might just be a crude oil fund in disguise.

Sources: WisdomTree's fund compare tool, which utilizes data from FactSet and Morningstar. Assets under management is from the individual fund sponsor websites and is as of 7/10/25. Fund SEC 30-Day Yields are as of June 30, 2025.

1 Hook, L. (2025, July 11). Commodity traders poised for $300mn windfall from US copper rush. Financial Times.

2 Sources: WisdomTree, Invesco, as of 7/10/25.

3 Hook, L. (2025, July 11). Commodity traders poised for $300mn windfall from US copper rush. Financial Times.

4 Uberti, D., & Dezember, R. (2025, July 10). Five things to know about record copper prices. The Wall Street Journal.

5 Source: Bloomberg, with data as of 3/31/25.

6 Source: Central Bank Gold Reserves Survey 2025: Perspectives on Gold Reserves, World Gold Council, 6/17/25.

7 Source: Morningstar, as of 3/31/25.

8 Source: Morningstar, with fund assets under management reviewed as of market close on 6/23/26.

9 Source: PDBC fund page on Invesco's website.

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund to fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund.

GCC: There are risks associated with investing, including the possible loss of principal. An investment in this Fund is speculative, involves a substantial degree of risk and should not constitute an investor’s entire portfolio. One of the risks associated with the Fund is the complexity of the different factors that contribute to the Fund’s performance. These factors include the use of commodity futures contracts. In addition, bitcoin and bitcoin futures are a relatively new asset class. They are subject to unique and substantial risks and, historically, have been subject to significant price volatility. While the bitcoin futures market has grown substantially since bitcoin futures commenced trading, there can be no assurance that this growth will continue. In addition, derivatives can be volatile and may be less liquid than other securities and more sensitive to the effects of varied economic conditions. The value of the shares of the Fund relates directly to the value of the futures contracts and other assets held by the Fund, and any fluctuation in the value of these assets could adversely affect an investment in the Fund’s shares. Because of the frequency with which the Fund expects to roll futures contracts, the price of futures contracts further from expiration may be higher (a condition known as “contango”) or lower (a condition known as “backwardation”), and the impact of such contango or backwardation may be greater than the impact would be if the Fund experienced less portfolio turnover. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

PDBC: Before investing, investors should carefully read the prospectus and consider the investment objectives, risks, charges and expenses. For this and more complete information about the fund, investors should ask their financial professionals for a prospectus or download one at invesco.com. There are risks involved with investing in ETFs, including the possible loss of money. Actively managed ETFs do not necessarily seek to replicate the performance of a specified index. Actively managed ETFs are subject to risks similar to stocks, including those related to short selling and margin maintenance. Ordinary brokerage commissions apply. The fund’s return may not match the return of the index. The fund is subject to certain other risks. Please see the current prospectus for more information regarding the risk associated with an investment in the fund.

The fund is subject to management risk because it is an actively managed portfolio. The investment techniques and risk analysis used by the portfolio managers may not produce the desired results.

Risks of futures contracts include: an imperfect correlation between the value of the futures contract and the underlying commodity; possible lack of a liquid secondary market; inability to close a futures contract when desired; losses due to unanticipated market movements; obligation for the fund to make daily cash payments to maintain its required margin; failure to close a position may result in the fund receiving an illiquid commodity; and unfavorable execution prices.

In pursuing its investment strategy, particularly when “rolling” futures contracts, the fund may engage in frequent trading of its portfolio securities, resulting in a high portfolio turnover rate.

Commodity-linked notes may involve substantial risks, including risk of loss of a significant portion of principal and risks resulting from lack of a secondary trading market, temporary price distortions and counterparty risk.

Swaps involve greater risks than direct investments. Swaps are subject to leveraging, liquidity and counterparty risks, and therefore may be difficult to value. Adverse changes in the value or level of the swap can result in gains or losses that are substantially greater than invested, with the potential for unlimited loss.

Derivatives may be more volatile and less liquid than traditional investments and are subject to market, interest rate, credit, leverage, counterparty and management risks. An investment in a derivative could lose more than the cash amount invested.

To qualify as a regulated investment company (“RIC”), the fund must meet a qualifying income test each taxable year. Failure to comply with the test would have significant negative tax consequences for shareholders. The fund believes that income from futures should be treated as qualifying income for purposes of this test, thus qualifying the fund as a RIC. If the IRS were to determine that the fund’s income is derived from the futures did not constitute qualifying income, the fund likely would be required to reduce its exposure to such investments in order to maintain its RIC status.

The fund’s strategy of investing through its subsidiary in derivatives and other financially-linked instruments whose performance is expected to correspond to the commodity markets may cause the fund to recognize more ordinary income. Particularly in periods of rising commodity values, the fund may recognize higher-than-normal ordinary income. Investors should consult with their tax advisor and review all potential tax considerations when determining whether to invest.

Leverage created from borrowing or certain types of transactions or instruments may impair liquidity, cause positions to be liquidated at an unfavorable time, lose more than the amount invested or increase volatility.

The fund may hold illiquid securities that it may be unable to sell at the preferred time or price and could lose its entire investment in such securities.

The fund currently intends to effect creations and redemptions principally for cash, rather than principally in-kind because of the nature of the fund’s investments. As such, investments in the fund may be less tax efficient than investments in ETFs that create and redeem in-kind.

The shares of the fund are not deposits, interests in or obligations of any Deutsche Bank AG, Deutsche Bank AG London Branch, Deutsche Bank Securities Inc. or any of their respective subsidiaries or affiliates or any other bank (collectively, the “DB Parties”) and are not guaranteed by the DB Parties.

Enhanced Commodity Strategy Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.