IHDG

International Hedged Quality Dividend Growth Fund

Published December 9, 2024

Equity Strategist

Few assets garnered more attention following the U.S. presidential election than the dollar, and for good reason.

The incoming Trump administration has advocated for tariffs to challenge existing U.S. trade relationships. Most of this rhetoric has been aimed at China, which could deliberately attempt to weaken its currency to mitigate such measures.

The dollar has been effectively weaponized as a result, and its upward trajectory since Election Day presents a new reality for global trade.

Since bottoming out in late September, the Bloomberg U.S. Dollar Spot Index climbed over 5.5%, with the bulk of gains coinciding with rising odds in October of a Trump victory.

The rally briefly paused immediately after Election Day before resuming its relatively unbothered ascent.

Today, the dollar is at its strongest point in two years, back when the Fed was still 150 basis points (bps) away from peak rates amid its tightening campaign, as figure 1 demonstrates.

Sources: WisdomTree, Bloomberg, as of 11/25/24. You cannot invest directly in an index.

The dollar often takes cues from interest rates, and the U.S. 10-Year Treasury yield bottomed around 3.60% before rising to 4.30–4.50%. Any new policies that cause the Fed to slow their rate cut campaign could be further support for the dollar.

But dollar volatility is not one-directional. Currencies for some of the U.S.’s largest trading partners have quickly come under pressure as well. Based on trade data from the end of 2023, all nine of the countries and regions with which the U.S. had its largest trade deficits saw their currencies decline versus the dollar in the election’s aftermath.

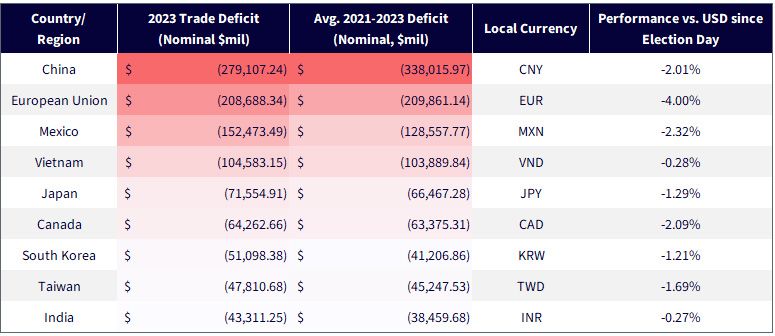

Figure 2 shows us that China remains the most notable target of Trump’s dispute, given that the U.S.’s disproportionately large trade deficit averaged well over $330 billion in the three full years since he’s been in office. The yuan renminbi (CNY) has weakened by over 2% since his re-election, matching declines in the Japanese yen (JPY). Only the euro (EUR) fared worse over this timeframe.

Sources: WisdomTree, United States Census Bureau, as of 12/31/23. Performance data sourced from Bloomberg, as of 11/26/24. Past performance is not indicative of future results.

But regional partnerships are not immune either. Trump surprised currency markets earlier this week when he newly advocated for 25% tariffs on good from Canada and Mexico. The Canadian dollar (CAD) sank to a four-year low on the news, while the peso (MXN) kept to its recent lows, remaining at its weakest since mid-2022. He also expressed support for an additional 10% tariff on Chinese goods.

Clearly, trade policy has important implications for investors as well, and the current landscape reaffirms our preference for hedging currency exposure in international equity investments.

We’ve long believed that the value of currency hedging lies in volatility reduction over return generation, but sometimes it’s possible to achieve both.

