DGRW

U.S. Quality Dividend Growth Fund

Published December 18, 2024

Director, Research

The rebalance of the WisdomTree U.S. Quality Dividend Growth Index became effective at the market close on Wednesday, December 11. This post provides the main takeaways from the changes to the Index and how it is positioned heading into 2025.

The Index follows a straightforward investment process that we walk through step by step.

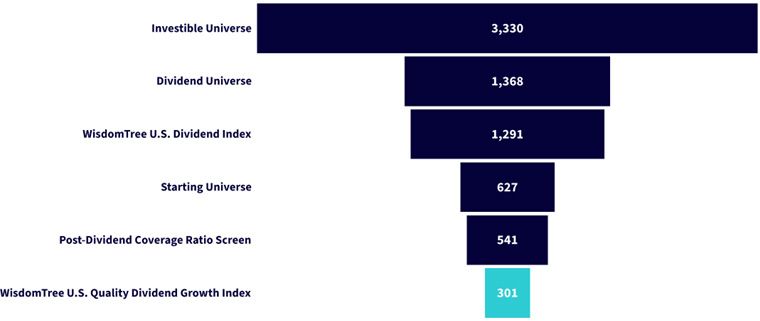

Figure 1 summarizes the process that starts with over 3,000 securities and ends with 301 included.

Unless otherwise specified, all data is as of November 30, 2024, the annual screening date for the Index.

Source: WisdomTree.

WisdomTree builds its proprietary Indexes from the bottom up instead of top down. In a top-down approach, we would start with a universe like the S&P 500 or Russell 1000 and then select securities.

WisdomTree builds its own universe based on eligibility requirements like exchange listing, market capitalization and liquidity. The starting investible universe at this year’s rebalance was 3,330 securities, just broader than the Russell 3000.

This step is self-explanatory: of the 3,330 securities in the investible universe, 41% are regular cash dividend paying companies.

WisdomTree’s key criteria for eligibility, unlike other dividend growth indexes, is that a company is an active dividend payer currently and not that it has paid or grown a dividend historically (say for the last 5, 10 or 25 years).

The parent index for WisdomTree’s domestic dividend Indexes is the WisdomTree U.S. Dividend Index. This Index can be thought of as our all cap or total market dividend index.

The only distinction between the dividend universe of 1,368 securities and the 1,291 securities that get included in this Index is the Composite Risk Screen.

The Composite Risk Screen (CRS), which removed exposure to 77 securities, aims to mitigate the risk of over-weighting value traps in our dividend-weighted Indexes. The measures included in the CRS include profitability (measured within industry groups), risk-adjusted momentum and dividend yield (the highest dividend yields representing the most risk).

The Index is designed to provide exposure to mid-cap and large-cap securities. Securities with less than $2bn market capitalization or that are included in the WisdomTree U.S. SmallCap Dividend Index are excluded.

This market-cap cutoff removes about half of the companies (664) from the WisdomTree U.S. Dividend Index.

Recall that 77 dividend-paying companies were excluded from the WisdomTree U.S. Dividend Index due to the CRS.

The Quality Dividend Growth Index has another key filter for removing exposure to value traps with its dividend coverage ratio screen.

Companies with negative dividend coverage ratios (earnings per share < dividends per share) are removed from the starting universe. At this year’s rebalance, this screen excluded 86 companies.

At this stage, with 541 companies eligible, the Index selects the 300 highest scoring companies on a composite of 50% profitability (3-year return on equity (ROE) and return on assets (ROA)) and 50% median analyst earnings growth estimates.

Because the Index included both shares of Alphabet, the Index has 301 securities.

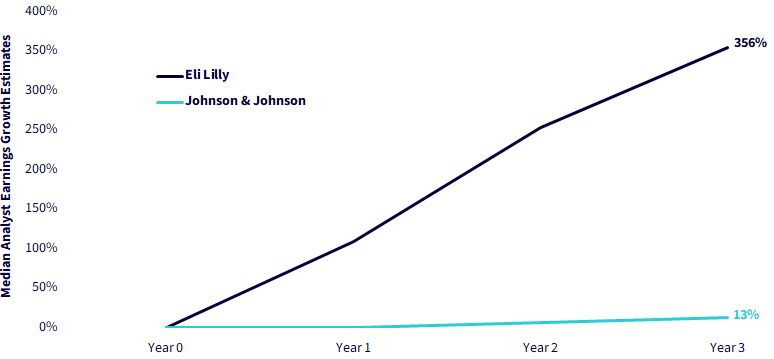

In figure 2, we illustrate how one security was included at the rebalance (Eli Lilly) and one was excluded (Johnson & Johnson). Both securities are in the pharmaceuticals Industry.

Though Eli Lilly scores significantly higher, both it and Johnson & Johnson are in the top 300 on ROE and ROA. The key driver for Eli Lilly’s inclusion over Johnson & Johnson has to do with the growth ranking.

Johnson & Johnson’s growth rank of 440 pushed that company’s ranking outside of the top 300 score needed for inclusion in the Index.

Source: WisdomTree, 11/29/24.

Figure 3 shows a stark difference in analyst estimated earnings growth for the two companies.

Eli Lilly’s earnings growth estimates have skyrocketed due to the success of its popular weight loss drug, Zepbound.

