CXSE

China ex-State-Owned Enterprises Fund

Published January 15, 2026

Research Analyst

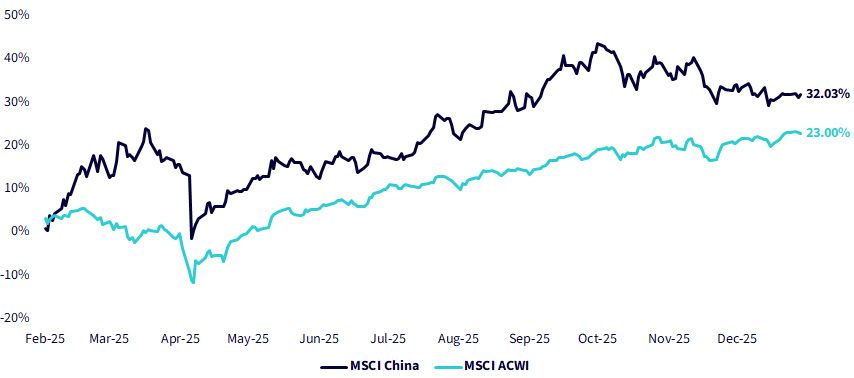

After years of uncertainty and underperformance, Chinese equities delivered a strong rebound in 2025. Improvements in investor sentiment—supported in part by advances in AI and semiconductor technology—helped rebuild confidence, while the MSCI China Index reached decade-high levels late in the year.

MSCI China Index and MSCI ACWI Index Year-to-Date Total Local Returns

Source: WisdomTree, MSCI, FactSet. Returns from 12/31/2024-12/31/2025. Past performance is not indicative of future results. You cannot invest directly in an index.

Policymakers implemented a series of targeted monetary, fiscal, and capital-market measures aimed at stabilizing growth and restoring confidence. Unlike past cycles, these actions were incremental and focused on risk containment rather than broad-based reflation.

Even so, China's equity gains in 2025 were not merely a policy-driven rally. Valuations began the year at deeply discounted levels, and as investor confidence improved, equities were repriced higher, narrowing the gap versus global markets.

Beyond policy support, investor sentiment has also been lifted by the resilience of China's technology sector and a faster-than-expected easing of U.S.-China tariff frictions. Plans for multiple high-level meetings between the two countries' leaders in 2026—potentially as many as four—have added to a sense of improving dialogue. A modest appreciation of the renminbi may also provide a tailwind for Chinese equities.

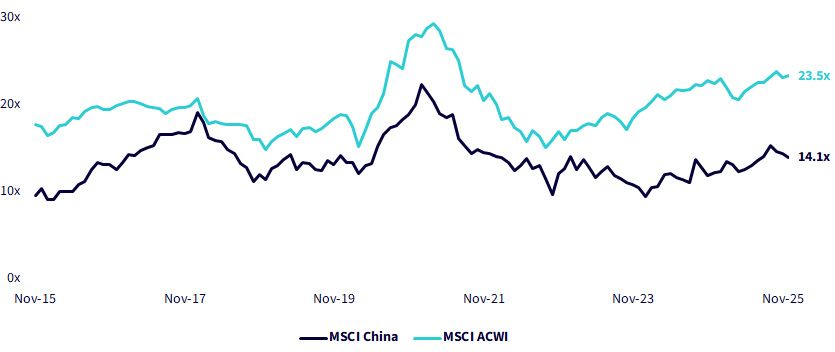

Even after this repricing, Chinese equities continue to trade at meaningful discounts relative to global equities, as measured by the MSCI ACWI Index. While valuation remains supportive, the renewed interest in China has been driven less by absolute cheapness and more by confidence in the resilience of its technology sector and supply-chain positioning.

Source: WisdomTree, MSCI, FactSet. Data from 11/30/2015-12/31/2025. Past performance is not indicative of future results. You cannot invest directly in an index.

At the company level, Chinese equities continue to trade at marked valuation discounts, most notably relative to U.S. equities. The largest constituents of the MSCI China Index trade at substantially lower forward multiples than those of the S&P 500, despite stronger forward earnings growth expectations.

Source: WisdomTree, S&P, MSCI, FactSet. Data as of 12/31/2025. Past performance is not indicative of future results. You cannot invest directly in an index.

Importantly, China's rebound has not been uniform across ownership structures. Government ownership can meaningfully influence corporate priorities, often creating trade-offs between policy objectives and shareholder outcomes.

