Looking Abroad for Dividend Income

Published April 14, 2022

Matt Wagner, CFA

Director, Research

Value has trounced growth globally this year. High dividend yield companies, which tend to have high overlap with value indexes, have also outperformed.

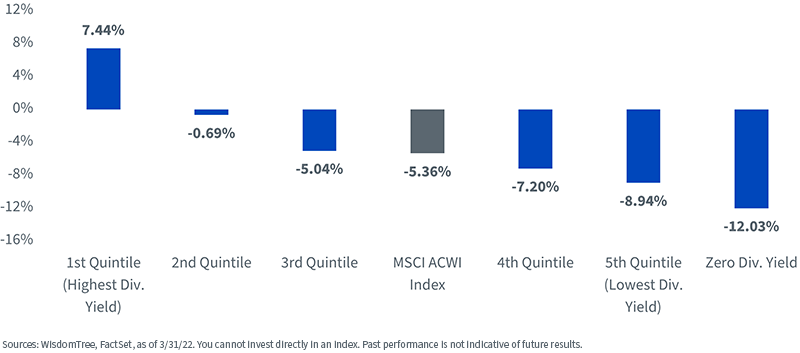

The first quintile of companies in the MSCI ACWI Index by dividend yield has outperformed the fifth quintile by over 1,600 basis points (bps) and outperformed non-payers by over 1,900 bps.

Year-to-Date MSCI ACWI Index

Many investors are familiar with investing in search of dividend income when allocating to U.S. equities. Some may be less familiar with the global dividend investment opportunity—particularly when it comes to emerging markets.

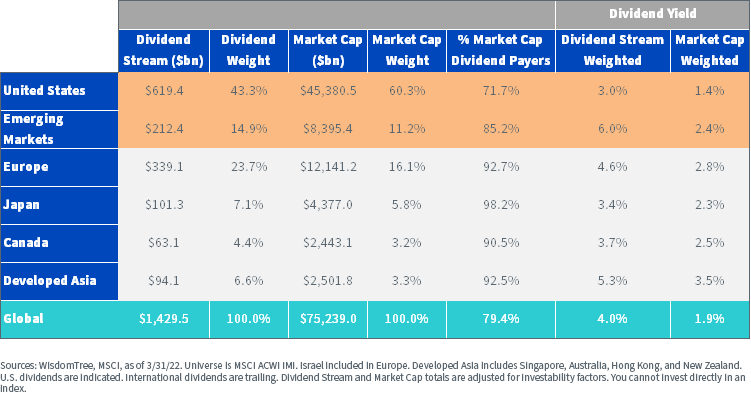

The below table summarizes some key data points for dividend payouts across the globe.

Of the $1.4 trillion in the global Dividend Stream, $216 billion, or 15%, comes from companies within emerging markets. That amount is just over 3.5% greater than the 11.5% weight that emerging markets have in the market cap-weighted MSCI ACWI IMI Index.

The U.S., on the other hand, comprises just 43% of the global Dividend Stream but accounts for 60% of market cap. In part that is because the U.S. has higher valuations, and much less of its market cap weight is in companies paying a dividend.

In emerging markets, 85% of the market cap is in companies paying dividends. In the U.S., the comparable number is just 72%.

As a result of the lower weight of companies paying a dividend, the U.S. has a dividend yield of just 1.4%—a full 100 bps lower than the yield of emerging markets.

The difference is even greater when weighting companies by their Dividend Stream instead of market cap. The emerging markets has a Dividend Stream-weighted yield of 6% compared to just 3% for the U.S.

