Two Ways to Earn from Options: Knowing When Each Shines

Published June 18, 2026

Christopher Gannatti, CFA

Global Head of Research

Key Takeaways

- The WisdomTree Equity Premium Income Fund (WTPI) has benefited from a largely rising U.S. equity market, as its systematic S&P 500 put-writing strategy captures option premium while working alongside equities’ historical upward bias.

- Defensive covered-call strategies can help cushion drawdowns, but investors often sacrifice upside participation when markets rally strongly.

- Income investors should consider matching their option strategy to their market outlook, with put-writing generally favoring stable or rising markets and defensive covered calls offering greater protection in weaker environments.

Equity derivative income strategies1 have become increasingly accessible to a broad range of investors, and with that access comes an important question:

Not just how these strategies work, but when they work.

Two approaches worth examining sit on different ends of the equity options spectrum.

- One sells call options against a basket of defensive stocks, effectively collecting premium while capping upside.

- The other sells put options on the S&P 500 Index at a targeted premium level, twice a month, thereby accepting the obligation to buy the market if it falls far enough.

Both involve selling options. But the market environments where each tends to thrive are quite different, and understanding that distinction can be quite important.

The Defensive Covered Call: Built for Caution

When a strategy sells call options on a basket of defensive equities, which could include stocks in such sectors as utilities, consumer staples, healthcare, it is, by design, comfortable giving up the upside in exchange for reliable premium income.

That trade-off is most rewarding when the broader equity market is grinding sideways or drifting modestly lower.

In those environments, the underlying stocks hold their value relatively well (being defensive), the premium collected cushions any mild drawdowns, and the capped upside isn't much of a penalty because there isn't much upside to cap.

This structure also tends to perform with more dignity during a genuine market correction. Defensive sectors, at least judging by history, don't tend to fall as hard as the broader index, and many would indicate that's the rationale for owning them, and the rolling premium from sold call options may provide an additional layer of cushion. An investor holding this kind of strategy heading into a 15% drawdown in the S&P 500 might experience something meaningfully softer, not because it is immune to losses, but because the combination of defensive equity selection and premium income absorbs some of the blow.

Where this strategy pays a price is in strong, sustained bull markets. When the S&P 500 Index charges higher, as U.S. equities have historically done over long periods, a portfolio anchored in defensive stocks with capped upside will, most likely, lag. The premium income, however consistent, rarely compensates fully for the opportunity cost of missing a powerful rally in cyclical or growth-oriented sectors.

The Index Put Sale: A Bet on Stability and the Upside Bias

Selling puts on the S&P 500 Index at a fixed premium target, executed on a regular cadence, is a fundamentally different posture. Rather than owning equities and capping their gains, this approach holds cash (or cash-like instruments) and collects premium for agreeing to absorb market downside below a certain level.

When nothing dramatic happens, meaning:

- When the market drifts upward

- Trades flat

- Declines only modestly

Then, the puts expire worthless and the premium is kept. Over time, in a market that tends to rise, this can be a productive engine.

The historical upward bias of U.S. equity markets is, in fact, this strategy's closest ally. Equities have tended to, historically, rise more often than they have tended to fall. While this can never be guaranteed to continue looking forward, recognizing historical trends is important. Corrections happen, but they have, historically, been more episodic and usually shorter in duration than the periods of calm that precede and follow them.

A strategy that systematically collects put premium in a market environment defined by that pattern is working with a structural tailwind. The twice-monthly cadence reinforces this, and rather than making a single large bet, it harvests premium across many short windows, allowing the law of large numbers to work in its favor.

The vulnerability, however, is real and worth stating plainly:

A sharp, sudden market decline is the scenario where selling index puts becomes uncomfortable quickly.

Unlike the covered call strategy, which already owns defensive equities and absorbs the drop through their relative resilience, the put-selling approach is directly exposed to a steep drawdown in the index. If the market falls hard enough to breach the strike prices of the sold puts, losses can be significant, and the twice-monthly execution means there is limited time between trades to react.

