Nowhere to Hide…Except Maybe Treasury Floating Rate Notes

Published April 8, 2026

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Key Takeaways

- Surging energy prices tied to the Middle East conflict have driven a sharp 50–60 basis point (bps) rise in Treasury yields, undermining traditional safe-haven demand and reinforcing the case for floating rate exposure through the WisdomTree Floating Rate Treasury Fund (USFR).

- Despite inflation concerns, treasury inflation-protected securities (TIPS) have failed to protect portfolios in this environment, with 10-year real yields rising ~30 bps, highlighting that they lag rate resets compared to floating rate notes (FRNs), which adjust with short-term benchmarks.

- With the Fed nearing the end of its rate cut cycle and volatility likely to persist even if geopolitical tensions ease, we believe that Treasury FRNs offer a compelling strategy to capture income while mitigating duration risk via USFR.

The Middle East war has proven to be a conundrum for the U.S. Treasury (UST) market. Typically, in times of geopolitical uncertainty, Treasuries are viewed as a safe-haven asset to turn to. However, the surge in energy prices has resulted in heightened inflation fears, and as a result, UST fixed coupon yields across the maturity spectrum have risen noticeably.

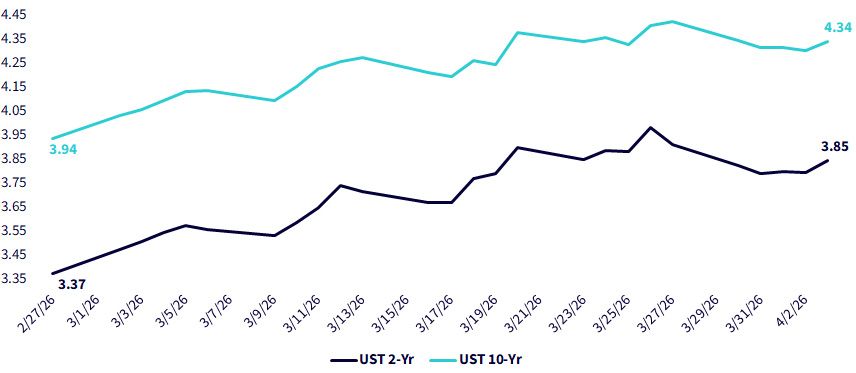

Figure 1: U.S. Treasury Yields

Source: Bloomberg, as of 4/3/2026.

Prior to the Middle East war, UST yields, such as the 2- and 10-year notes, had been falling as concerns surrounding AI’s potential impact on software companies and attendant private credit exposures had produced a flight-to-quality bid. In fact, 2-year yields dropped to 3.37%, the lowest reading since 2022, while 10-year yields fell below the 4% threshold to 3.94%.

While the surge in energy prices has stoked inflation fears, other factors contributing to the sell-off include the reversal of prior ‘long’ positions and yield curve positioning trades, as well as potential liquidation by Persian Gulf nations to raise cash to pay for infrastructure repairs that have been damaged by Iranian missiles and drones.

As a result, 2- and 10-year yield levels had, at one point, risen as much as 60 bps and 50 bps, respectively. While renewed concerns have surfaced about higher energy prices becoming a ‘tax’ on the economy, rates are still considerably above their pre-war levels (see above graph).

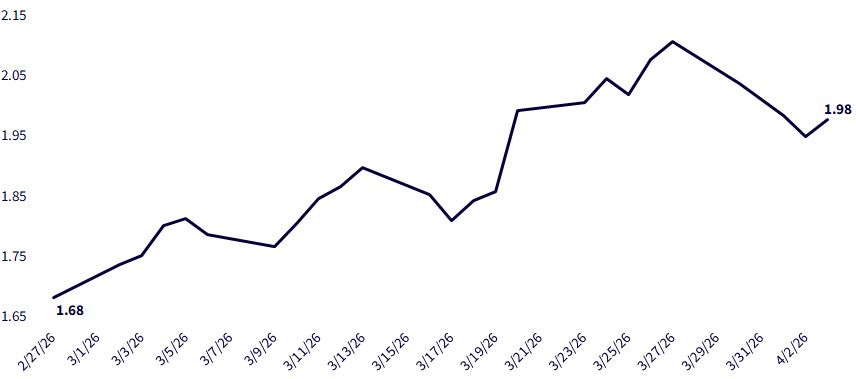

Figure 2: UST 10-Year TIP Yield

Source: Bloomberg, as of 4/3/2026

The interesting aspect to the UST market sell-off has come from the inflation-adjusted sector or TIPS. Once again, investors discovered that TIPS are not immune from increasing yields, even if the catalyst was arguably increasing inflation fears. Remember, TIPS are referenced to actual trailing CPI figures; they are not reset to a specific interest rate, like secured overnight financing rate (SOFR) or the three-month T-bill, to which Treasury Floating Rate Notes (FRNs) are tied (see below). In other words, investing in TIPS is not necessarily an ideal way to position your bond portfolio for rising rates.

The above graph clearly illustrates this point, as 10-year TIPS have seen their yield increase by +30bp from pre-war levels.

Potential Solution: Treasury FRNs

This is where Treasury FRNs can come into play. As investors have witnessed over the last four weeks or so, apart from the FRN space, there has been no place to hide along the UST yield curve, as short-, intermediate- and longer-dated maturities and TIPS have all seen yield levels rise in a visible fashion.

The March jobs report underscored our position that the Fed is at, or near the end, of this rate cut cycle. So, if the Fed is essentially done, or close to it, UST FRN yields are bottoming out. In addition, when the Middle East war does de-escalate, fixed coupon yields may come down from their high watermarks, but it could prove to be short-lived and volatility is not going away any time soon.

The WisdomTree Floating Rate Treasury Fund (USFR) offers investors a potential solution to avoid uncertainty and volatility, as well as any potential increase in rates while still providing a relatively attractive income opportunity.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Securities with floating rates can be less sensitive to interest rate changes than securities with fixed interest rates, but may decline in value. Fixed income securities will normally decline in value as interest rates rise. The value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.