NTSX

U.S. Efficient Core Fund

Published July 15, 2026

Global Chief Investment Officer

Director, Model Portfolios

In our prior blog, we revisited the original case for the WisdomTree US Efficient Core Fund (NTSX) in the context of today’s evolving interest rate environment. After a period when stocks and bonds struggled together, the setup for bonds appears more constructive: yields are higher, real yields are positive, and duration may again have a better chance of serving as a hedge if the dominant macro risk shifts from inflation surprise to growth disappointment.

That matters because NTSX was built on the simple but powerful idea that a diversified portfolio can provide a stronger foundation than a 100% equity allocation.

But that is only the first chapter.

For advisors and allocators, the practical evolution is how NTSX and other capital-efficient ETFs can serve as total portfolio tools that deliver target core exposures with smaller capital allocations.

This can create room for other differentiated, complementary investment strategies such as commodities, managed futures, long/short equity or alternative income. Importantly, these new return streams can be added without forcing investors to make the usual trade-off of selling stocks or bonds to fund them.

The Funding Problem

Most investors understand the appeal of diversification.

They want more than one way to make money. They want parts of the portfolio that can respond differently to macro forces such as economic growth, inflation, currency movements, or commodity shocks.

But diversification has a funding problem.

In a traditional portfolio, every dollar allocated to a diversifying strategy has to come from somewhere else.

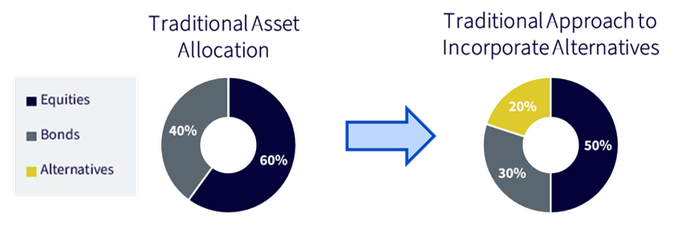

In the example below, a 60/40 portfolio that adds a 20% diversifying sleeve might become a 50/30/20 portfolio.

Figure 1: Portfolio Paradox: Incorporating Alternatives Has Historically Required Reducing Core Equity and/or Bond Exposures

Source: WisdomTree. For illustrative purposes only.

As a result, the diversifying sleeve is often forced to compete psychologically with the S&P 500 during strong equity markets. And if the funding comes from fixed income, investors may also be giving up income, liquidity and the potential recession sensitivity that bonds can provide.

That combination can make even a well-designed, more efficient portfolio look worse than a traditional allocation during periods when stocks and bonds are both performing well.

It is one of the reasons diversifying strategies are often difficult for allocators and individual investors to stick with for long periods of time, and why they are so often sold right before they are needed most.

Compress the Core, Then Build Around It

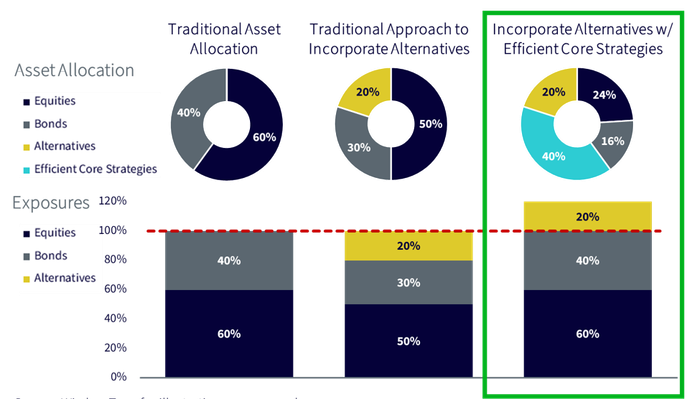

The capital-efficient framework starts with a simple observation: the capital allocation and the economic exposure of a portfolio are not always the same thing.

A traditional 60/40 portfolio uses 100% of the capital to get 60% equity exposure and 40% bond exposure.

A capital-efficient ETF can seek to deliver a similar stock/bond exposure profile using less than 100% of the portfolio’s capital. The remaining capital can then be used for other strategies.

Consider the same example above. Instead of funding a 20% alternatives allocation by reducing core stock and bond holdings, investors can use capital-efficient ETFs to maintain their desired 60/40 exposure with less invested capital. The capital that is freed up can then be allocated to alternative investments and diversifying strategies. As a result, the portfolio can retain its full 60/40 core exposure while also adding a 20% allocation to alternatives—in effect achieving a 60/40/20 portfolio rather than diluting the core into a 50/30/20 allocation.

Figure 2: Efficient Core Strategies Allow Investors to Incorporate Alternatives Without Reducing Their Existing Stock and Bond Allocations

Source: WisdomTree. For illustrative purposes only.

This is where the use case becomes especially important for model portfolios.