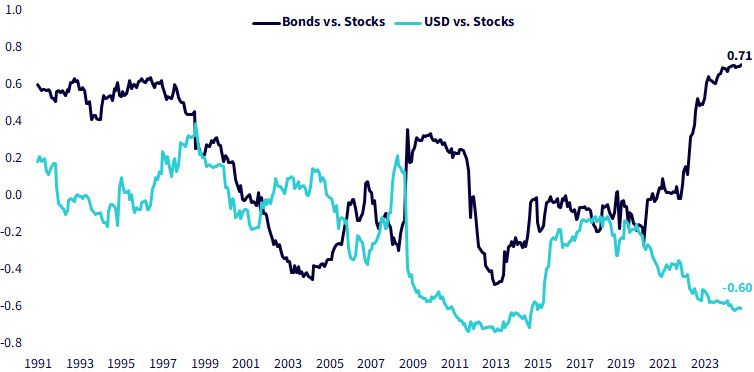

For U.S. investors, hedging international currency exposures re-establishes a long-USD and short-foreign currency position that is designed to mitigate the inherently long-foreign and short-USD position received by investing abroad. Reversing this implicit short-USD bet is especially valuable for potential risk reduction today, when, as seen in figure 3, bonds and U.S. stocks are positively correlated and the dollar is negatively correlated, making the dollar a strong equity diversifier.

Sources: WisdomTree, Bloomberg, as of 10/31/24. You cannot invest directly in an index. USD represented by the Bloomberg U.S. Dollar Spot Index. Stocks represented by the S&P 500 Index. Bonds represented by the Bloomberg U.S. Aggregate Bond Index.

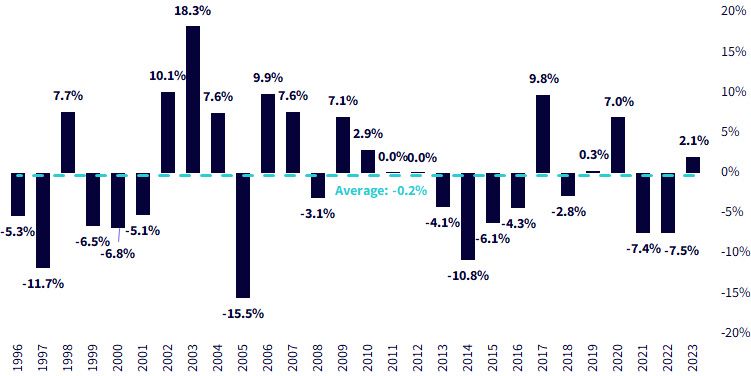

More broadly, currency hedging can reduce volatility merely by avoiding uncertainty. Figure 4 shows us that over the last 28 years, the EAFE foreign currency basket produced positive returns against the dollar only 50% of the time and provided an average return of -0.20%. Though the average is negligible, the pattern of returns exhibited little momentum or continuity from one year to the next, confirming that currencies are notoriously difficult to predict with accuracy for most investors.

Sources: WisdomTree, MSCI, as of 12/31/23. Past performance is not indicative of future results. You cannot invest directly in an index.

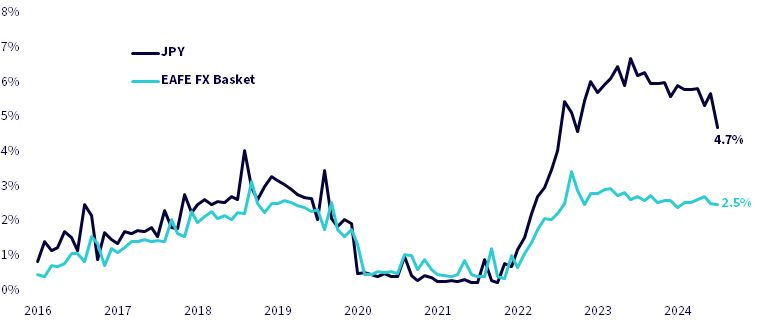

Meanwhile, diverging monetary policy continues to offer a pathway for incremental return via carry opportunities. Using current interest rate differentials, currency-hedged U.S. investors can potentially earn an extra 2.5% in their EAFE investments and 4.7% from Japanese allocations by simply hedging their foreign currency exposures, which is seen in figure 5.

Figure 5: Annualized Carry by Currency

Sources: WisdomTree, MSCI, as of 10/31/24. Carry measures the interest rate differential between the U.S. dollar and foreign currencies embedded in the difference in spot and forward FX rates. You cannot invest directly in an index.

For investments in the EAFE region, the additional volatility from unhedged currency exposure in an uncertain trade environment may not be worthwhile.

