DGRW

U.S. Quality Dividend Growth Fund

Published October 28, 2024

Director, Research

We believe the quality factor is one of the most intuitive and widely adopted factor premiums in investor portfolios.

The disappointing returns of emerging markets (EM) in recent years have led many investors to reduce allocations or avoid EM altogether.

We believe that the same principles that “work” for investing in developed markets (DM), like choosing high-quality companies, can also work in EM.

The WisdomTree Emerging Markets Quality Dividend Growth Fund (DGRE) is one way to invest in these high-quality companies in EM.

Last spring, the Fund’s exposure to China was lowered to 0% as part of a strategic decision to mitigate the volatility associated with the market and provide investors a broad-based ex-China EM option.

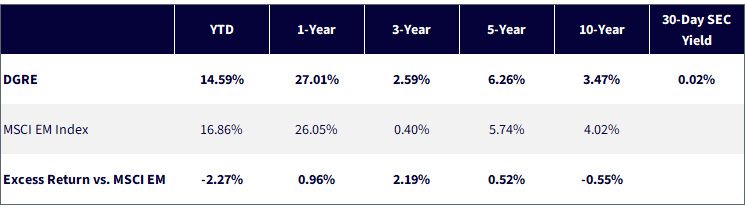

Over the last year, the Fund has outperformed the MSCI Emerging Markets Index without the incremental volatility of the China exposure.

Sources: WisdomTree, MSCI, as of 9/30/24. Fund returns at NAV. You cannot invest directly in an index. Performance of less than one year is

cumulative. You cannot invest directly in an index. Performance is historical and does not guarantee future results. Current

performance may be lower or higher than quoted. Investment returns and principal value of an investment will fluctuate so that

an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance data for the most recent

month-end is available here. WisdomTree shares are bought and sold at market price (not NAV) and are not individually redeemed from

the Fund. Total returns are calculated using the daily 4:00 p.m. ET net asset value (NAV). Market price returns reflect the midpoint of the

bid/ask spread as of the close of trading on the exchange where Fund shares are listed. Market price returns do not represent the returns

you would receive if you traded shares at other times.

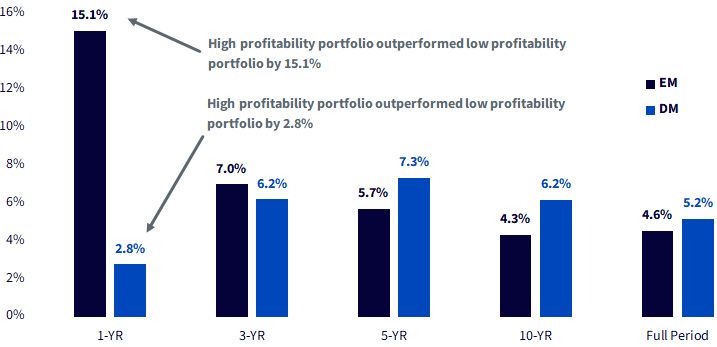

One way to test how strong a factor is, is to see if it performs well in various markets.

The below chart compares returns from DM and EM for companies with high profits versus those with low profits. Since 1991, high-profit companies in both DM and EM have shown similar extra returns.

Over the last one- and three-year periods, high-profit companies in EM have done even better than those in DM.

Sources: WisdomTree, Kenneth French Data Library, 6/30/1991—8/31/2024. Emerging market (EM) and Developed market (DM) returns

measure the return difference of the BIG HiOP and BIG LoOP portfolios for the respective markets. BIG HiOP = intersection of top 90% of

market cap and top 30% on operating profitability. BIG LoOP = intersection of top 90% of market cap and bottom 30% on operating

profitability. Past performance is not indicative of future returns.

DGRE is a rules-based active Fund. The model selects 250–300 dividend-paying companies based on dividend safety measures, profitability metrics and dividend growth rates.

Many investors don’t think of dividends outside of DM. There is arguably an even greater case for looking to dividends in EM where there can be greater questions around accounting standards and earnings reliability. A dividend paid cannot be manipulated and cannot be restated.