Sources: WisdomTree, FactSet, 11/29/24. Year 0 is the latest annual filing for each company, Year 1 is the next annual filing, and so on.

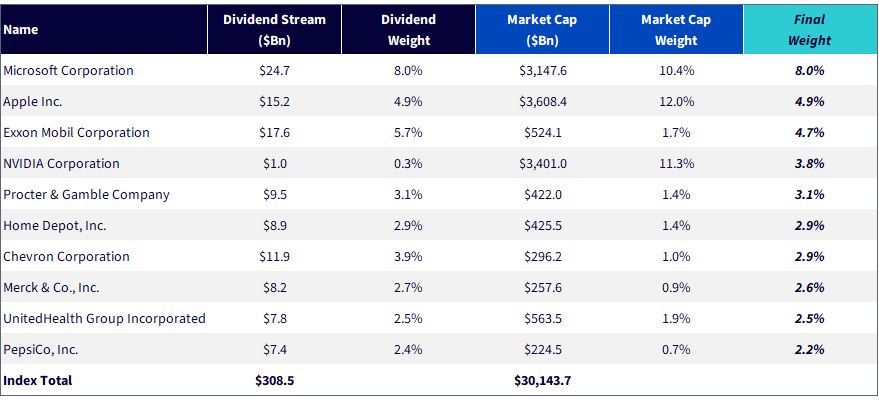

After selecting the 300 highest scoring companies on the composite quality/growth scores, securities are initially weighted based on Dividend Stream, or cash dividends paid.

As seen in figure 4, Microsoft has far and away the largest cash dividend in the U.S., at $25bn. Of the $308.5bn in total dividends across the 300 selected companies, Microsoft’s $25bn dividend gives it a dividend weight of 8%.

In 2022, WisdomTree introduced a constraint on its dividend-weighting relative to market-cap weighting. The constraint is that no security could have a weight that was more than three times or less than one-third its market-cap weight.

The purpose of this change was to seek to mitigate the active risk of any single holding based on dividend weighting relative to market cap, while still having dividend weighting as a critical element of the Index’s valuation discipline.

For example, Nvidia’s final weight of 3.8% is greater than its dividend weight (0.3%) but still well below its market-cap weight (11.3%).

Source: WisdomTree, as of 11/29/24. You cannot invest directly in an index. Past performance is not indicative of future results.

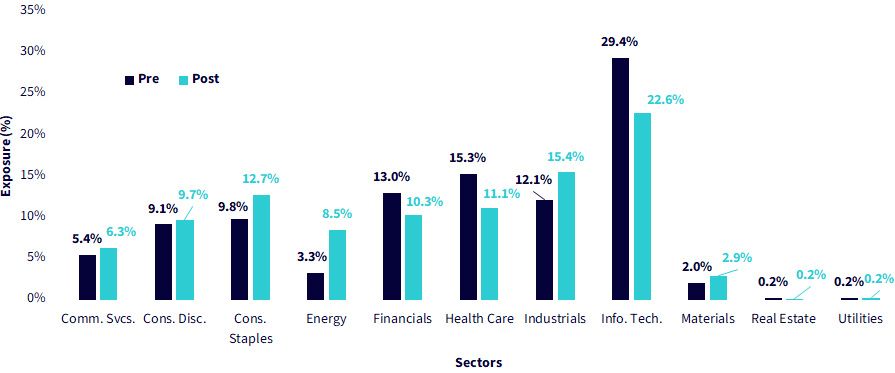

In figure 5 we show the pre- and post-sector weights. There were two notable sector changes at the rebalance:

Source: WisdomTree, as of 11/29/24. You cannot invest directly in an index.

Figure 6 highlights some of the key characteristics of the Index after the rebalance.

From a valuation perspective, the Index has a dividend yield advantage of about 40 basis points and a price-to-earnings ratio that is almost four turns below the S&P 500.

The implied growth rate (ROE x earnings retention ratio) is a key element to the strategy—we do not target companies that paid a higher dividend historically but have the highest combination of current profitability and profit growth potential. We find companies with these characteristics have the greatest capacity to grow dividends going forward.

In a market environment where clients are concerned about valuations and what to do with core allocations, we think a fundamentals-based approach that doesn’t sacrifice on profitability and growth in search of value provides a nice solution.

Source: WisdomTree, as of 11/29/24. WisdomTree U.S. Dividend Growth Index characteristics based on post-rebalance holdings as of the screening date, 11/29/24. You cannot invest directly in an index. Past performance is not indicative of future results.

U.S. Quality Dividend Growth Fund

Director, Research

Matt Wagner joined WisdomTree in May 2017 as an Analyst on the Research team. He currently serves as a Director, where he supports the creation, maintenance, and reconstitution of WisdomTree’s indexes and actively managed ETFs. Matt began his career at Morgan Stanley, working as an analyst in Treasury Capital Markets from 2015 to 2017, focusing on unsecured funding planning, execution, and risk management. He graduated magna cum laude from Boston College in 2015 with a B.A. in International Studies, concentrating in Economics. In 2020, he earned a Certificate in Advanced Valuation from NYU Stern. He is also a Chartered Financial Analyst (CFA) charterholder.