The Fund invests in high-quality international companies with the potential to grow their dividends, while hedging the attendant currency risk.

Today, this could serve the dual purpose of implementing strong dollar views while eliminating foreign currency exposures when they may be poised for volatility. The WisdomTree International Hedged Quality Dividend Growth Fund (IHDG) allows investors to earn the return of the stocks it holds in the local equity market, plus the 2.5% carry outlined above.

We view IHDG as a strategic long-term holding as part of a core international equity allocation. We believe there are benefits to currency-hedging international equity exposures that can potentially be earned over an entire market cycle, rather than as a tactical, narrow opportunity.

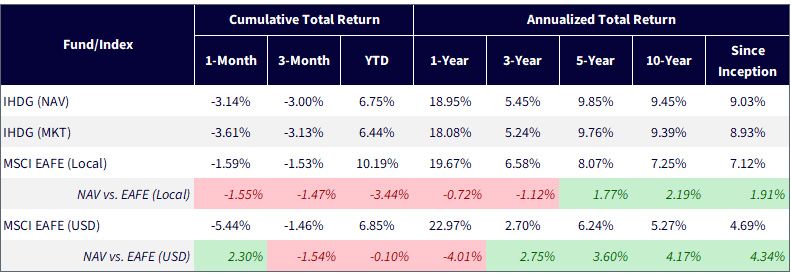

Its performance data since inception illustrates this in figure 6. Relative to USD-denominated returns for the MSCI EAFE Index, representing unhedged international equity returns, IHDG has delivered an extra 4% per year, on average, over the 5- and 10-year and since-inception periods.

Sources: WisdomTree, MSCI, as of 10/31/24. IHDG inception date = 05/07/2014. You cannot invest directly in an index. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized fund performance, click here.

The static currency hedge itself has been impactful. Comparing the returns for IHDG's underlying Index, the WisdomTree International Hedged Quality Dividend Growth Index (WTIDGH), to those of the same non-currency-hedged equity basket (represented by the WisdomTree International Quality Dividend Growth Index, WTIDG) in figure 7, shows that nearly 3% has been added per year, on average, by neutralizing FX exposures.

Sources: WisdomTree, as of 10/31/24. WTIDGH inception date = 12/02/2013. WTIDG inception date = 12/02/2013. Past performance is not indicative of future results. You cannot invest directly in an index.

Meanwhile, volatility is meaningfully reduced by the currency hedge since it eliminates FX uncertainty. Figure 8 shows that the unhedged strategy added 2%–4% incremental volatility since inception, which is entirely due to currency movements. Coupled with potential performance advantages, this may enhance the risk-adjusted returns of international allocations for U.S. investors.

Source: WisdomTree, as of 10/31/24. WTIDGH inception date = 12/02/2013. WTIDG inception date = 12/02/2013. Past performance is not indicative of future results. You cannot invest directly in an index.

In our view, currency-hedged equity strategies may be an effective way for U.S. investors to potentially find attractive returns overseas while avoiding currency pitfalls, and IHDG may be a useful method.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. To the extent the Fund invests a significant portion of its assets in the securities of companies of a single country or region, it is likely to be impacted by the events or conditions affecting that country or region. Dividends are not guaranteed and a company currently paying dividends may cease paying dividends at any time. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

International Hedged Quality Dividend Growth Fund

Equity Strategist

Brian Manby is an Equity Strategist at WisdomTree and part of the Investment Strategy team.

He is responsible for developing and communicating equity market insights, investment themes, and portfolio strategies that support the firm’s ETF and investment solutions platform. He evaluates sectors, valuations, fundamentals and equity styles to identify investment opportunities and provide actionable perspectives to clients and advisors. He also helps investors understand how WisdomTree’s equity strategies can be used to achieve long-term investment objectives in evolving market environments.

Brian joined WisdomTree in October 2018 as an Investment Strategy Analyst after a few years as a Consultant for FactSet Research Systems, Inc. He earned a B.A. in Economics and Political Science from the University of Connecticut in 2016 and has been a Chartered Financial Analyst since 2022.