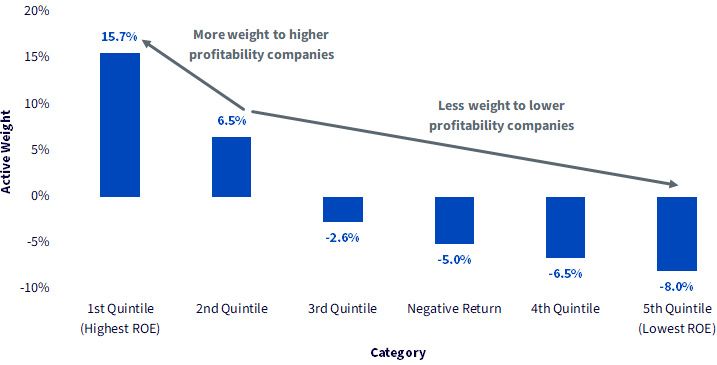

The below graph shows the average tilts to higher return on equity (ROE) quintiles for DGRE relative to the MSCI EM Index over the last three years.

On average, DGRE has had more than 20% greater weight to the highest two ROE quintiles with under-weight allocations to the lowest ROE quintiles and the group of negative return companies.

Sources: WisdomTree, FactSet, for the period 8/31/21 to 8/31/24. Holdings subject to change.

DGRE is rebalanced at minimum each October with the discretion for ad hoc rebalances throughout the year. The most recent rebalance became effective at the close of October 16.

The below table shows the top 10 DGRE holdings before (old) and after (new) the rebalance. The only adds to the top 10 holdings were International Container Terminal Services (three-year annualized dividend growth of 30%) and HDFC Bank (three-year annualized dividend growth of 44%).

Taiwan Semiconductor Manufacturing Company—maintained as the top holding in DGRE—has consistently been one of the fastest dividend growers globally over the last several years, growing at over 11% annualized over the last five years.

Sources: WisdomTree, FactSet, MSCI. DGRE (Old) weights as of 10/16/24, DGRE (New) weights as of 10/17/24, and MSCI EM Index

weights as of 9/30/24. Dropped securities in red. Added securities in green. Chinese companies in blue. You cannot invest directly in an

index. For current holdings of DGRE, please click here. Holdings are subject to risk and change.

The weighting process for DGRE is modified market cap to give greater weight to companies with higher scores on quality and dividend growth. To reduce turnover, constituents that are maintained in the basket are held at a weight that is roughly equal to what it was prior to the rebalance.

The one-way turnover for the Fund at rebalance was 19%.

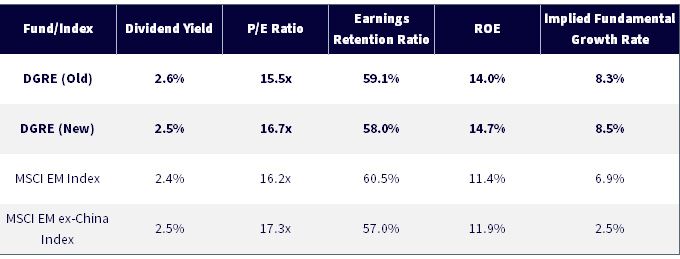

After the rebalance, DGRE's dividend yield and price-to-earnings (P/E) ratio are roughly in line with the MSCI EM Index.

As the process favors quality companies earning a high ROE, the ROE advantage over the broad MSCI EM Index was improved. The implied fundamental growth rate (ROE x earnings retention ratio) advantage over the benchmark was also increased.

Relative to the MSCI EM ex-China Index, valuations are slightly lower on P/E with an even greater improvement on the implied fundamental growth rate than versus the broad MSCI EM Index.

Sources: WisdomTree, FactSet, MSCI. DGRE (Old) weights as of 10/16/24, DGRE (New) weights as of 10/17/24, and MSCI EM Index

and MSCI EM ex-China Index weights as of 9/30/24. You cannot invest directly in an index.