Global Dividend Stream

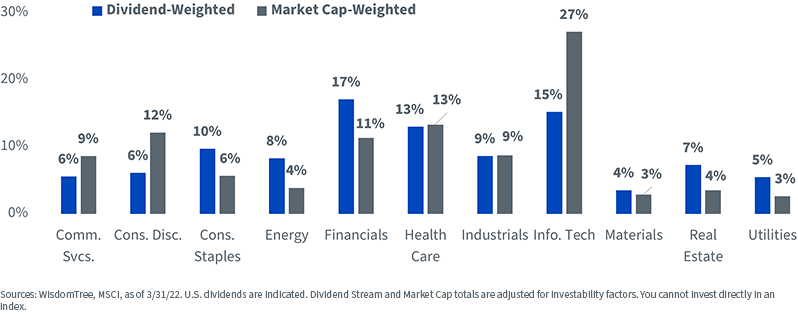

We can break down the U.S. and emerging markets market-cap weights and Dividend Stream weights on a sector level to get an indication of where dividend payouts are more concentrated.

In the U.S., the largest dividend sectors are Financials (17%), Information Technology (15%), Health Care (13%) and Consumer Staples (10%).

Sector Weights: Market Cap-Weighted vs. Dividend-Weighted (MSCI USA IMI Index)

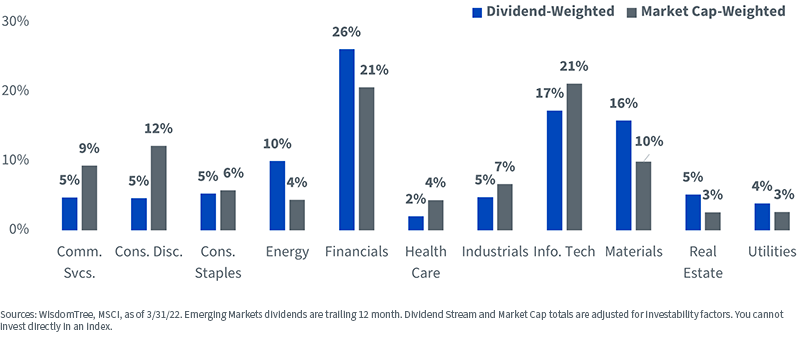

In the emerging markets, the largest dividend sectors are Financials (26%), Materials (16%), Information Technology (17%) and Energy (10%).

The combined dividend weights of Materials and Energy (26%) make a dividend-weighted exposure to emerging markets much more commodity-sensitive than the tech- and consumer-heavy allocations of market cap-weighted emerging markets exposures.

Sector Weights: Market Cap-Weighted vs. Dividend-Weighted (MSCI Emerging Markets IMI Index)

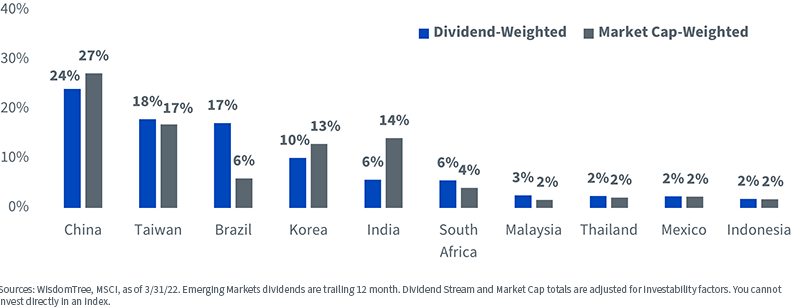

From a country perspective, China and India have noticeably lower weights based on dividend weighting. Many Chinese tech and consumer companies pay little, or no, dividends. In India, there is a tendency for low dividend payouts/yields.

Brazil is the most noticeable overweight given its large dividend-paying Energy and Materials companies. Russia was recently removed from MSCI indexes for its invasion of Ukraine but historically had been another overweight based on its large dividend payouts.

Country Weights: Market Cap-Weighted vs. Dividend-Weighted (MSCI Emerging Markets IMI Index)

