Loosening YCC Will Not Stop Japanese Stocks’ TINA Appeal

Published August 14, 2023

Jeff Weniger, CFA

Head of Equity Strategy

One of the main reasons the MSCI Japan Index has rallied by 14% in 2023 is the country’s status as the last remaining “TINA” holdout. According to the TINA concept, stocks are to be purchased when There Is No Alternative, which is shorthand for something like “buy stocks because bond yields stink.” But if government bonds are throwing off 3% or 4% yields, as is now the case in the U.S., Canada and most of Europe, suddenly stocks don’t look as enticing as they did a few years back when many of those bonds were in negative yield territory.

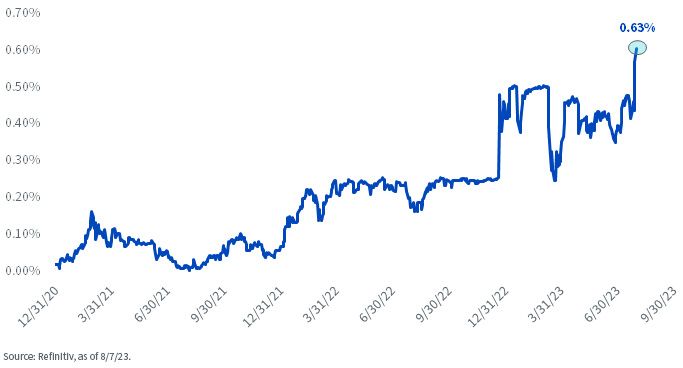

Until recently, the 10-year Japanese government bond (JGB) was bopping around at levels south of 0.50%, the upper boundary of the Bank of Japan’s (BoJ’s) +/-50 basis points (bps) window around a 0% target. While the vibe is that the benchmark JGB was itching to explode through 0.50%, with only the BoJ preventing it, I want to take great pains to point out that it wasn’t like the 10-year was spending most of this year at 0.49% or 0.50%. To the contrary, for large chunks of this year you could pull a yield quote and it would be in the low-40s. That fact seems lost on many observers, who seem to have it in their mind that the selling impulse on JGBs was at some boiling point.

There was pressure, no doubt, but I’m not sure it was as bold as commonly believed. Granted, the 50-bps band was a bit new; for several years, the yield curve was considered to be in control so long as bond yields never hopped outside of -0.25% or +0.25%.

Nevertheless, with global bond markets all over the place in the last couple years—and by “all over the place,” I mean being sold—the BoJ was put into a tough bind as rates jumped in the other six members of the G7. A few weeks ago, the BoJ got cornered and made the decision that was being whispered loudly for a while before it happened—to let 0.50% get pierced to the upside (figure 1). The new terminology: 0.50% is a “reference rate,” a guidepost, not a line in the sand.

Up through 0.50% the JGB yield went. You can see the little pop at the end of figure 1.

Figure 1: 10-year Japanese government bond yield (%)

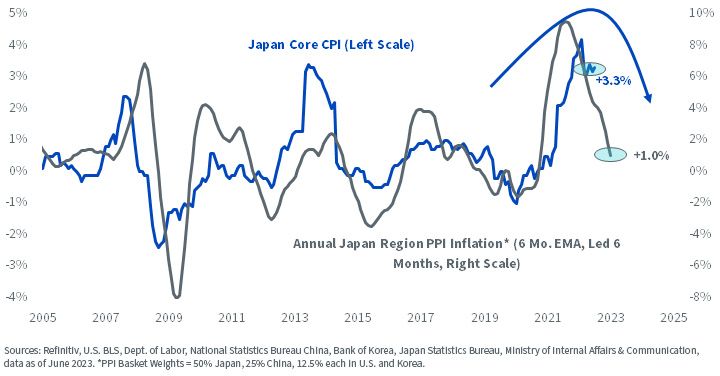

The BoJ is going to get lucky, I believe, and it’s not from any genius policy moves or anything like that. It’s a right place at the right time situation. So many global PPIs are tumbling, ostensibly as the global economy deteriorates.