Conclusion: Let’s Look at Some Live Performance History

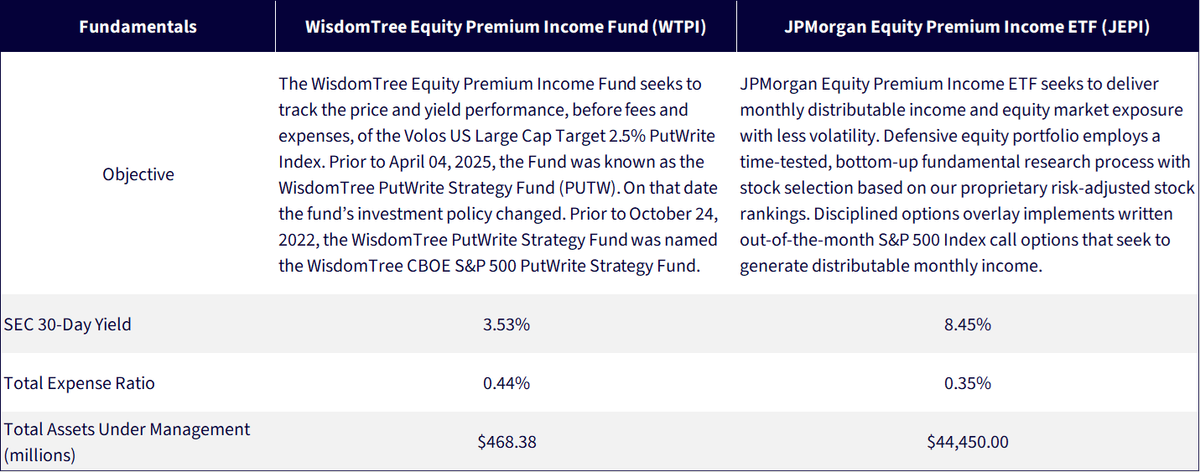

While, conceptually, this may make sense, it’s important to test these ideas with real strategies. The JPMorgan Equity Premium Income ETF (JEPI) is the largest strategy within the Morningstar US Fund Derivative Income Category.2 We can compare this to the WisdomTree Equity Premium Income Fund (WTPI), which is also in this category.

The fund methodologies are as follows:

- WisdomTree Equity Premium Income Fund (WTPI) seeks to track the Volos U.S. Large Cap Target 2.5% PutWrite Index, which runs a systematic, collateralized put-writing strategy on the S&P 500 Index. At any given time, the index holds two S&P 500 put options, written at whichever strike price is either at-the-money or carries a premium closest to 2.5%, with expirations targeting the first or third Friday of the following month. This twice-monthly rolling cadence is designed to generate more consistent premium income than a standard monthly approach. Proceeds are held in 3-month Treasury Bills, keeping the strategy fully collateralized. The fund aims to make monthly distributions.

- JPMorgan Equity Premium Income ETF (JEPI) combines two distinct building blocks: a defensive equity portfolio and a disciplined options overlay. The equity sleeve employs a bottom-up, fundamental research process that uses proprietary risk-adjusted stock rankings to construct a diversified portfolio of U.S. large cap stocks tilted toward lower volatility. The options overlay writes out-of-the-money call options on the S&P 500 Index on a monthly basis, generating premium income that supplements dividend income from the equity holdings. The strategy is designed to deliver monthly income while maintaining less volatility and lower beta relative to the broader U.S. equity market.

We now have two funds, representing two fundamentally different approaches to selling options on an exposure to U.S. equities, that we can compare to the S&P 500 Index.