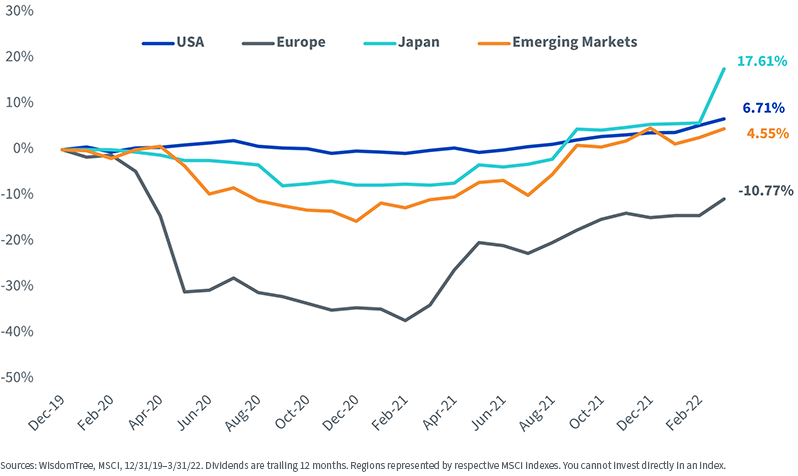

The global recession during the height of the COVID-19 pandemic provides a good case study as to the relative riskiness of the payouts from emerging markets companies.

Emerging markets dividends did get reduced more than U.S. dividends, but also rebounded sharply in the past 12 months. European dividends, not emerging markets, stick out as the global laggard in reducing payouts during the pandemic.

Index Dividend Growth since 2019

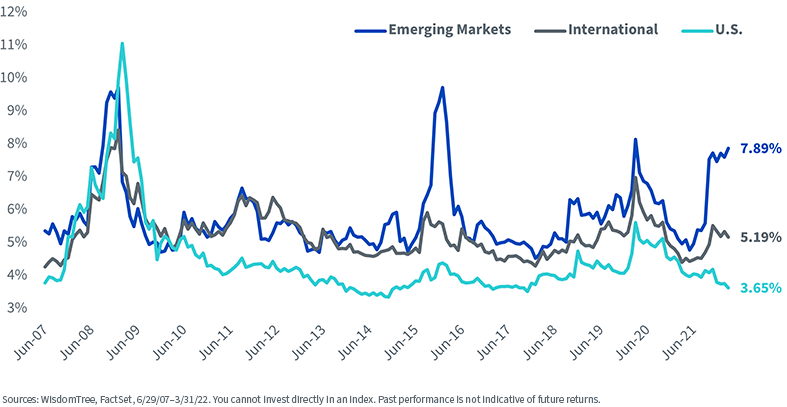

Lastly, we can compare the yields across markets to get an idea of how investors can look to emerging markets to harvest income in a low-rate environment.

The WisdomTree Emerging Markets High Dividend Index has historically had an average yield premium of 130 bps relative to the WisdomTree U.S. High Dividend Index, and a yield premium of about 50 bps relative to the WisdomTree International High Dividend Index.

For investors looking to increase dividend income, emerging markets equities may offer a compelling addition to portfolios in a low-yield environment.

Trailing 12-Month Dividend Yields: WisdomTree High Dividend Yield Indexes

Categories

Related articles

Dividend Growth Is Not One Strategy

Beyond Market Cap: A Nearly 19-Year Case for Dividend-Driven Emerging Markets

Quality as a Foundation in an Uncertain World

Value Isn’t What It Used to Be

Don’t Mistake Speculation for Strength: The Mirage of Small-Cap “Junk” Outperformance

From Momentum to Discipline: Navigating Volatility in Emerging Markets

A Rebalance Review for U.S. Large-Cap Dividends

The Discipline of Dividends: Capturing Value in U.S. Large Caps

A Review of Our 2025 Global Dividend Rebalance

About the contributor

Matt Wagner, CFA

Director, Research

Matt Wagner joined WisdomTree in May 2017 as an Analyst on the Research team. He currently serves as a Director, where he supports the creation, maintenance, and reconstitution of WisdomTree’s indexes and actively managed ETFs. Matt began his career at Morgan Stanley, working as an analyst in Treasury Capital Markets from 2015 to 2017, focusing on unsecured funding planning, execution, and risk management. He graduated magna cum laude from Boston College in 2015 with a B.A. in International Studies, concentrating in Economics. In 2020, he earned a Certificate in Advanced Valuation from NYU Stern. He is also a Chartered Financial Analyst (CFA) charterholder.