If the portfolio can maintain its intended 60/40 exposure while also creating room for alternatives, the diversifying sleeve does not need to beat equities in a bull market to be valuable. It needs to earn a return above cash (effectively the funding cost of the capital efficiency), behave differently from stocks and bonds, and provide a return stream that can help in environments where the traditional portfolio is more challenged.

That is a much more realistic standard for most alternative investment strategies.

It may also be a more repeatable way to improve model portfolio performance than relying solely on active manager selection inside core equity allocations. Finding active managers who can consistently deliver alpha after fees is difficult. Identifying them in advance and sticking with them through inevitable periods of underperformance is even harder.

By contrast, using capital-efficient ETFs to preserve core exposures while adding diversifying return streams is a portfolio construction decision. Instead of finding one manager who can beat the market every year, advisors can build a portfolio with more than one way to generate returns.

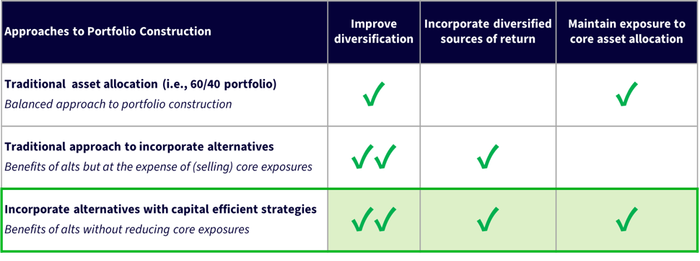

Figure 3: Capital-Efficient Portfolio Construction Delivers Diversification Without Sacrificing the Core

Source: WisdomTree. For illustrative purposes only.

Real Portfolio Example

Start with a traditional 60/40 ETF portfolio. Now make the core exposure more capital efficient.

Figure 4: Example Portfolio: Using Capital Efficiency to Add Diversifying Return Streams

Source: WisdomTree. For illustrative purposes only.

In this example, we use the WisdomTree US Efficient Core Fund (NTSX) as the core holding. Because NTSX provides stock and bond exposure in a more capital-efficient structure, it creates room in the portfolio for other diversifying return streams.

We use that freed-up space to add alternatives through a combination of the WisdomTree Managed Futures Strategy Fund (WTMF) and the WisdomTree Enhanced Commodity Strategy Fund (GCC).

The goal is simple: keep the familiar 60/40 foundation, but use capital efficiency to expand the opportunity set.

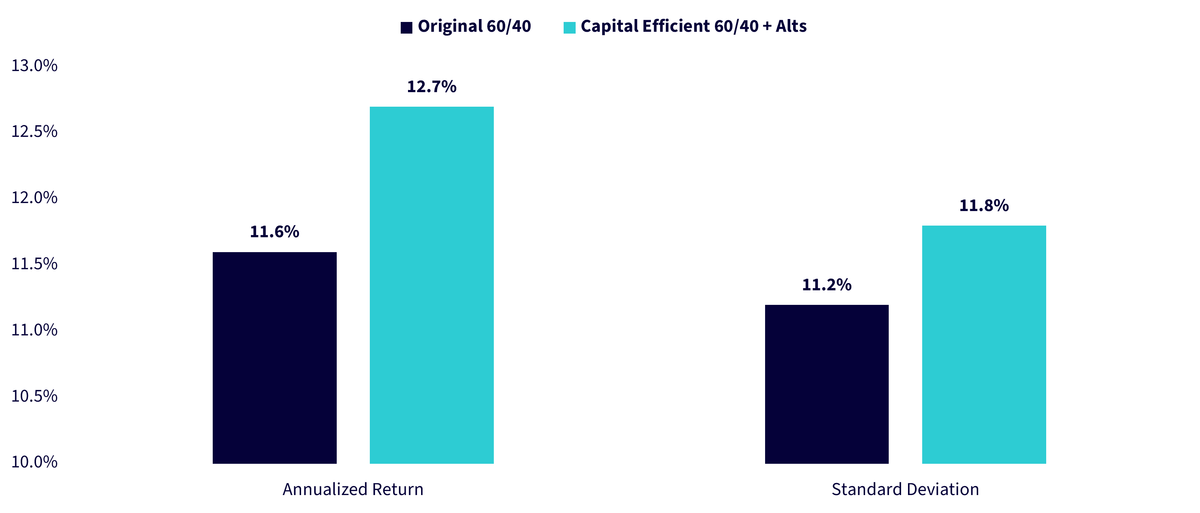

Using January 2019 as the starting point, which corresponds with the inception date of NTSX, the results show how this approach can help investors add diversified return drivers while maintaining a similar volatility profile.

Figure 5: Capital Efficiency Expanded Return Drivers While Maintaining a Similar Risk Profile

Source: WisdomTree; as of May 31, 2026. Inception date: January 1, 2019, based on the inception date of NTSX.

