Warsh’s Reality Check: The Fed Balance Sheet

Published February 18, 2026

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Key Takeaways

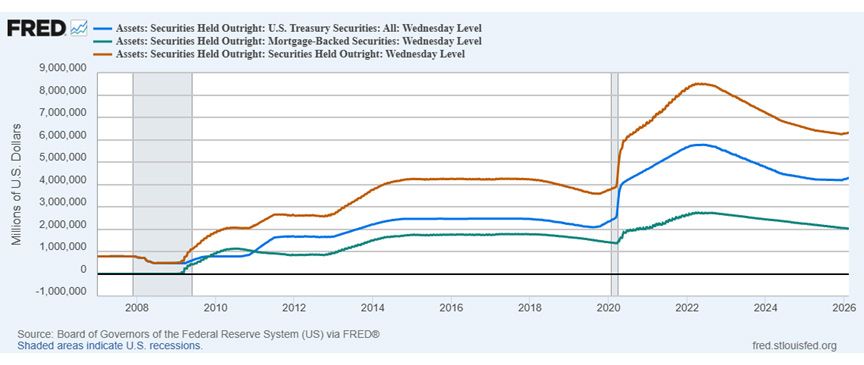

- With Fed holdings of Treasuries and MBS still totaling $6.3 trillion, well above the $4.25 trillion peak following the Financial Crisis, any Warsh-led effort to shrink the balance sheet could have potentially meaningful implications for longer-dated yields and mortgage rates.

- Although Quantitative Tightening reduced the balance sheet by $2.2 trillion from its 2022 peak, policymakers still face a difficult choice between passive runoff and active sales, each carrying potential disruptions for funding markets and financial conditions.

- While Warsh has discussed the possibility of rate cuts, he has framed them alongside balance sheet reduction, suggesting that any policy easing would likely remain data dependent and accompanied by a continued effort to reduce the Fed’s overall footprint.

Last week, I weighed in on Kevin Warsh being nominated to be the next Fed Chair and provided some background and perspective about where he might take the U.S. central bank under his leadership. This week, I wanted to go a little deeper in the analysis, specifically the notion that Warsh would like to reduce the Fed's ‘footprint.'

As you may recall, the Fed's ‘footprint' really consists of two dynamics: the balance sheet and forward guidance. This blog will focus on the Fed’s balance sheet—specifically its holdings of Treasury securities (USTs) and mortgage-backed securities (MBS). For the record, the actual Fed balance sheet consists of many other line items besides its UST and MBS holdings (known as the System Open Market Account or SOMA), but this is typically where the lion's share of attention resides.

It has been no secret that Warsh is not a fan of Quantitative Easing (QE), both while he was a Fed governor and more recently in comments and writings. That being said, in the aftermath of the Financial Crisis and Great Recession, he did not dissent when the Bernanke-led Fed initially decided to pursue QE.

Source: St. Louis Fed, as of February 13, 2026

However, let's fast-forward and assume Warsh is confirmed as the next Fed Chair. What can he do about that balance sheet in reality? Well, the first thing he would have to do is to get the remaining Fed governors and regional bank presidents on board with a plan on how to shrink the Fed's UST and MBS securities holdings. Then comes the size of SOMA and that's where reality sinks in. Total Fed holdings of Treasuries and MBS at present come in at $6.3 trillion, with a breakdown of $4.3 trillion in USTs and $2.0 trillion in MBS. In the post–Financial Crisis period, the peak total was $4.25 trillion combined!

Let's offer some perspective, at its peak in 2022, SOMA was at $8.5 trillion, consisting of roughly $5.8 trillion in Treasuries and $2.7 trillion in MBS. In other words, the Quantitative Tightening (QT) which was put in place in mid-2022 and ended on December 1, reduced the Fed’s balance sheet by $2.2 trillion.

There are a few ways the policymakers can reduce their SOMA holdings. There is the passive approach—allowing a certain amount of securities to mature or be redeemed without replacement—or the more disruptive active approach of outright selling Treasuries or MBS. The aforementioned QT was an example of the passive approach where only a portion of maturing securities was allowed to roll off the balance sheet.

Interestingly, the current Powell-led Fed and Warsh appear to agree on one point: the Fed should hold only Treasuries. However, with $2.0 trillion ‘still on the books', that is a Herculean task in and of itself. Indeed, either approach—particularly active sales—could have unintended consequences for longer-dated yields and, by extension, mortgage rates.

What about the Treasury portion of SOMA? Similarly, by definition, QT of any kind is a tightening of monetary policy and could result in higher rates. In addition, as witnessed in both the pre-COVID episode of QT and the most recent round, upward pressures in the funding markets have appeared and required intervention. What happened during each of the ‘plumbing issues’ in the funding markets? The Fed bought Treasuries—that is, it restarted QE to ease conditions in the money markets.

There are also other options to adjust the balance sheet, such as decreasing the weighted average maturity of their UST holdings. However, there's no point losing any sleep over the issue at this juncture.

Conclusion

Perhaps the most important aspect of the Fed footprint concept is that Warsh discussed rate cuts—but in the context of reducing the Fed’s balance sheet. In my view, any Warsh-led rate cuts that could come this year or into 2026 would likely be of the traditional, data-dependent variety.

Categories

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.