From Lagging to Leading? The Case for a Small-Cap Inflection Point

Published February 23, 2026

Christopher Gannatti, CFA

Global Head of Research

Key Takeaways

- After nearly 13 years of persistent small-cap underperformance, early 2026 has opened with a sharp reversal in relative returns, suggesting the WisdomTree U.S. SmallCap Quality Dividend Growth Fund (DGRS) may be entering a potential leadership inflection point worth monitoring closely.

- While DGRS has outperformed the S&P 500 in only two calendar years since 2014, its discounted valuation profile, trading around 13x earnings versus materially higher large-cap multiples, creates a compelling risk-reward setup if earnings stabilize and market leadership broadens.

- With price-to-cash-flow, price-to-book and price-to-sales ratios all at less than half those of the S&P 500, small-cap quality dividend growers appear priced for muted expectations, positioning DGRS as a contrarian allocation should 2026 mark the start of a sustained rotation away from mega-cap concentration.

In sports, momentum is rarely subtle. A turnover before halftime. A three-pointer that silences the home crowd. A sudden defensive stop that changes the rhythm of the game. You can feel it before the scoreboard fully reflects it. The energy shifts. The confidence moves. What looked inevitable moments ago suddenly feels uncertain.

Markets move in similar cycles. Investors gravitate toward what has been working, reinforcing trends that can persist for years. Winning teams attract more fans; winning stocks attract more capital. Leadership becomes concentrated. Narratives harden.

But just as in sports, momentum can stall, and sometimes reverse. The question is rarely whether a shift will happen. It’s when.

For more than a decade, U.S. large caps have dominated the equity landscape. Small caps, by contrast, have largely trailed. Yet early 2026 performance hints at something different. It may be noise. Or it may be the first signal that leadership in U.S. equities is beginning to rotate.1

A Nearly 13-Year Drought—and a Very Different Start to 2026

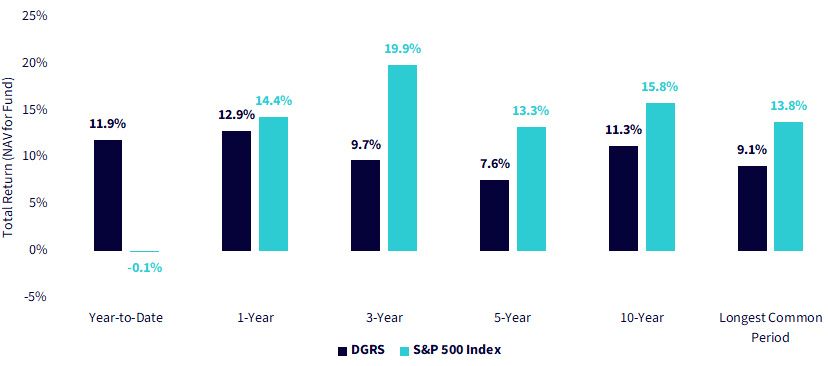

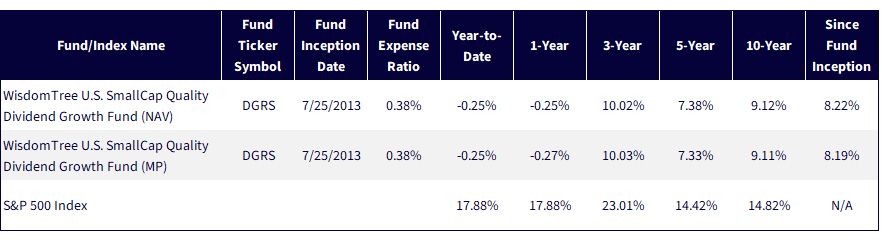

The WisdomTree U.S. SmallCap Quality Dividend Growth Fund (DGRS) has faced a difficult performance environment in recent years. In our experience, investors tend to focus first on the S&P 500 Index or similar large-cap-oriented domestic strategies. Small caps represent adding something different. Figure 1a shows two very distinct things, in my opinion:

- Across the one-, three-, five-, 10- and ‘Longest Common’ periods,2 DGRS's performance has significantly lagged that of the S&P 500 Index. This is notable in the context of equity factor discussions. Small caps can be riskier, but historically, in certain periods, that additional risk has been rewarded with stronger performance. Over this period, which stretches nearly 13 years, DGRS has not exhibited outperformance against the S&P 500 benchmark.

- Then, we look at the Year-to-Date period, which represents the start of 2026 through February 12 and we see a completely different story. We don’t know if that story will persist, but it’s important to keep an eye on it since it could portend a dramatic turn in U.S. equity market leadership.

Figure 1a: A Nearly 13-Year Gap—and a Very Different Start to 2026

Figure 1b: Standardized Performance

Sources: WisdomTree, FactSet specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed February 13, 2026 with returns as of February 12, 2026 for Figure 1a and December 31, 2025 for Figure 1b. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

Two Wins. Ten Losses. The Calendar-Year Reality.