As demonstrated in this example, capital efficiency does not have to mean taking significantly more risk. It can mean making the same risk budget work harder.

Stocks remain the long-term growth engine. Bonds can provide income and potential ballast. Alternatives can add exposures tied to different market environments. Capital-efficient ETFs can help make room for all three.

That is the next step beyond 60/40: not abandoning the traditional portfolio but using capital efficiency to build more around it.

There are risks associated with investing including possible loss of principal. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

NTSX: While the Fund is actively managed, the Fund’s investment process is heavily dependent on quantitative models and the models may not perform as intended. The Fund invests in derivatives to gain exposure to U.S. Treasuries. The return on a derivative instrument may not correlate with the return of its underlying reference asset. The Fund’s use of derivatives will give rise to leverage and derivatives can be volatile and may be less liquid than other securities. As a result, the value of an investment in the Fund may change quickly and without warning and you may lose money. Interest rate risk is the risk that fixed income securities, and financial instruments related to fixed income securities, will decline in value because of an increase in interest rates and changes to other factors, such as perception of an issuer’s creditworthiness.

WTMF: An investment in this Fund is speculative, involves a substantial degree of risk, and should not constitute an investor's entire portfolio. One of the risks associated with the Fund is the complexity of the different factors which contribute to the Fund's performance, as well as its correlation (or non-correlation) to other asset classes.

These factors include use of long and short positions in commodity futures contracts, currency forward contracts, swaps and other derivatives. In addition, bitcoin exchange-traded products (ETPs) and bitcoin futures are relatively new and the markets may be less developed. They are subject to unique and substantial risks, and historically, have been subject to significant price volatility. As a result, the markets for bitcoin futures and bitcoin ETPs may be less developed, and at times, potentially less liquid and more volatile, than more established commodity futures and ETP markets. While the bitcoin futures market has grown substantially since bitcoin futures commenced trading, there can be no assurance that this growth will continue. Derivatives can be volatile and may be less liquid than other securities and more sensitive to the effects of varied economic conditions.

The Fund should not be used as a proxy for taking long only (or short only) positions in commodities or currencies. The Fund could lose significant value during periods when long only indexes rise (or short only) indexes decline. The Fund's investment objective is based on historic price trends. There can be no assurance that such trends will be reflected in future market movements. The Fund generally does not make intra-month adjustments and therefore is subject to substantial losses if the market moves against the Fund's established positions on an intra-month basis. In markets without sustained price trends or markets that quickly reverse or "whipsaw" the Fund may suffer significant losses.

The Fund is actively managed thus the ability of the Fund to achieve its objectives will depend on the effectiveness of the portfolio manager. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. The Fund will not invest in bitcoin directly.

GCC: An investment in this Fund is speculative, involves a substantial degree of risk, and should not constitute an investor's entire portfolio. One of the risks associated with the Fund is the complexity of the different factors which contribute to the Fund's performance. These factors include use of commodity futures contracts. In addition, bitcoin exchange-traded products (ETPs) and bitcoin futures are relatively new and the markets may be less developed. They are subject to unique and substantial risks, and historically, have been subject to significant price volatility. As a result, the markets for bitcoin futures and bitcoin ETPs may be less developed, and at times, potentially less liquid and more volatile, than more established commodity futures and ETP markets. While the bitcoin futures market has grown substantially since bitcoin futures commenced trading, there can be no assurance that this growth will continue. In addition, derivatives can be volatile and may be less liquid than other securities and more sensitive to the effects of varied economic conditions. The value of the shares of the Fund relate directly to the value of the futures contracts and other assets held by the Fund and any fluctuation in the value of these assets could adversely affect an investment in the Fund's shares. Because of the frequency with which the Fund expects to roll futures contracts, the price of futures contracts further from expiration may be higher (a condition known as “contango”) or lower (a condition known as “backwardation”) and the impact of such contango or backwardation may be greater than the impact would be if the Fund experienced less portfolio turnover. The Fund will not invest in bitcoin directly.

Global Chief Investment Officer

Jeremy Schwartz has served as Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Behind the Markets podcast. Jeremy is a member of the CFA Society of Philadelphia.

Director, Model Portfolios

Andrew Okrongly joined WisdomTree in 2022 as a Director on the Model Portfolios Team. He is responsible for the design and ongoing management of model portfolios and custom solutions for portfolio managers and advisors. Andrew is also a member of the Model Portfolio Investment Committee. Prior to joining WisdomTree, Andrew was a Director on the Outsourced Chief Investment Officer (OCIO) team at Commonfund, where he was responsible for macro-economic analysis and advising institutional clients on strategic and tactical asset allocation. Andrew began his career at BlackRock where he held a variety of fixed income and multi-asset investment roles. Andrew received a BBA degree from the University of Michigan and is a holder of the Chartered Financial Analyst designation.