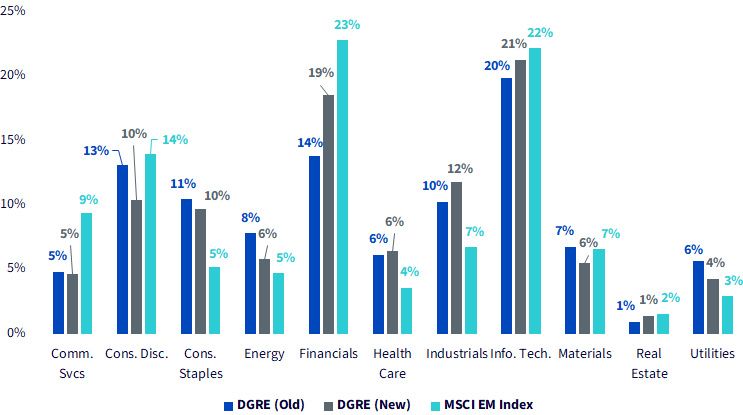

From a sector perspective, the changes were modest. All sector weights are within 5% of the MSCI EM Index. The most notable change was an increase to Financials (+5%).

Sources: WisdomTree, FactSet, MSCI. DGRE (Old) weights as of 10/16/24, DGRE (New) weights as of 10/17/24, and MSCI EM Index weights as of

9/30/24. You cannot invest directly in an index.

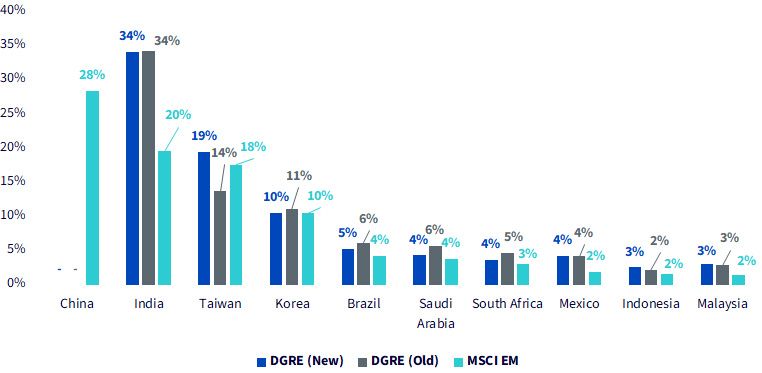

Country changes were similarly minor. The most notable change was an increase to Taiwan (-5%). The 0% China exposure and the resulting over-weight allocation to India of over 10% has been consistent since the May 2023 rebalance.

Sources: WisdomTree, FactSet, MSCI. DGRE (Old) weights as of 10/16/24, DGRE (New) weights as of 10/17/24, and MSCI EM Index weights as of

9/30/24. You cannot invest directly in an index.

We know investors are familiar with quality investing in their DM allocations. We believe DGRE offers a unique exposure to quality dividend growers in EM.

Recent knee-jerk responses to China stimulus have investors skittish about whether now is the time to dive into EM, or if the best-case scenario for China has already been priced in.

DGRE and its 0% exposure to China allows investors to access the upside potential of EM without the headache of timing a China allocation.

1 Includes both developed and emerging markets exposures.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Funds focusing on a single sector generally experience greater price volatility. Investments in emerging, offshore or frontier markets are generally less liquid and less efficient than developed markets and are subject to additional risks, such as of adverse governmental regulation, intervention and political developments. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Director, Research

Matt Wagner joined WisdomTree in May 2017 as an Analyst on the Research team. He currently serves as a Director, where he supports the creation, maintenance, and reconstitution of WisdomTree’s indexes and actively managed ETFs. Matt began his career at Morgan Stanley, working as an analyst in Treasury Capital Markets from 2015 to 2017, focusing on unsecured funding planning, execution, and risk management. He graduated magna cum laude from Boston College in 2015 with a B.A. in International Studies, concentrating in Economics. In 2020, he earned a Certificate in Advanced Valuation from NYU Stern. He is also a Chartered Financial Analyst (CFA) charterholder.