I have reason to believe that we have seen the peak in Japan’s Core CPI, at least as far as 2023 and early 2024 are concerned. Using an amalgamation of Japan’s PPI, along with the PPIs of its major trade partners, there appears to be a gravitational pull in consumer price inflation in the next quarter or two. I will not be stunned in the slightest if the coveted 2% inflation target gets breached to the downside (figure 2).

Figure 2: Japan’s Core CPI has downside risk

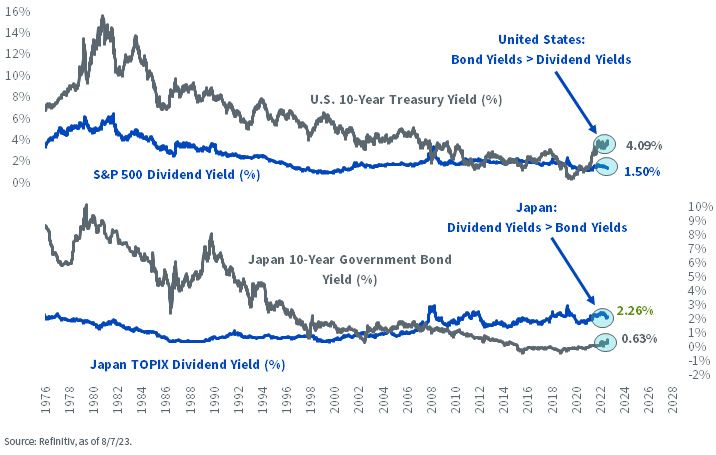

As far as TINA is concerned, figure 3 shows why this yield backup only matters around the edges.

Consider, for one, the death of TINA in the U.S.

The last generation or so, which I’ll date to the global financial crisis, has witnessed the S&P 500’s dividend yield clocking in sometimes higher, sometimes lower than the 10-Year U.S. T-note yield. The bond market bear, which celebrated a second birthday the other day, changed that situation notably; the Treasury yield has popped to around 4%, while the ruthlessly rallying S&P’s dividend yield has withered to 1.50%. It makes you think a little when your head hits the pillow and you’re in an 80/20 or a 70/30, with most of that equity in U.S. stocks.

In contrast, most of the last generation saw Japan’s stock-versus-bond math flip the other way around from the situation in the U.S. While TINA died for the S&P 500, in Japan it’s as strong as ever. If I have this right and the BoJ feels compelled to stop the bond market at something like 1% yields—or JGBs don’t even get there, then an overweight allocation in TINA-based Japan looks like a solid argument.

Figure 3: TINA no vs. TINA yes

Categories

Related articles

Japan Is Back

From Trading Houses to Tokio Marine: Buffett’s Expanding Bet on Japan

A Playbook for the Currency Opportunity in Today’s Market

Tariffs Are (Sort of) Done: What the Supreme Court Ruling Means for Markets

Japan’s Moment: Elections, Flows & Global Opportunities

An Update on the Japan Opportunities

The Power of Hedging in a Year of Yen Swings

The Power of Framing a Story in Investing

Japan's Equities Are Seeing a Performance Acceleration

About the contributor

Jeff Weniger, CFA

Head of Equity Strategy

Jeff Weniger, CFA, has been with WisdomTree since 2017 and serves as the Head of Equities. He shapes the firm’s market outlook through a combination of macroeconomic and fundamental analysis. With more than two decades in investment strategy, Jeff is known for his work on market cycles and valuations. Before joining WisdomTree, Jeff was with BMO Private Bank and BMO Global Asset Management for 11 years. At BMO, he sat on the firm’s Asset Allocation Committee and co-managed ETF model portfolios across the U.S. and Canada. In 2013, at age 32, he became the youngest member of BMO’s Global Investment Forum. When he left BMO to come to WisdomTree, his final role was Director, Senior Strategist in the Office of the CIO in 2017.

Jeff is a frequent television guest on networks such as CNBC, Bloomberg, and Schwab, with regular print appearances in The Wall Street Journal, Barron’s and Reuters. He also appears weekly on the Behind the Markets podcast and is a regular on SiriusXM’s The Business Briefing. On X, Jeff has developed one of the larger followings in financial media. He earned a B.S. in Finance from the University of Florida and an MBA from the University of Notre Dame. He has held the CFA charter since 2006.