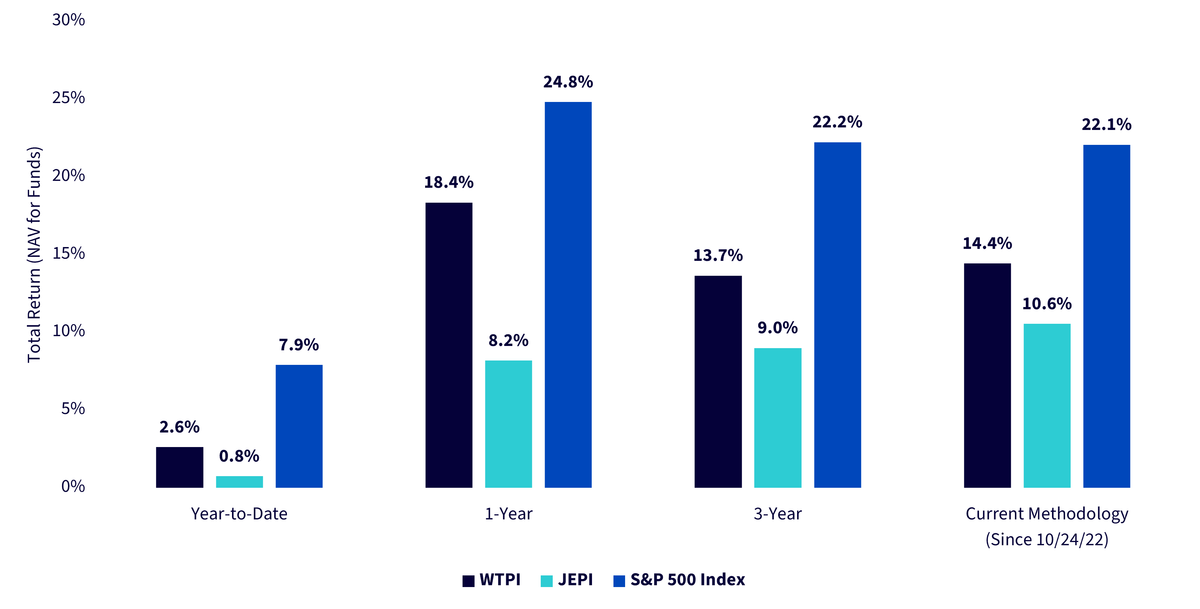

The big picture, and we see this in Figure 1a, is that, for the most part, U.S. equity market performance, shown through the S&P 500 Index, has been strong. A strong, largely upward-trending market should favor WTPI over JEPI, and that is what we have observed. In certain sharp, short-term, drawdowns that have occurred in this longer period, it’s absolutely true that JEPI did outperform, but this was again, short. Since there were not sustained negative market environments, a focus on lower volatility stocks has not been the way to keep pace with the S&P 500 Index.

We can also note that, to be fair, WTPI also did not keep pace with the S&P 500 Index, but this should not be expected in a largely upward trending performance environment.

Figure 1a: Comparing Distinct Option-Writing Strategies over Live Performance

Figure 1b: Standardized Returns

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of May 20, 2026, but showing returns for the period ended May 19, 2026 for Figure 1a and March 31, 2026 for 1b. Prior to April 4, 2025, WTPI was known as the WisdomTree PutWrite Strategy Fund (PUTW). On that date, the Fund’s investment policy changed. Prior to October 24, 2022, the WisdomTree PutWrite Strategy Fund was named the WisdomTree CBOE S&P 500 PutWrite Strategy Fund and tracked the total return performance, before fees and expenses, of the CBOE S&P 500 PutWrite Index. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

We respect that we do not have the proverbial crystal ball and do not know exactly what type of equity market will be coming next. However, we would note that investors should align their views and objectives, as well as the market they want to be prepared for, with their underlying strategy.

Figure 2: Additional Information

Sources: Individual fund sponsor website pages at WisdomTree and JPMorgan. Data for assets under management is as of 5/19/2026. Subject to change.

1 Referring to the Morningstar US Fund Derivative Income Category.

2 Assets under management measured as of 4/30/26.

Categories

Related articles

Two Roads to Less Volatile U.S. Equity Returns

Adding, Not Replacing: Managed Futures in the Age of Efficient Capital

Adding, Not Replacing: Broad Commodities in the Age of Efficient Capital

Rebalancing for a Fragmenting World: Why Broad Commodities Still Matter

Shockwaves: How an Energy Crisis Spreads Across Commodities

Inflation Fears Are Rising Again. WTIP Was Ready.

Private Credit Jitters and Their Impact on the Broader Macroeconomy

Oil Markets Face a Supply Shock—and the Offsets Aren’t Enough

Navigating a Structurally More Fragile Market Cycle

About the contributor

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.