IHDG

International Hedged Quality Dividend Growth Fund

Published November 26, 2024

Director, Research

Each fall, WisdomTree conducts the annual rebalance of its developed international dividend Indexes.

The WisdomTree International Quality Dividend Growth Index selects approximately 300 dividend-paying companies. Companies are selected primarily based on premium quality (return on equity/return on assets) and growth (analyst earnings growth estimates) characteristics.

One-hundred fifty-four securities were maintained in the Index, and the total turnover was around 48%.

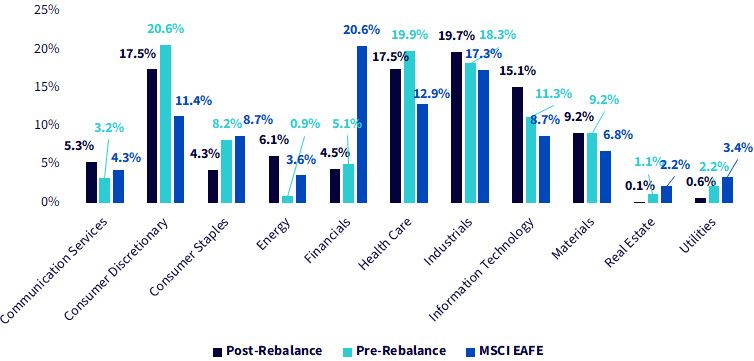

As we can see in figure 1, from a sector perspective, the largest sector over-weights relative to MSCI EAFE are in Consumer Discretionary (+6%) and Information Technology (+6%).

The largest sector under-weights are in Financials (-16%) and Consumer Staples (-4%).

Sources: WisdomTree, FactSet, MSCI. Pre-rebalance data as of 10/30/24 and post-rebalance data as of 10/31/24. MSCI EAFE data as of 9/30/24. You cannot invest directly in an index.

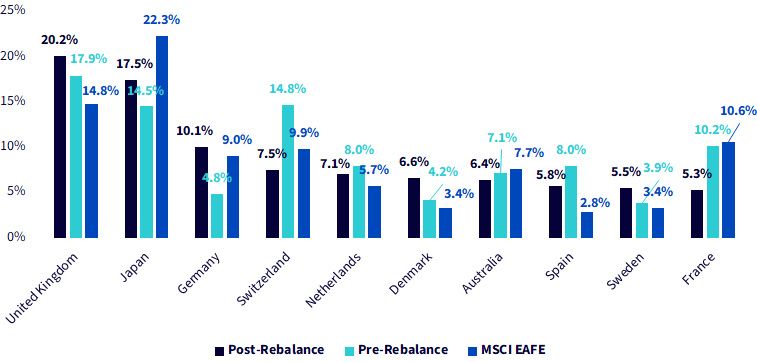

From a country perspective, the greatest over-weight is in the United Kingdom (5%), and the greatest under-weights are in France (-5%) and Japan (-5%), as shown in figure 2.

Sources: WisdomTree, FactSet, MSCI. Pre-rebalance data as of 10/30/24 and post-rebalance data as of 10/31/24. MSCI EAFE data as of 9/30/24. You cannot invest directly in an index.

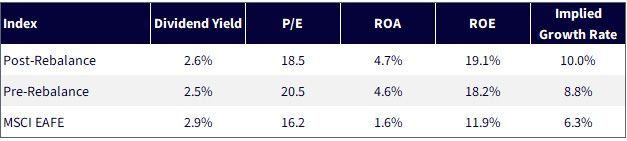

As shown in figure 3, the post-rebalance dividend yield is little changed—from 2.5% to 2.6%.

Interestingly, the price-to-earnings (P/E) ratio was lowered from 20.5x to 18.5x, while there was an improvement in quality characteristics as both return on equity (ROE) and return on assets (ROA) were increased.

The implied growth rate (ROE x earnings retention ratio) was increased from 8.8% to 10.0%, an even greater margin of improvement from the MSCI EAFE Index.

Sources: WisdomTree, FactSet, MSCI. Dividend yield: A financial ratio that shows how much a company pays out in dividends each year relative to its share price. Pre-rebalance data as of 10/30/24 and post-rebalance data as of 10/31/24. MSCI EAFE data as of 9/30/24. You cannot invest directly in an index.

The process of selecting companies with higher profitability and high earnings growth estimates has been rewarded since launching the Index near the end of 2013.

Over the last 10+ years, the Index has outperformed the MSCI EAFE Index by 92 basis points (bps) annualized as high quality has outperformed low quality.

In 2024, this trend reversed, as low-quality (or “junkier”) names have outperformed.

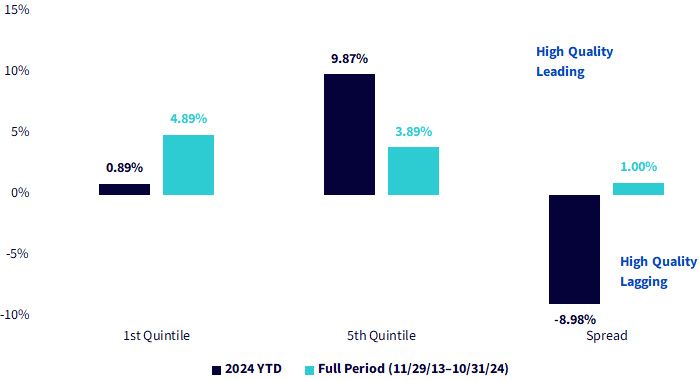

Figure 4 shows us that from November 29, 2013, through October 31, 2024, the highest return-on-equity (ROE) quintile of the MSCI EAFE Index outperformed the lowest quintile by 100 bps annualized.

