WCBR

Cybersecurity Fund

Published February 19, 2026

Global Head of Research

Sometimes markets behave in ways that don't make sense, as investors get carried away with a particular idea.

This dynamic appears evident in early 2026 when looking at the share price performance of certain cybersecurity stocks. To understand the current picture, it's important to place two concepts in mind:

1. Artificial intelligence (AI) software continues to increase in capability. Collectively, we saw the virality of what is now referenced as OpenClaw1 in contextualizing what an agentic AI future could really look like—and this is simply the most recent example. Enterprises have finite technology budgets. If AI can do more, firms may require less of their ‘other software' solutions. Put another way, sometimes it's postulated that employees can just ‘vibe code' customized software solutions to suit company needs2.

2. It is also true that nearly every time I am seeing OpenClaw mentioned, I am seeing or hearing references to potential cybersecurity issues3. It makes sense, in that if this software is taking actions and has access to important systems without being directed in every instance, it's possible that the user may not agree with all of those actions. There is no guarantee that important private data would not be shared or mishandled.

The implication: If OpenClaw represents an important window into our potential agentic AI future, proper cybersecurity practices will only become more important for both companies and individuals.

The WisdomTree Cybersecurity Fund (WCBR) is a strategy that focuses on a specific group of cybersecurity providers4. Before progressing further, instead of just saying ‘cybersecurity', which can mean many things, let's zoom in on the specific types of cybersecurity these companies must focus on to have the potential for inclusion in this strategy5:

If we can agree that these eight areas of focus at least sound reasonable if a company is seeking to provide cybersecurity solutions to businesses, it allows us to move to looking at performance.

The primary question:How does a group of cybersecurity-focused companies that have a strong focus in at least one of these eight areas look, performance-wise, as of mid-February 2026?

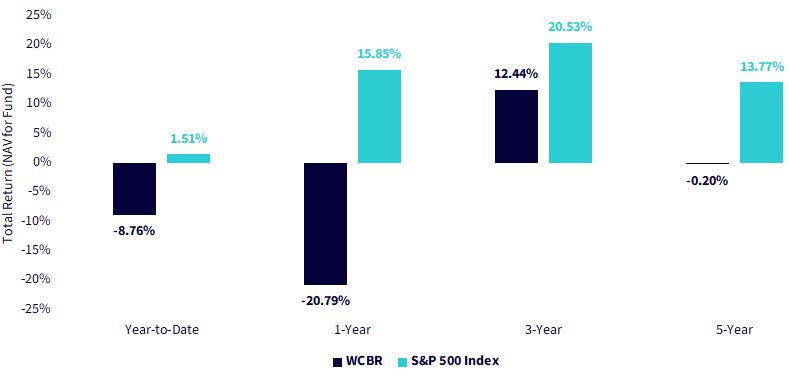

Figure 1a tells the story…

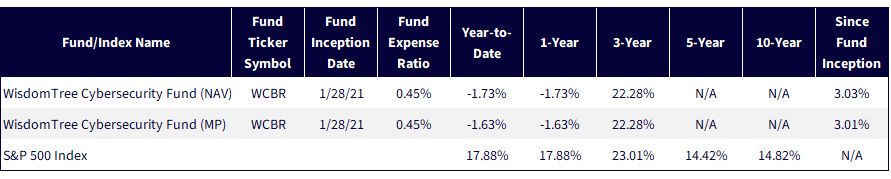

Sources: Morningstar, FactSet and WisdomTree. Data are from the PATH Fund Comparison Tool, accessed as of February 12, 2026, but showing returns for the period ended February 11, 2026 for Figure 1a and December 31, 2025 for 1b. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted.For the most recent month-end and standardized performance, clickhere.

Conclusion: Why do Firms Invest in Cybersecurity Solutions?

Cybersecurity is an area where protection from threats such as hackers and ransomware is only part of the story. Another part is putting together a picture of activities such that a company's cybersecurity strategy appears ‘credible' and ‘up-to-date.' If an issue ever were to occur, it is helpful to be seen to have subscribed to different providers who are amongst the best at such things as network security, identity management, endpoint protection, observability…and the list goes on. There is never a guarantee that issues will never occur, but if or when they do, it's better to be seen as having a comprehensive set of solutions that are accepted as amongst the best-of-breed at what they focus on6.

It's possible that, since many cybersecurity-focused companies are ultimately ‘software-as-a-service' (SaaS), and the equity market at least in early 2026 seems to be running away from this business model, it's possible that there could be a lack of discrimination. It's possible that people see such things as software or SaaS and they seek to position elsewhere and they may not be thinking more deeply about what the software is meant to do7.

Can the downdraft continue? Of course, but it is often that investors tell me they are looking for dislocations and areas where they have not already missed the price appreciation. Cybersecurity in early 2026 may represent one such opportunity.

1 Source: OpenClaw. (n.d.). OpenClaw — Personal AI assistant. Retrieved February 12, 2026, from https://openclaw.ai/

2 Source: ShiftMag. (2025, The Illusion of Vibe Coding: There Are No Shortcuts to Mastery). ShiftMag.dev.

3 Source: Stokel-Walker, C. (2026, February 3). OpenClaw is a major leap forward for AI — and a cybersecurity nightmare. Fast Company.

4 WCBR is built to track the total return performance of, before fees and expenses, the WisdomTree Team8 Cybersecurity Index.

5 Source: The WisdomTree Team8 Cybersecurity Index defines as part of its selection criteria that companies must have a strong solution in at least one of the eight themes to be eligible for further screening and possible index inclusion.

6 Sources: LegalClarity.org. (2026). Building a legally compliant cyber security strategy; Fortinet. (2026). Why compliance is a critical part of a cybersecurity strategy; Larcker, D. F., & Tayan, B. (2022). Building effective cybersecurity governance. Harvard Law School Forum on Corporate Governance.

7 Sources: Cohan, P. (2026, February 6). Why SaaS stocks are falling as AI reshapes software. Forbes; Lipman, D., Callahan, G., Fiore, G., Kieffer, G., & Bosche, A. (2026). Why SaaS stocks have dropped—and what it signals for software's next chapter. Bain & Company.

There are risks associated with investing, including possible loss of principal. The Fund invests in cybersecurity companies, which generate a meaningful part of their revenue from security protocols that prevent intrusion and attacks to systems, networks, applications, computers, and mobile devices. Cybersecurity companies are particularly vulnerable to rapid changes in technology, rapid obsolescence of products and services, the loss of patent, copyright and trademark protections, government regulation and competition, both domestically and internationally. Cybersecurity company stocks, especially those which are internet related, have experienced extreme price and volume fluctuations in the past that have often been unrelated to their operating performance. These companies may also be smaller and less experienced companies, with limited product or service lines, markets or financial resources and fewer experienced management or marketing personnel. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Cybersecurity Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.