WisdomTree's ex-State-Owned Enterprises approach focuses on companies with limited government ownership, where firms tend to operate with greater autonomy and stronger alignment with market incentives. By excluding state-owned enterprises (SOEs), this framework seeks to reduce governance and capital-allocation risks.

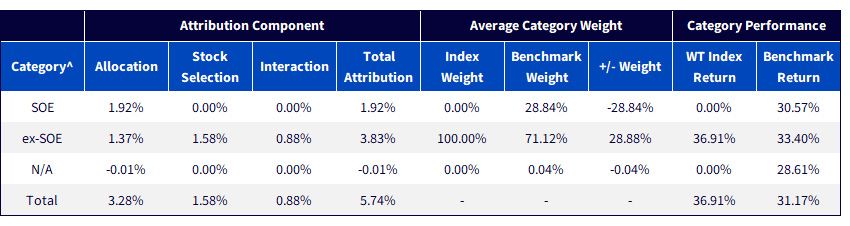

The WisdomTree China ex-State-Owned Enterprises Index, tracked by the WisdomTree China ex-State-Owned Enterprises Fund (CXSE), has had a very strong year in 2025, outperforming its benchmark, the MSCI China Index, by 574 basis points year-to-date. Most of this outperformance can be attributed to its overweight to non-SOEs (ex-SOEs) and underweight to SOEs, with 328 basis points of attribution driven by allocation effects.

Source: WisdomTree, MSCI, FactSet. Returns from 12/31/2024-12/31/2025. Past performance is not indicative of future results. You cannot invest directly in an index.

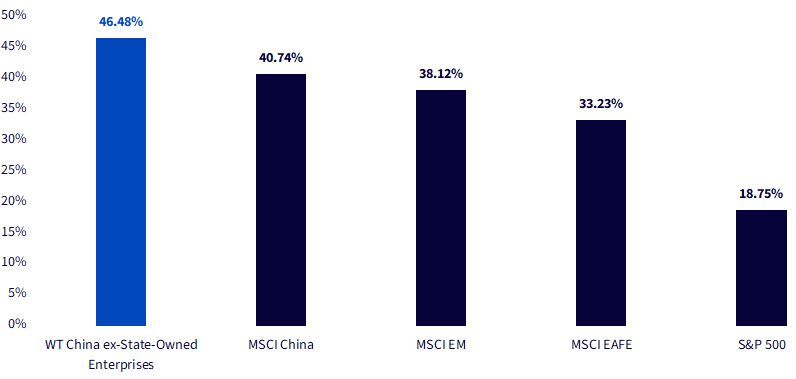

CXSE's outperformance has not been limited to China benchmarks alone. In 2025, the strategy also outperformed developed and emerging market peers, underscoring that its results were not simply a byproduct of China's rebound, but of how exposure was constructed.

Source: WisdomTree, S&P, MSCI, FactSet. Returns from 12/31/2024-12/31/2025. You cannot invest directly in an index. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

China's experience in 2025 underscores that how investors gain exposure matters as much as whether they do. As valuations reset and confidence improved, performance dispersion reflected ownership structure and governance differences. CXSE's construction—tilting away from state ownership and toward market-oriented companies—has been well aligned with those dynamics.

Looking ahead, the U.S.–China relationship does not appear to be deteriorating, and China's technology sector has remained resilient. China's equity market is likely to continue to be defined by uneven macroeconomic recovery and meaningful dispersion. Investing in Chinese equities therefore requires a long-term view on China's technology sector, which is largely non-state owned. In that environment, strategies that emphasize governance, capital discipline, and market incentives may be better positioned to navigate ongoing uncertainty. CXSE offers one such approach for investors seeking a more selective way to access China's equity opportunity.

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in China, including A-shares, which include the risk of the Stock Connect program, thereby increasing the impact of events and developments associated with the region which can adversely affect performance. Investments in emerging or offshore markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. The Fund’s exposure to certain sectors may increase its vulnerability to any single economic or regulatory development related to such sector. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

China ex-State-Owned Enterprises Fund

Research Analyst

Hyun Kang joined WisdomTree in July 2022 as a Research Analyst. As a part of the Index team, he assists with the creation and maintenance of the firm’s indexes and supports the group’s research initiatives across various strategies. Hyun graduated from Carnegie Mellon University, with a B.S. in Business Administration and an additional major in Statistics and Machine Learning.