In 2024, it has been the lowest ROE quintile, outperforming by a whopping 898 bps.

Sources: WisdomTree, FactSet, MSCI, as of 10/31/24. You cannot invest directly in an index. Past performance is not indicative of future returns.

The outperformance of low quality can also be seen from the performance spread of value versus growth in EAFE. Unlike in the U.S. market, where growth has steadily beaten value in 2024, value has beaten growth in the developed international, as seen in figure 5.

Sources: WisdomTree, MSCI, as of 10/31/24. You cannot invest directly in an index. Past performance is not indicative of future returns.

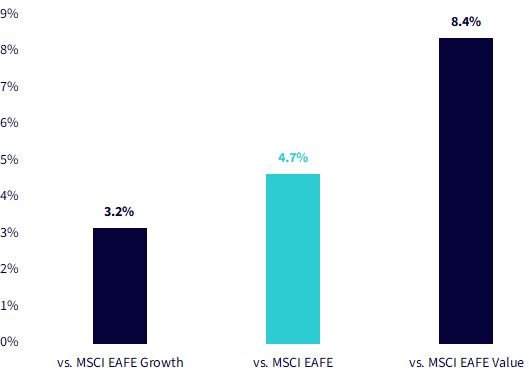

One way of showing that the WisdomTree International Quality Dividend Growth Index skews more toward growth than value is by showing the historical tracking error of the Index relative to the MSCI EAFE Value and Growth Indexes.

In figure 6 below, we show the WisdomTree Index had a tracking error to the Growth Index (3.2%) that was less than half the tracking error to the Value Index (8.4%).

Sources: WisdomTree, MSCI, 11/29/13–9/30/24. You cannot invest directly in an index. Past performance is not indicative of future returns.

Low-quality rallies are not uncommon, but they don’t tend to persist.

As we saw from the year-to-date performance of the MSCI EAFE ROE quintiles, the least profitable names have outperformed over the short run.

Going back more than 10 years, higher ROE companies have handily outpaced lower ROE companies.

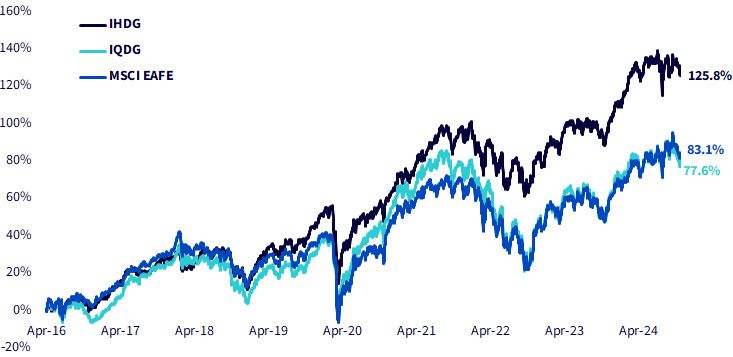

Both the WisdomTree International Quality Dividend Growth Fund (IQDG) and the WisdomTree International Hedged Quality Dividend Growth Fund (IHDG) were launched to systematically target a basket of high-quality dividend-paying companies.

Both Funds track underlying Indexes with the same stock selection criteria. IHDG tracks an Index that aims to neutralize the fluctuations of currency inherent in investing in foreign equities.

With the strengthening of the U.S. dollar over this period, having a currency-hedged international equity exposure has been beneficial to both lowering overall volatility and increasing returns, as demonstrated in figure 7.

Sources: WisdomTree, FactSet, 4/7/16–11/4/24. Start date chosen to coincide with the inception date of the WisdomTree International Quality Dividend Growth Fund (IQDG). Fund returns based on NAV total returns. Index returns are net total returns in USD. You cannot invest directly in an index. Past performance is not indicative of future returns. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances and to download the respective Fund prospectuses, click the relevant ticker: IHDG, IQDG.

For more information on the Index rebalance, please check out the index rebalance summaries:

For definitions of terms in the blog post, please visit the glossary.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

IHDG: To the extent the Fund invests a significant portion of its assets in the securities of companies of a single country or region, it is likely to be impacted by the events or conditions affecting that country or region. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. Derivative investments can be volatile, and these investments may be less liquid than other securities and more sensitive to the effects of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs.

IQDG: Heightened sector exposure increases the Fund’s vulnerability to any single economic, regulatory or other development impacting that sector. This may result in greater share price volatility. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time.

Director, Research

Matt Wagner joined WisdomTree in May 2017 as an Analyst on the Research team. He currently serves as a Director, where he supports the creation, maintenance, and reconstitution of WisdomTree’s indexes and actively managed ETFs. Matt began his career at Morgan Stanley, working as an analyst in Treasury Capital Markets from 2015 to 2017, focusing on unsecured funding planning, execution, and risk management. He graduated magna cum laude from Boston College in 2015 with a B.A. in International Studies, concentrating in Economics. In 2020, he earned a Certificate in Advanced Valuation from NYU Stern. He is also a Chartered Financial Analyst (CFA) charterholder.