Viewed year by year, the pattern feels less like randomness and more like a long stretch of large-cap dominance interrupted by brief counter-moves. Since 2014, DGRS has led in just two calendar years: 2016 and 2022. Both were meaningful, but they were also short-lived. In 2016, small caps surged decisively ahead. In 2022, they provided valuable downside resilience in a difficult market. Yet outside of those moments, the S&P 500 consistently reasserted leadership, particularly during the powerful rally after Covid-19 and leading into the robust generative AI environment that began in November 2022.3

The takeaway isn’t that small caps never lead. We know that they clearly can. It’s that leadership has been episodic, not sustained. After more than a decade of relative underperformance, the more relevant question may be whether we might be due for a shift in leadership that may have a longer shelf life.

Figure 2: Long Stretches of Lag, Short Bursts of Leadership

Sources: WisdomTree, FactSet specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed February 13, 2026 with returns as of the specified calendar years, example being 1/1/2014 to 12/31/2014 for 2014. Further years are calculated analogously. Fund returns are measured at NAV. Past performance is not indicative of future results.

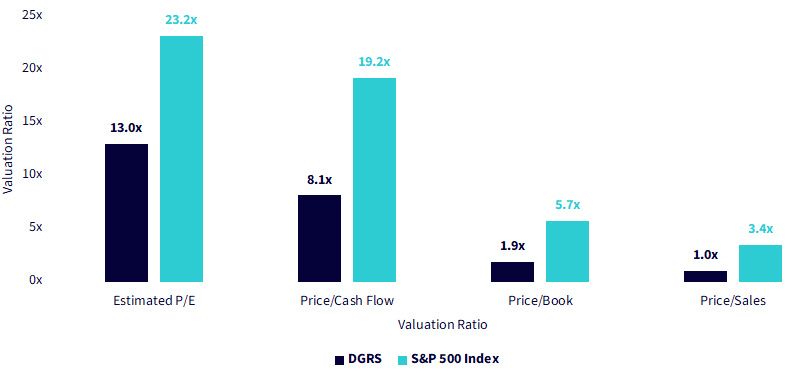

The Valuation Gap Is Striking

While we can never be sure of what forward-looking performance will bring in any investment strategy, what we can do is note the fundamental picture visible at present. Some of these statistics are staggering, in my opinion:

- Estimated P/E Ratio: DGRS exhibited a 13.0x, which was roughly 10.0x below that of the S&P 500 Index.

- Price/Cash Flow Ratio: DGRS exhibited a 8.1x, which was less than half that of the S&P 500 Index, shown at 19.2x.

- Price/Book Ratio: DGRS exhibited a 1.9x, less than half that of the S&P 500 Index at 5.7x.

- Price/Sales Ratio: DGRS exhibited a 1.0x, again, less than half that of the S&P 500 Index at 3.4x.

Figure 3: Priced for Very Different Potential Futures

Sources: WisdomTree, FactSet, Morningstar, with data as of January 31, 2026. Subject to change.

If Leadership Turns, This May Be the Setup

We cannot know what future returns will bring, but valuation ratios help frame the expectations already embedded in prices. Lower multiples typically reflect more modest forward assumptions about growth and profitability. That also means the hurdle to exceed expectations is lower. If results simply stabilize or improve incrementally, share prices can respond meaningfully. Higher valuations, by contrast, signal elevated expectations and a narrower margin for error. Strong performance must persist merely to justify today’s pricing.

DGRS sits on the lower end of that spectrum. Its discounted multiples suggest subdued expectations, while early 2026 performance hints, cautiously, at improving momentum. That combination does not guarantee a shift in leadership, but it does create a different risk-reward profile. After a prolonged stretch of small-cap underperformance, the setup itself may warrant closer attention.

1 Sources: Barron’s (December 10, 2025), “Small-Cap Stocks May Be Ready to Outperform After Five Years of Lagging”; Schwab (2025), “Can Small Caps Bounce Back?”

2 The longest common period refers to July 25, 2013, to February 12, 2026, the full period since inception for DGRS.

3 Source: OpenAI (November 30, 2022). Introducing ChatGPT.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Growth stocks, as a group, may be out of favor with the market and underperform value stocks or the overall equity market. Growth stocks are generally more sensitive to market movements than other types of stocks. Funds focusing their investments on certain sectors and/or smaller companies increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. The Fund is non-diversified, as a result, changes in the market value of a single security could cause greater fluctuations in the value of Fund shares than would occur in a diversified fund. The securities of small-capitalization companies generally trade in lower volumes and are subject to greater and more unpredictable price changes than larger capitalization stocks or the stock market as a whole. Small-capitalization companies may be particularly sensitive to adverse economic developments as well as changes in interest rates, government regulation, borrowing costs and earnings. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

About the contributor

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.